January 31, World (LNW): A Pakistani court has sentenced former Prime Minister Imran Khan and his wife to 14 years in prison for corruption, according to prison officials.

This follows a separate conviction the previous day in which another special court found Khan guilty of leaking state secrets, resulting in a 10-year prison sentence.

The corruption charges against Khan and his wife involve allegations of retaining and selling state gifts during Khan’s tenure as the country’s premier.

The court’s decision marks a significant legal development for the prominent political figure, known for leading Pakistan’s Tehreek-e-Insaf (PTI) party and serving as the Prime Minister.

These legal proceedings add a layer of complexity to the political landscape, with implications for Khan’s role and influence within Pakistani politics.

The convictions and sentences are subject to legal processes and may have broader ramifications on the political dynamics of the country.

January 31, Colombo (LNW): The government intends to create 100,000 additional foreign job opportunities for Sri Lankan citizens this year, announced State Minister of Social Empowerment Anupa Pasqual.

The Minister outlined this initiative during a press briefing held at the Presidential Media Centre (PMC) under the theme ‘Collective Path to a Stable Country.’

Recognising the potential of international job markets, the government intends to send 10,000 individuals proficient in the Japanese language to secure employment abroad.

This strategic move aims to leverage existing language skills and tap into new markets, providing lucrative opportunities for the workforce.

State Minister Anupa Pasqual emphasised the government’s commitment to investing in skills development and training programmes to ensure that Sri Lanka’s workforce is well-prepared for the demands of the global job market.

Empowering beneficiaries is the government’s ultimate objective, Pasqual went on, adding that they are moving beyond simply providing financial assistance.

The State Minister further emphasised that the government’s revamped system focuses on creating opportunities for foreign employment, with 10,000 Japanese Language Proficiency Test passers already placed abroad and a further 100,000 foreign jobs targeted.

In addition to enhancing professional skills through targeted training programmes, the government plans to promote the cultivation of high-value crops such as tea, cinnamon, and pepper for export.

This dual approach, combining skill development and export-oriented agriculture, is expected to pave the way for sustainable economic empowerment.

January 31, Colombo (LNW): Vaiyapuri Gopalsamy, better known as Vaiko, the General Secretary of the Marumalarchi Dravida Munnetra Kazhagam (MDMK) and Member of Rajya Sabha, has called upon the Indian government to approach its relationship with Sri Lanka with careful consideration, particularly in light of China’s increasing presence in the island nation, The Hindu reported.

During an all-party meeting chaired by Defence Minister Rajnath Singh in New Delhi, Vaiko emphasised the strategic significance of China’s construction of a port in Hambantota, highlighting the potential threat that could emerge from the south.

In addition to geopolitical concerns, Vaiko drew attention to the alleged attacks on Tamil fishermen by the Sri Lankan Navy, expressing deep concern over the reported fatalities of over 800 fishermen.

He urged the Indian government to address this issue promptly, emphasising the importance of safeguarding the lives and property of Tamil fishermen.

During the meeting, Vaiko also took the opportunity to criticise Tamil Nadu Governor R.N. Ravi, accusing him of making inconsistent remarks on various issues.

Responding to claims that Governor R.N. Ravi attributed India’s independence to Subhas Chandra Bose, Vaiko pointed out the Governor’s clarification and suggested that the Minister may not have been adequately informed on the matter.

Furthermore, Vaiko expressed apprehension about the potential threats to Indian democracy, cautioning against the implementation of policies driven by “Hindutva forces,” such as one country, one election, one language, and one religion, which, according to him, could pose significant risks to the democratic fabric of the nation.

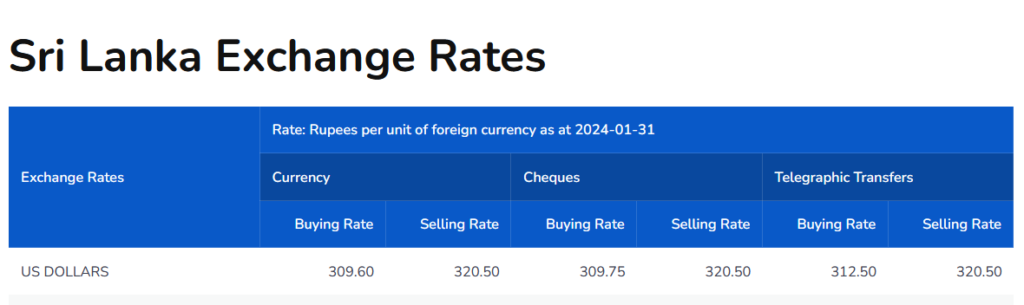

January 31, Colombo (LNW): The Sri Lankan Rupee (LKR) has appreciated against the US Dollar today (31) in comparison to yesterday, as per the exchange rates of leading commercial banks in the country.

At Peoples Bank, the buying price of the US Dollar has dropped to Rs. 310.88 from Rs. 312.35, and the selling price to Rs. 321.71 from Rs. 323.34.

At Commercial Bank, the buying price of the US Dollar has dropped to Rs. 309.60 from Rs. 311.45, and the selling price to Rs. 320.50 from Rs. 321.50.

Sampath Bank follows similar pattern with the buying and selling prices of the US Dollar dropping to Rs. 312 from Rs. 313 and Rs. 321 from Rs. 322, respectively.

January 31, Colombo (LNW): The Police have arrested three additional suspects believed to be involved in aiding and abetting the recent shootings in Beliatta, where five individuals lost their lives.

Two suspects were taken into custody in the Hungama Police Division, while the third suspect was apprehended in the Matara Police Division on Monday (29), according to Police.

The arrested individuals, aged 28, 42, and 58 years, are residents of Negombo, Alawwa, and Boossa, respectively.

The police assert that these suspects played a role in disposing of the T-56 firearm used in the shootings and were also involved in financial transactions related to the incident.

All three suspects have been handed over to the Beliatta Police for further investigations into the tragic events that unfolded on January 22, 2024, resulting in the deaths of five individuals, including Saman Perera, the Leader of the ‘Our Peoples Party’ (Ape Jana Bala Pakshaya).

January 31, Colombo (LNW): In a continued effort to combat drug-related activities, the Police Special Task Force (STF) has arrested an additional 729 suspects in the ongoing islandwide special operation known as ‘Yukthiya.’

The Ministry of Public Security reported that the arrests took place during multiple raids conducted within the last 24 hours, concluding at 12.30 am today (31).

As part of these operations, law enforcement authorities also seized various narcotics, including 146 grams of heroin and 119 grams of crystal methamphetamine aka ‘ICE’.

Launched in December of the previous year, the ‘Yukthiya’ special operation aims to curtail and eliminate drug-related activities within Sri Lanka.

The recent arrests contribute to the sustained efforts of the STF in addressing the complex issue of narcotics trafficking and related crimes.

January 31, Colombo (LNW): Sri Lanka Telecom (SLT) witnessed a significant change in its Board composition as Board members submitted their resignations.

This move comes in response to President Ranil Wickremesinghe’s recent directive to the Treasury Secretary to promptly reconstitute the SLT Board.

In an official disclosure to the Colombo Stock Exchange (CSE) on the matter, SLT PLC informed that Chairman and Independent Non-Executive Director Reyaz Mihular tendered his resignation, effective from January 29, 2024.

Additionally, five other Directors, namely Rohan Fernando (former SLT Chairman), Lalith Seneviratne, Ranjith Rubasinghe, Mohan Weerakoon, and Treasury representative K.A. Vimalenthirarajh, submitted their resignations in a separate filing to the CSE.

Notably, Rohan Fernando also stepped down as Chairman of SLT Subsidiary eChanneling PLC.

On January 26, under the directive of President Wickremesinghe, Secretary to President Saman Ekanayake announced the appointment of a new set of Board Directors for SLT.

The newly appointed members include K.D.D.D. Arandara (Chairman), Dr. K.A.S. Keeragala, Attorney-at-Law Dinesh Vidanapathirana, Prof. K.M. Liyanage, Dr. D.M.I.S. Dassanayake, and Chathura Mohottigedara as the Treasury Representative.

According to reports, this restructuring stems from the government’s concerns over SLT-Mobitel’s legal challenge against the proposed merger between telecom giants Dialog Axiata and Airtel.

January 31, Colombo (LNW): Measures are underway to introduce a minimum speed limit on expressways to address safety concerns arising from slow-moving vehicles, Transport Minister Bandula Gunawardena announced.

During the weekly Cabinet briefing, the Minister highlighted that while a maximum speed limit of 100 kmph is currently in place, there is no established minimum speed.

Gunawardana emphasised that many accidents occur when vehicles attempt to overtake slow-moving ones.

To mitigate such incidents, he stressed that implementing a minimum speed limit on expressways is important.

He disclosed that consultations with experts in the field and relevant institutions, including the police, have taken place to address expressway accidents comprehensively.

The Minister further revealed that new rules and regulations pertaining to expressway safety will be officially published in a gazette notification within the next two weeks.

January 31, Colombo (LNW): The current high-tax regime backed by the International Monetary Fund (IMF) could potentially exacerbate the growth of the informal economy, impeding economic recovery and constricting the tax base in Sri Lanka, leading advocate of free-market capitalism, Dr. Tom G. Palmer, Executive Vice President (International Programmes) at the Atlas Network, warned.

Speaking at a panel discussion during the Economic Freedom Summit organised by the Advocata Institute in Colombo, Dr. Palmer highlighted the experiences of nations emerging from debt crises.

He noted that countries successfully recovering from such crises often embraced simplified, low tax rates, diverging from the high tax rates prescribed by the IMF.

Dr. Palmer cited Greece as an example where a bold rejection of IMF-prescribed high taxation contributed to a thriving economy, particularly in the tourism sector.

The result was an expanded tax base and increased tax collection. Similarly, war-torn Ukraine opted for a flat tax rate, moving away from a complex ‘optimised tax rate,’ ultimately curbing the influence of corrupt oligarchs.

Encouraging the Sri Lankan government to take a bold stance in negotiations with the IMF on taxation, Dr. Palmer emphasised that a lower tax rate should be coupled with digitisation and a reduction of bureaucratic inefficiencies in the public sector to combat corruption.

Drawing parallels with the transformation of Georgia’s entire police force within three months, Dr. Palmer underscored the potential impact of bold policies and decisive actions.

He suggested that such measures, when implemented, could yield positive and desired results for Sri Lanka’s economic landscape.

January 31, Colombo (LNW): Media and civil society organisations have jointly appealed to Speaker of Parliament Mahinda Yapa Abeywardena, requesting careful consideration before endorsing the recently passed Online Safety Bill.

Expressing concerns about potential violations of freedom of expression and constitutional principles, the collective urged the Speaker to ensure full compliance with the directives issued by the Supreme Court.

In a letter addressed to Speaker Abeywardena, the Media, Civil Society, and Trade Union Collective to Rise against Oppressive Laws emphasised the need for a thorough examination of the legislation.

The letter highlighted the perceived haste in passing the Bill on January 24, without adequate discussion with stakeholders and, notably, without incorporating the Supreme Court’s directives.

The collective, representing various media and civil society groups, contested the parliamentary process, with opposition MPs asserting that the Bill was passed without due consideration of the amendments and guidelines mandated by the Supreme Court.

These directives had emerged from a series of 45 fundamental rights petitions challenging the draft Bill.

Expressing concern that such a scenario might constitute a violation of the Constitution, undermining the sovereignty of the people and potentially leading to contempt of court, the collective voiced strong objections to the legislation.

They emphasised their commitment to continuing the fight against regulations that impede freedom of expression and potentially harm the economy.

The groups accused the government of expediting the passage of the Online Safety Bill to counter opposition ahead of upcoming elections.

They urged Speaker Abeywardena to uphold his responsibility in ensuring parliamentary orders are followed, insisting on the incorporation of Supreme Court-directed amendments into the Bill before granting his approval.

As citizen activists and proponents of democracy, the collective respectfully requested Speaker Abeywardena to withhold consent to the Bill until full satisfaction that the Supreme Court’s orders and guidelines are seamlessly integrated.

The letter signifies their dedication to defending democratic values and safeguarding the right to free expression against regulations they deem detrimental to both democratic principles and economic well-being.

")