{kind=link}

LISTEN TO STORY

WATCH STORY

By Adolf

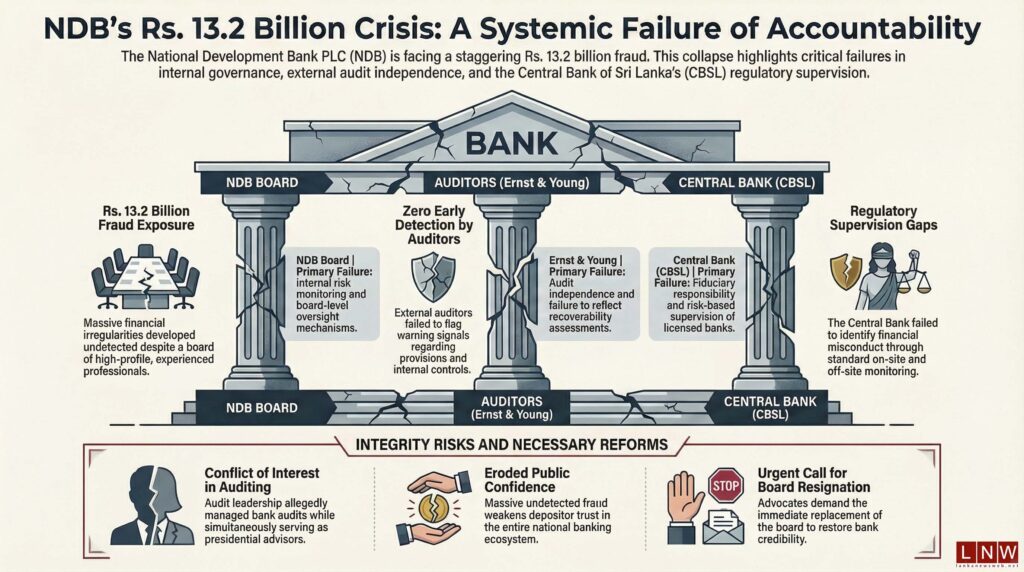

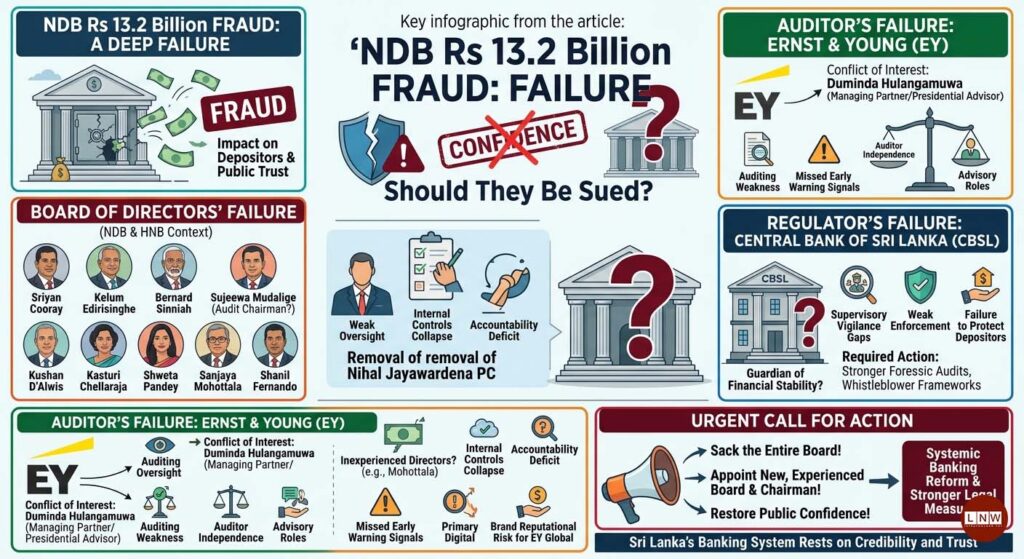

Recent developments surrounding the Rs. 13.2 billion fraud at National Development Bank PLC (NDB), together with the earlier governance controversy involving Hatton National Bank PLC (HNB), should serve as a serious wake-up call for the entire financial ecosystem—banks, auditors, and the regulator. In particular, the role of the Central Bank of Sri Lanka (CBSL) and the responsibilities of external auditors such as Ernst & Young must now come under sharper public scrutiny. Despite public concerns raised regarding governance issues linked to the appointment of Suresh Shah, the regulator allowed the appointment to proceed at HNB. The governance arrangements that followed enabled a small group of directors—including Suresh Shah and Reganathan Samarasinghe—who reportedly held no meaningful shareholding in the bank, to influence the removal of a sitting chairman, Nihal Jayawardena PC (ugly and disgraceful), widely regarded as a strong governance advocate. Such developments triggered widespread debate within corporate and banking circles about the strength of governance safeguards in systemically important banks.

Failure by CBSL

More recently, public allegations have surfaced relating to customer complaints and possible irregularities involving Hatton National Bank PLC (https://slguardian.org/sri-lankas-hnb-in-fraud-storm-as-customers-allege-funds-quietly-taken/). Whether these allegations are ultimately proven or not, the reputational impact on a major financial institution is significant. When governance concerns persist within a leading bank, questions inevitably arise about the role of the regulator responsible for supervising the sector.

Inexperienced Directors

At the same time, the alleged fraud of approximately Rs. 13.2 billion at National Development Bank PLC raises deeper questions about oversight and internal controls. The board of NDB includes several experienced professionals such as Sriyan Cooray, Kelum Edirisinghe, Bernard Sinniah, Sujeewa Mudalige, Kushan D’Alwis, Kasturi Chellaraja, Shweta Pandey, Sanjaya Mohottala and Shanil Fernando. With such a high-profile board, stakeholders would have expected reasonably strong governance oversight and robust risk controls. Kasturi is the female god of business, Mohottala a failed BOI Chairman, Sujeewa Mudalige the master craftsman for accounts (did CBSL check why he left HNB? But cleared him for NDB Audit Chairman ). Particularly noteworthy is the role of the audit committee, which is central to safeguarding financial integrity within a bank. The effectiveness of audit oversight becomes even more critical when large financial exposures or irregularities emerge. If such a significant fraud could develop within a regulated institution, it inevitably raises questions about whether internal risk monitoring, audit review processes, and board oversight mechanisms were sufficiently rigorous.

Failure of Ernst & Young

External auditors also carry significant responsibility in protecting stakeholders. Firms such as Ernst & Young are entrusted with reviewing financial statements and assessing whether adequate provisions, recoverability assessments, and internal controls are properly reflected in financial reporting. When substantial financial irregularities later surface, the natural question is whether audit procedures were sufficiently robust to detect early warning signals. The potential conflicts of the managing partner of Ernst & Young Sri Lanka, Duminda Hulangamuwa, deserve special attention. Sources indicate that he is simultaneously engaged in advisory work for the President while also managing the audit firm. Such dual roles create an inherent conflict of interest, compromising independence and raising doubts about the effectiveness of audit oversight at NDB. Stakeholders must ask whether these conflicts may have contributed to the failure to identify recoverable or irregular transactions before the fraud surfaced. Independence is the cornerstone of auditing credibility, and any compromise erodes public trust. Ernst & Young global needs to wake up to protect its brand name in Sri Lanka.

Confidence

Sri Lanka’s banking system rests fundamentally on confidence. Depositors place their savings in banks believing that institutions are governed prudently, managed responsibly, and supervised rigorously by the regulator. When a fraud of Rs. 13.2 billion occurs within a licensed bank, the public quite reasonably asks how such a large exposure could have developed without early detection through internal audits, external audits, and regulatory supervision. For God’s sake, 13 billion and no one knew it was happening?

Role of CBSL

Banks are among the most closely supervised institutions in any economy. Through on-site examinations, off-site surveillance, risk-based supervision, and compliance monitoring, regulators are expected to identify warning signals well before financial misconduct reaches systemic levels. If a fraud of this magnitude occurs, it inevitably suggests potential gaps in internal controls, governance, or supervisory vigilance. Regulators carry a heavy fiduciary responsibility. The mandate of the Central Bank of Sri Lanka goes beyond enforcing technical compliance. It includes protecting depositors, preserving financial stability, and ensuring that boards of financial institutions adhere to the highest governance standards. When governance lapses appear to go unchecked or financial irregularities surface on a large scale, public confidence in the regulatory framework is inevitably weakened. Globally, regulators have strengthened oversight following similar episodes. Enhanced forensic audit capabilities, stronger whistleblower frameworks, and real-time monitoring of large financial exposures are increasingly standard practices. Sri Lanka cannot afford to fall behind in strengthening these supervisory mechanisms. Equally important is the need for banks themselves to reinforce governance standards. Independent boards, empowered audit committees, transparent leadership appointments, and strong risk management cultures remain the foundation of a resilient financial system. Sri Lanka’s banking sector has historically been viewed as one of the more stable pillars of the economy. Protecting that reputation requires decisive action whenever governance concerns or financial irregularities arise.

Sack the Board

The alleged fraud at National Development Bank PLC and the governance controversies surrounding Hatton National Bank PLC should therefore serve as a wake-up call for banks, auditors, and the Central Bank of Sri Lanka. Stronger oversight, stricter accountability, and uncompromising governance standards are essential if trust in the financial system is to be preserved. Ultimately, financial stability rests not only on capital and liquidity but on credibility, transparency, and vigilant supervision. When those pillars weaken, the consequences extend far beyond any single institution. The time for serious regulatory introspection is now. CBSL should immediately ask the entire board to resign given the stench and depth of the fraud, ( they will not resign) and appoint a new board of experienced directors and a chairman to win back the confidence of the public. They should not fail again.