{kind=link}

This article sheds some light on the monetary myth of inflation control power of the monetary policy pursued at present in Sri Lanka and how it helps business of government and money dealers.

The present CB Governor blames the previous regime for historically high inflation in 2022 as a result of printing of Rs. 250 bn for refinance credit by following modern monetary theory and home grown economic model. However, he also has been effectively pursuing same modern monetary theory, but with a foreign grown economic model prescribed by the IMF.

This article shows that the monetary policy model presently pursued in Sri Lanka has got no inflation control power in the real economy. Instead, the CB uses it for monetary financing of the government and money dealers without any trace over its impact on prices. However, the CB like a parrot talks on price stability and control of inflation at mid-single digit in the medium to long-term.

At the beginning, the CB Governor claimed that inflation would be controlled by shrinking the economy first through higher interest rates and the economy would then be rebuilt with the price stability. This is a highly undemocratic hypothesis that aims to push the people to the poverty trap.

Present Sri Lankan monetary policy model – Key instrumentsThe two key instruments followed at present are given below.

- Policy rates corridor as the target for overnight inter-bank interest rates

Policy rates are the standing deposit facility rate (SDRF) and standing lending facility rate (SLFR). These are the CB’s overnight interest rates applied on its transactions with banks and primary dealers. SDFR is the interest rate paid on overnight deposits held with the CB. SLFR is the interest rate charged on overnight borrowing from the CB against the collateral of government securities. As a result, call money rates or inter-bank overnight interest rates are expected to remain within the policy rates corridor (see Chart 1 below).

For this purpose, the CB should stand ready to lend or accept deposits at policy rates without limits. Therefore, this is not different from the maximum price and floor price imposed on certain goods. Accordingly, policy rates set the target for the inter-bank interest rates volatility.

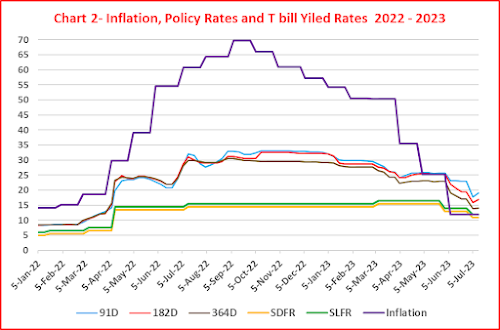

As such, the primary monetary policy decision taken from time to time is the setting of policy interest rates, i.e., hike or cut or unchanged. At preset, SDFR and SLFR are 11% and 12%, respectively, from 6 July, 2023.

The CB claims that policy interest rates are pursued for controlling the inflation at a target of 4%-6%, which is rhetorically called as flexible inflation targeting monetary policy framework.

- Statutory reserve ratio (SRR)

This is the portion of deposit liabilities of commercial banks that should be kept with the CB. At present, it is 4%. This is intended to limit lending of banks and the CB does not pay any interest on these deposits whereas a penal rate of 36.5% is charged on the amount in the short of SRR. However, SRR is not an active monetary policy instrument.

Is this monetary policy model credible? No

This model is flawed in controlling inflation or maintaining the price stability due to several lapses. Six of them are presented blow.1. No link is established between policy rates, inter-bank overnight interest rates and determination or movements of prices of goods and services.

Central bank economists believe a transmission mechanism of policy interest rates to affect prices through bank credit/financing conditions and demand for goods and services over a period of 12-18 months to control inflation as they wish.

Further, their direct impact on the supply side through the cost of production and investments is well known to have counter effects on monetary policy goals although central banks are ignorant of such effects on theoretical grounds.

However, despite modern economic research, nobody has any acceptable research findings on this transmission and its roots and lags except talking. Modern economies are not static systems to find such monetary transmissions to demand, prices and inflation.

However, all text books teach students that inflation is a monetary phenomenon that can be controlled only by central banks through the monetary policy/interest rates. Political leaders for their political benefits tell the public that inflation is a matter for the central bank who is independent to do that. However, the public punishes the political leaders for unbearable inflation as they are not aware of central banks’ inflation control story.

2. New OMO rule has invalidated the monetary policy principle.The corridor-based monetary policy principle is the unlimited access to finance at policy interest rates. However, the CB has restricted SDFR and SLFR windows effective from 16 January 2023, i.e., SDFR only five days a month and SLFR only up to 90% of the SRR at any date for a bank. This is no different from rationing imposed at controlled prices. In general economics, the rationing should lead to the black money market. Therefore, the CB’s present monetary policy model has collapsed in its principle concept.

As banks are reluctant to lend their excess funds in the inter-bank due to current stability concerns and acute shortage of liquidity together with black market developments, overnight inter-bank interest rates tend to move beyond the SLFR. Therefore, the CB has commenced injecting new liquidity lavishly through reverse repo auctions on a daily basis in order to neutralize the cap on SLFR access. In most cases, banks receive reverse repo funds at interest rates lower than SLFR and, therefore, they are now better off at costs to public funds.

From January 2023, the total injection through reverse repo auctions until the end of the last week is Rs. 3,490 bn as against the auctioned amount of Rs. 4,715 bn. In addition, multi-billions are offered for during-the day-settlement free of interest (intra-day liquidity facility).3. Inflation target is an annual statistical exercise not practical for measurement of price stability.

Central bank economists use the year-on-year percentage change of the consumer price index (CPI) as the inflation indicator for the monetary policy. This is the percentage increase of the current month’s CPI over the same month’s CPI in the last year. Therefore, this is a statistical estimate driven by the base effect, i.e., the level of the last year’s CPI as the denominator. The inflation number rising so fast in 2022 up to September and falling so fast from May 2023 are largely a base effect phenomenon as the current CPI marginally rises or remains unchanged.

As such, inflation in Sri Lanka is like to fall to zero towards the end of 2023 and possibly negative in early 2024 if prices of basic food items are to fall.

Therefore, the CB has commenced cutting policy interest rates by celebrating the victory of the return of the statistical annual inflation towards their target of 4%-6%. However, this is a meaningless policy as the general public continues to suffer from prices that rose or more than doubled in 2022. I do not understand why internationally trained CB’s economists do not grasp this simple fact on prices understood by any man on the road.

4. Inflation is the phenomenon of rising prices over a period affecting the cost of living and real income of the general public.

To the general public, inflation is a phenomenon of rising prices over a longer period, not a 12-month period. Prices and CPI in Sri Lanka commenced rising since early 2020 due to a composite of factors. Accordingly, the general price level represented by the CPI basket in June 2023 is roughly 86% higher than that at the end of 2019. Therefore, prices of consumer essentials confronted by the general public at present are almost twice to thrice the prices that prevailed prior to the present inflation waive.

However, the CB who believes statistical annual inflation has so far cut policy interest rates twice in total of 4.5% by celebrating the inflation rate fallen to 12% in June 2023 from its peak of 69.8% in September 2022 together with a forecast of falling it further to mid-single digit at the end of 2023 than anticipated.

Therefore, the CB pursues its monetary policy on a myth of inflation and price stability that does not serve the general public.5. Policy rates cannot resolve supply side bottlenecks and costs that have caused the inflation.

The present waive of inflation in Sri Lanka as well as in the globe is a phenomenon connected with supply side bottlenecks and cost push. In Sri Lanka, its major was the grave market uncertainties caused by political and social instability seen in 2022.

However, central banks attempt to control rising prices by raising interest rates to suppress the demand side of the economy in line with tribal monetary concepts. Therefore, policy interest rates cannot resolve present inflation problem. That is why even after 18 months of consecutive hikes of policy interest rates by 10-20 times, central banks even in developed market economies still continue to raise interest rates as inflation is not tamed sustainably.6. Setting policy interest rates is highly arbitrary and not economically justifiable.

The CB like all other central banks moves policy interest rates here and there without any justification for the specific level or change. However, they talk about various sectoral economic statistics to pretend that policy rates have been determined macroeconomically on both domestic and global fronts.

The CB raised policy interest rates by 7% to 13.5% – 14.5% in April when the annual inflation rose to 18.7% in March by predicting of an inflation of around 30% in the near future. Further, policy rates were raised by another 1% in July 2022 (14.5% – 15.5%) when inflation was rising towards 70%. However, it raised interest rates by 1% in March 2023 (to 15.5% – 16.5%) when inflation was falling to 50% after peaking at 69.8% in September 2022.

In contrast, the economic rationale for policy rate cuts of 2.5% in May 2023 when the inflation was 25.2% and of 2% in July 2023 (to present 11% – 12% level) when inflation was drastically fallen to 12% with a forecast of mid-single digit at the end of the year cannot be established (see Chart 2 below). Inflation forecasts have been consistently false and the CB itself does not accept its forecasts.

Therefore, the policy rates are merely arbitrary exercises that cannot be established in statistics or in macroeconomics.

Concluding Remarks

- Some political leaders and economists think that policy interest rates-based monetary policy is a God-given formula to control inflation at levels they wish. Central banks think that changes in policy rates work like a rocket science to affect prices as they wish to keep inflation at targets. However, above points shows that all these are tribal misconceptions.

- If those beliefs are correct, the world from the beginning of 2022 would not have confronted the present four-decades-high inflationary pressures in front of inflation controlling central banks. Further, they have been trying to control inflationary pressures by raising policy interest rates in a range of 10 to 20 times, but even annual statistical inflation does not seem to be turning back towards the targets in a sustainable manner.

- Raising policy rates in countries like Sri Lanka caught by a foreign currency and debt crisis consequent to flawed monetary policies pursued in the past two decades in old fashion demand management concept is unjustifiable. It will push these countries to decades of economic crises and a new round of poverty and social unrest.

- In fact, what the CB has been engaged in is the implementation of the same modern monetary theory although the CB Governor blames the past regime. This is revealed from the excessive money printing for monetary financing through the direct purchase of Treasury bills by the CB. At present, CB’s Treasury bill holding is Rs. 2,539 bn at face value which is an increase of Rs. 689 bn or 37.2% since his appointment on 7 April 2022. Accordingly, nearly 70.4% of the CB’s assets now are lending to the government. Therefore, CB’s new monetary operations are nothing but modern monetary theory. If so, the present monetary policy also will not be able to resolve inflationary pressures underlying the economy although the CB celebrates the unexpected fall of annual or year-on-year inflation towards the mid-single digit.

- As such what the CB is actually and actively engaged in by talking of inflation control and stabilization of the economy is a day-to-day printing of money to fund the government and dealers to help their liquidity management which is good during normal times but not in crisis times.

- Therefore, I feel sorry for the general public whose tax money was spent for providing education to those monetary and fiscal policy bureaucrats who have no new ideas except going after the tribal concepts and IMF model like parrots to rescue the country from the present crisis created by themselves. That is because they have secured academic qualifications by memorizing theories and have got no common sense in business activities.

- At least, political leaders must force the CB to bring the price stability back to the pre-crisis level in terms of the CPI so that the general public regains the living standards and real incomes. Talking about economic numbers, models and concepts is useless without it.

- Otherwise, political leaders will cause another economic catastrophe if they wait till the CB like the God stabilizes the economy by moving its flawed policy interest rates here and there arbitrarily as highlighted above.

- Therefore, it is the public duty of political leaders representative of the public to distant them from tribal economic concepts such as monetary theory and demand management and to implement a fiscal and monetary package capable of driving the supply and demand sides of the economy on sectoral basis towards higher livings standards of the general public if they are interested in the economic welfare of the general public.

(This article is released in the interest of participating in the professional dialogue to find out solutions to present economic crisis confronted by the general public consequent to the global Corona pandemic, subsequent economic disruptions and shocks both local and global and policy failures.)

P Samarasiri

Former Deputy Governor, Central Bank of Sri Lanka

(Former Director of Bank Supervision, Assistant Governor, Secretary to the Monetary Board and Compliance Officer of the Central Bank, Former Chairman of the Sri Lanka Accounting and Auditing Standards Board and Credit Information Bureau, Former Chairman and Vice Chairman of the Institute of Bankers of Sri Lanka, Former Member of the Securities and Exchange Commission and Insurance Regulatory Commission and the Author of 10 Economics and Banking Books and a large number of articles published.

The author holds BA Hons in Economics from University of Colombo, MA in Economics from University of Kansas, USA, and international training exposures in economic management and financial system regulation)

Source: Economy Forward