{kind=link}

The new Open Market Operations (OMO) system comes into effect today, 16th January 2023, which is a special bank holiday. In last two articles released to this blog on this subject, I commented on this new OMO as follows.

- It invalidates the present policy interest rates corridor and money market-based monetary policy model followed by the Monetary Board and breaches the authority given to the Monetary Board under the Monetary Law Act (MLA) for implementation of the National Monetary Policy.

- Inter-bank overnight interest rates will move beyond the policy rates corridor depending on market conditions.

- This provides the space for the Central Bank to favour its friendly dealers on liquidity management through money printing via frequently conducted repo and reverse repo auctions that may be connected with insider monetary dealings.

This article is to elaborate further on this subject. It mainly focuses on explicit price controls and rationing on money under the new OMO rule and resulting market irregularities and abuses like in commodity markets.

The author’s objective is to stress that such ad hoc monetary policy actions are not the types of policy action that should be adopted in compliance with the MLA to help the recovery of the economy from the present crisis.

New OMO Rule to be effective from 16th January

Limits on Overnight Standing Facilities

- Limiting the overnight standing deposit (SDF) facility to a maximum of five times/days in any month for any commercial bank.

- Limiting the overnight standing lending facility (SLF) to a maximum of 90% of the statutory reserves of each commercial bank on the day.

- Limits are not applicable to primary dealers in government securities.

Interest Rates on Standing Facilities

The rates known as SDFR and SLFR which are 14.5% and 15.5%, respectively, as at present will continue until the Monetary Board may revise them independently.

New OMO Rule as a direct market control

SDFR and SLFR are no different from price controls in the inter-bank overnight market. SDFR is the floor price and SLFR is the maximum price. So far, they have been operated without any control over market volumes. The reason was the availability of the unrestricted SDF and SLF. As the Central Bank has the autonomy in printing money without limits, it supplied money in any quantity to keep the maximum price, SLFR and purchased any amount of money to keep the floor price, SDFR.

Therefore, SLFR and SDFR did not confront implementation problems although they also were price controls imposed by the Central Bank. SLFR and SDFR are just administrative prices as the Central Bank does not have a mechanism to know the market clearing prices. Therefore, liquidity imbalances in the inter-bank market are inevitable and the Central Bank balance them through SDF, SLF and other OMO instruments.

However, the Government in commodity markets always fails to administer such controlled prices such as rice price and paddy price because it does not have the control over the production and supply of commodities subject to price controls.

Therefore, the government tends to impose rationing of such commodities to ensure that the market is controlled to help the needy segments at controlled prices. However, the existence of black markets and market irregularities in response to such market controls is not a secret.

The new OMO limits are nothing but monetary rationing by the Government or the Central Bank. The SDF limit is similar to the Paddy Marketing Board purchasing limited quantity of paddy on the guaranteed price. Conversely, the SLF limit is similar to the government selling limited quantities of food items at controlled prices through CWE.

Therefore, black markets and irregularities in money markets will emerge in due course. Nobody needs Economics knowledge to understand it. It is a well-experienced real-world activity seen from ancient times of market controls. I hope that A/L students and teachers will analyze the market impact of new OMO rule and estimate its dead-weigh loss to the economy.

Key Points in the Central Bank Press Release on the New OMO Rule

According to the press release issued by the Communication Department on 7th January (see below), the objectives of the New OMO rule are as follows.

- To reduce the overdependence of some banks on the standing facilities without considering market-based funding options to address their structural liquidity needs. Standing facilities are only fallback options to be resorted to after utilizing all other funding options.

- To reactivate money markets, primarily the interbank call money market and the repo market which remained nearly inactive for the last few months. Such inactivity poses a threat to smooth channeling of funds in the economy with a possibility of clogging the payment and settlement systems.

- To eliminate unhealthy competition for deposits among financial institutions and the new rule would be instrumental in inducing a moderation in the market interest rate structure (of both deposit and lending interest rates) in the period ahead along with improving market liquidity conditions.

My comments on the press release

- All these objectives are nothing but a sum of words whose meaning is not understood by those who drafted and authorized the press release.

- If the is new rule can restore the stability of the economy and financial system, the Director of Domestic Operations who decided the new rule is the God. So, both the government and the Central Bank must immediately abandon the debt restructuring and IMF programme pending for nearly one year.

- Standing facilities are the essential elements of the present inter-bank overnight interest rate targeting-based monetary policy models followed in line with global monetary policy practices. Therefore, they are not fallback options as stated in the press release. Fallback funding is well known as the Lender of Last Resort (LOLR) that central banks implement in different market conditions and circumstances.

- Unhealthy competition for deposits was induced by the Central Bank itself by forcing and encouraging banks to raise deposit mobilization as a part of the new monetary policy strategy adopted to control the hyperinflation since 8th April, 2022. The Central Bank in fact issued a Direction on 21 April, 2022, requiring banks to raise deposit interest rates in line with the policy rate hike. Therefore, moderation in market interest rate structure and improvement in market liquidity conditions can be expected only from reduction in policy rates and relaxation of monetary policy. Therefore, the new rule is like an attempt to swallow medicine without allowing the tongue and throat to feel and against the basic monetary policy principle.

- Inter-bank funding operations are based on trust and risks. In crisis times, the inactivity in inter-bank market is normal due to the erosion of trust. Call money is a trusted deal without collaterals and market repos also have issues on underlying securities. Therefore, the new OMO rule cannot resolve the inter-bank trust issue to reactivate the money market, given the weak financial conditions of banks under current economic and financial circumstances.

Therefore, it is advisable that the Central Bank carefully refers to their standard textbooks and institutional policy memory when such press releases of policy/technical nature are drafted and authorized.

Monetary Black Market and Irregularities Expected

Like in commodity markets, money dealers in banks will have black market transactions through various devices which are not daily monitored by the Central Bank. For example, when the Central Bank monitors bank foreign exchange spot deals (T+2) to ensure that deals are at exchange rates set unofficially, bank dealers start T+3 and above to circumvent the Central Bank rule. Foreign exchange market is well known for black market devices adopted to circumvent the exchange controls. However, it is too early to trace specific inter-bank dealing devices that would be invented in response to the new OMO rule as the new rule is a new experience in the banking history of Sri Lanka.

As I mentioned in the two previous articles, the Central Bank will use its money printing and regulatory powers to engage in insider monetary operations with identified banks to show the world that new OMO rule produces intended outcomes, i.e., moderation of interest rate structure, reactivation of the inter-bank market and improvement in bank-wise liquidity management and financial stability in its rhetoric.

The potential of such insider monetary dealings is already shown by the data.

- First, the total daily volume of standing lending has started falling significantly well before the effective date of the new rule. The decline as on last Friday (13 January) from 2nd January is Rs. 347.9 bn or 63.8%, i.e., to Rs. 197.2 bn from Rs. 545.1 bn. This shows a very strange money market during the last week. However, standing deposits remained around same levels.

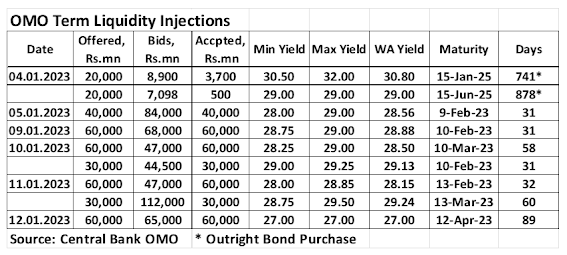

- Second, the decline in standing lending is a direct result of insider monetary deals. The Central Bank/Domestic Operations Dept. has commenced active auctions to inject new money on a permanent and term basis to banks. From 2nd to 12th January, 10 auctions were conducted and Rs. 344.2 bn was injected, i.e., permanent liquidity of Rs. 4.2 bn and long-term liquidity of Rs. 340 bn. with the term ranging from 31 days to 878 days and interest rates ranging from 27% to 30.8% (see Table below). This new money could be routed to illiquid banks at unofficially directed interest rates through agent banks organized unofficially. The Central Bank had a similar habit of selling foreign exchange though such agent banks. Since there is no active secondary market on government securities for similar terms, the public is unable to assess the interest rates and term structure behind such monetary dealings. For example, on 12th January, Rs. 60 bn at 27% has been granted to one bank for 89 days as compared to Rs. 30 bn granted at 29.24% for 60 days previous day. Whether the secondary market activity so active to offer new money to one party at a lower rate for a longer term than the rate on the previous day auction is questionable. Further, why those banks borrow from the Central Bank at such high rates against government securities is not clear as banks can raise deposits at much lower interest rates. Therefore, standing lending volume has been artificially brough down through arranged long-term injection of new money. It is nothing but a market manipulation through insider monetary dealings.

- Third, as a result of term reverse repo injections and reduction in standing lending, the overnight liquidity in the banking sector declined from negative Rs. 231 bn (deficit) at the end of December 2022 to a surplus of Rs. 117 bn as on last Friday (13 January). However, outstanding liquidity continued to be a high deficit of Rs. 333 bn on last Friday (as compared to the deficit of Rs. 361 bn at the end of 2022) due to new term-injections (total Rs. 344 bn) offsetting the decline in overnight liquidity. Therefore, these monetary are nothing but outcomes of insider monetary dealings.

- Fourth, if the price control on one point of the supply chain is to be maintained, it will require a series of price controls and rationing on other points of the supply chain. The good example is the exchange control. Therefore, there is a considerable risk that the Director, Domestic Operations, may impose controls on various banking transactions such as deposit withdrawals and lending by referring to the bank liquidity management and OMO procedure for preservation of the financial system stability. Such controls could even cause bank runs, given the current status of the poor health of the banking system consequent to the present economic crisis.

Conceptual debate on present policy interest rates based monetary policy model

This model has been introduced in 1997 and operated with the blessings of the IMF and World Bank under the Central Bank modernization to be in line with developed market models. The assumption behind the model is that the liquidity of the economy, excess or deficit, is reflected by the banking sector liquidity. Therefore, inflation targeting can be achieved through policy interest rates adopted to regulate the banking sector liquidity. In this model, standing facilities are freely available without any regard to bank-wise differences in liquidity and usage of standing facilities because what is targeted here are the inter-bank aggregates and not individual banks. Therefore, the model is a market-based monetary policy mechanism.

However, in times of 2012 and 2013 when huge excess liquidity in the banking system was built up due to foreign inflows to government securities market, banks started parking such excess liquidity at SDF. The Central Bank also moped up the excess through repo auctions. As I was the Secretary to the Monetary Board and engaged in bank supervision function, I started arguing that the excess liquidity was a micro-prudential issue that should be resolved by the bank supervision with respective banks.

I disputed the approach to the banking sector liquidity as the reflection of the economy’s liquidity as various sectors of the economy suffer chronic liquidity shortages without access to the banking system. Irrespective of the banking liquidity levels, the government inherently suffers liquidity problems. The bone of my contention was that this interbank liquidity and policy rates based monetary policy model copied from developed market economies was not appropriate for Sri Lanka. I also proposed at several strategic meetings that the Consumer Price Index should be targeted in the monetary policy to be mor accountable unlike in the base-biased statistical inflation target.

However, when the subject was debated at a top level forum in the Central Bank, one of the monetary policy group annoyed me by inquiring whether I had forgotten my economics to talk about micro-prudential approach. I now find that same set of professional monetary economists have introduced the new OMO rule of micro-prudential or bank specific approach and forgotten the market approach of the liquidity believed by them in 2012/13.

In addition, when the Monetary Board approved the SDF and SDFR in 2013 in place of the overnight repo rate and standing repo facility, I clarified the Monetary Board that it was a non-compliance as the MLA does not provide for acceptance of deposits on payment of interest. However, the MLA provides for payment of interest on statutory reserves balances. In fact, the instrument authorized for OMO under the MLA is the trade of government securities and Central Bank own securities.

However, on the legal opinion that the Central Bank has the authority to regulate the supply, availability and cost of money, the Monetary Board approved the new policy rates and standing facilities. However, the legal opinion so cited related to an OMO governing principle given in the MLA and not the specific authority. Another OMO governing principle in the MLA is the stabilization of the value of government securities or interest rates without altering the fundamental movements to promote private investments. This is generally regarded as the yield curve control.

However, new policy rates abandoned this principle of monetary policy and the Central Bank used a private placement-based bond issuance system to control the value/yield rates of government securities outside the monetary policy. Central banks globally use the monetary policy OMO to control the yield curve as the benchmark for guiding market interest rates.

I continuously maintained that the present monetary policy model was not appropriate for Sri Lanka. Now, with the new OMO rule the Central Bank has not only accepted same view but also virtually abandoned the model without a new policy model in line with global standards.

Therefore, the Central Bank’s new rhetoric that the new OMO rule is to restore stability of the Sri Lankan economy while preserving stability of the financial system is only a fiction.

If so, the new Governor would have introduced same OMO rule on 8th April 2022 without defaulting loans and bankrupting everybody by red-hot interest rates as he was not a stranger to the monetary policy and Central Bank who could be misled by officials. Therefore, the new OMO rule shows the incompetence of the Governor and his team to implement the correct monetary policies at the correct time. This is not the time for policy-testing.

It is also surprising that same IMF and World Bank now sanction the Central Bank to resume a monetary price controls in place of current inflation targeting market-based monetary policy while requiring the fiscal policy to follow market prices.

Overall Comments

- The global standard of the monetary policy used for inflation targeting has now collapsed in Sri Lanka with the new OMO rule introduced by the Director, Domestic Operations. The new monetary price control with rationing by the Central Bank is not a policy model tested for inflation targeting.

- Therefore, the Monetary Board has no monetary policy framework to reduce inflation from 57.2% at present to 4%-6% in the near term and, therefore, its existence despite wide powers in the MLA serves no purpose.

- It is likely that maintenance of such monetary price controls and rationing at the apex level of the monetary system will require a series of similar controls on the monetary chain down the line. The resulting irregularities and dead-weigh losses will push the economy to further catastrophe.

- The new OMO rule does not provide the types of monetary needs of the economy for recovering from the bankruptcy caused by the monetary policy itself.

- Therefore, if the Monetary Board is to survive within the MLA, it has to come up with a new monetary policy model to provide the country with monetary needs required for the recovery of supply side of the economy within the powers given to it by the MLA.

- If that does not happen, it is the public duty of the Minister of Finance to direct the Monetary Board under section 116(2) of the MLA to adopt a type of monetary policy to the greatest advantage of the people of Sri Lanka as directed by the Minister.

- Alternatively, if the Minister gets the Parliament to give the autonomy to the Central Bank Governor to operate the Central Bank like a private central bank in consultation with Deputy Governors virtually appointed by the Governor, because the IMF wants for the grant of 2.9 bn USD loan being dragged on for about a year, they will install the money printing machines at their homes at the cost to the public. That will be the end of the present state money-based monetary system of the country as they are not divine.

- Therefore, all layers of policymaking authorities must be mindful of the loss to the socio-economic living standards of the public due to the present economic crisis and ad hoc, unjustified policies that are against the basic fundamental rights guaranteed to citizens of Sri Lanka by the Constitution. The last week Supreme Court judgement on the Easter Sunday Terrorist Attack is a real eye opener to high-ranking public officials who are legally empowered with public powers to protect the public, irrespective of their policy rhetoric and tribal concepts.

- In this context, business bankruptcies, loss of income and employment, malnutrition of children, death of patients due to non-availability of critical medicine and acquisition of mortgaged property by banks on loans defaulted due to bankruptcies are nothing but losses to the public caused by the economic terrorist attack. Therefore, lapses in fiscal policy and monetary policy followed in the recent past, at present and in future could well be a subject of fundamental rights applications against the authorized public officials and landmark judgements may be expected.

- Therefore, it is advisable that leading internationally trained economists of the Central Bank give up the practice of monetary policy tinkering and market manipulations and innovate policies justifiable in law or order to help the government and the public to recover the economy from the current crisis.

References

New OMO Circular

New OMO Press Release

Monetary Board Order on Deposit Interest Rates

(This article is released in the interest of participating in the professional dialogue to find out solutions to present economic crisis confronted by the general public consequent to the global Corona pandemic, subsequent economic disruptions and shocks both local and global and policy failures.)

P Samarasiri

Former Deputy Governor, Central Bank of Sri Lanka

(Former Director of Bank Supervision, Assistant Governor, Secretary to the Monetary Board and Compliance Officer of the Central Bank, Former Chairman of the Sri Lanka Accounting and Auditing Standards Board and Credit Information Bureau, Former Chairman and Vice Chairman of the Institute of Bankers of Sri Lanka, Former Member of the Securities and Exchange Commission and Insurance Regulatory Commission and the Author of 10 Economics and Banking Books and a large number of articles publish.

The author holds BA Hons in Economics from University of Colombo, MA in Economics from University of Kansas, USA, and international training exposures in economic management and financial system regulation)

Economy Forward: https://economyforward.blogspot.com/2023/01/monetary-price-controls-and-rationing.html