Colombo (LNW): A new Gazette notification has been released detailing updates to the fees associated with National Identity Card (NIC) services.

Minister of Public Security, Tiran Alles, has announced these changes under the Registration of Persons Act, No. 32 of 1968.

The updated charges are as follows:

The fee charged for the issuance of a certified copy of an NIC fixed at Rs. 1,000.

The fees for the certification of authenticity of the particulars relating to an NIC:

– Online submissions made through the Registration of Persons Department’s website – Rs. 25. – Submissions made by way of a physical document or electronic means acceptable to the Commissioner General – Rs. 500.

The fee for the registration of a person as a photographer, under the Act raised from Rs. 10,000 to Rs. 15,000.

The annual fee for the renewal of a Certificate of Registration increased to Rs. 3,000.

Colombo (LNW): The Customs, Inland Revenue and Excise Trade Union Collective voiced concerns, asserting that ad-hoc policy shifts and questionable methodologies used in policy revisions, pose a threat to the crucial role played by these departments in Government revenue collection.

Issuing a statement, unions argue that these efforts undermine the Government’s ability to fund essential services such as free education and healthcare.

Representatives from the union, which oversees the Customs, Inland Revenue, and Excise Departments, contend that despite being State-run entities operating following Government policy, certain factions are disseminating baseless claims to wipe out these institutions.

They further highlighted that proposals put forth by the three revenue-collecting organisations to enhance revenue and efficiency during the economic crisis, have been disregarded by higher authorities within the Government, signifying a lack of concern for public interests.

The Inland Revenue Department’s outstanding achievement in collecting a record-breaking Rs. 1,229 billion as of 19 October compared to Rs. 653 billion in the same period last year, was cited as evidence of the departments’ dedication to their crucial role.

Despite the challenging economic landscape, the Government has yet to address internal issues within the revenue-collecting organisations, opting instead to convey concerns to the international community.

They alleged that the Commissioner General position of the Inland Revenue Department has been vacant since 27 August 2023, and has hampered the full implementation of policies required to reach Government targets by the end of the year.

Despite import restrictions on over 1,000 items as of mid-October 2023, union representatives said the Customs Department outperformed the Rs. 695 billion collected in the first nine months of 2022, by collecting Rs. 715 billion and was confident the department would make significant collections by year’s end.

“The original income targets for the Excise Department undergo numerous alterations during the year, due to a lack of a structured methodology.

Additionally, there have been significant revenue losses as a result of increased alcohol prices. The problem has been made worse by businesses’ misuse of stickers introduced to prevent smuggling foreign liquor to the country and to stop selling adulterated liquor to the customers and further increase its revenue,” they disclosed.

Despite these difficulties, they said the Excise Department was still able to collect Rs. 137.1 billion (excluding court fines) as of 15 October 2023, up from Rs. 134.6 billion during the same period in 2022.

They observe these circumstances as a conspiracy to erode the significance of these State institutions and demoralise the three departments.

However, the Union representatives reiterate their commitment to contributing to economic prosperity and emphasise the need to broaden their responsibilities to overcome difficulties, to ensure access to services for the public like free education and healthcare.

Colombo (LNW): At the time of Chinese research ship docking at the Colombo Port on Wednesday the US Department of Defence to the US Congress claims that China is considering using Sri Lanka as part of its global military supply chain.

The report by the US Department of Defence to the US Congress is titled “Military and Security Developments Involving the People’s Republic of China.”

The report notes that the People’s Republic of China probably also has considered 18 countries including Sri Lanka as locations for People’s Liberation Army’s military logistics facilities.

It added that the PRC is seeking to expand its overseas logistics and basing infrastructure to allow the PLA to project and sustain military power at greater instances.

If realized, a global PLA military logistics network could disrupt U.S. military operations as the PRC’s global military objectives evolve.

The report says that beyond the PLA support base in Djibouti, the PRC is very likely already considering and planning for additional military logistics facilities to support naval, air, and ground forces projection.

The report also revealed that in June 2022, a PRC official confirmed that the PLA would have access to parts of Cambodia’s Ream Naval Base.

Chinese research ship docked at a Sri Lankan port on Wednesday, likely adding to neighboring India’s concerns about China’s growing influence in the Indian Ocean.

The arrival of the Shi Yan 6 follows last year’s visit by a Chinese naval vessel.

The latest ship was given permission to dock for replenishment at the port of Colombo, the Indian Ocean island’s main port, from Wednesday until Oct. 28, said foreign ministry spokesman Kapila Fonseka.

The vessel had been expected to conduct research with Sri Lankan state institutions, but Fonseka said permission was granted only for replenishment and no research work would be carried out.

According to Chinese television network CGTN, Shi Yan 6 is a geophysical scientific research vessel on an expeditionary voyage in the eastern area of the Indian Ocean.

Organized by the South China Sea Institute of Oceanology under the Chinese Academy of Sciences, the vessel is scheduled to operate at sea for 80 days, covering a range of more than 12,000 nautical miles (roughly 22,200 kilometres), CGTN reported.

China has been trying to expand its influence in Sri Lanka, which is located on one of the world’s busiest shipping routes in what India considers part of its strategic backyard.

Beijing was once widely seen as having an upper hand with its free-flowing loans and infrastructure investments. But Sri Lanka’s economic collapse last year provided an opportunity for India as New Delhi stepped in with massive financial and material assistance.

Colombo (LNW): Union Bank now comes under CG Capital Partners Global Pte. Ltd indirectly as it as brought Culture Financial Holdings Ltd. (a substantial shareholder of shares in Union Bank a majority stake of the bank.

This was announced in December 2022. On 24 October 2023, the Board of Directors of Union Bank received formal notification that the transaction has been completed and the Colombo Stock Exchange (CSE) has been notified of the same.

Through its ownership in Culture Financial Holdings, CG Capital Partners Pte Ltd., is now the main shareholder of Union Bank.

CG Corp Global (CG) takes pride as one of the leading conglomerates in Asia with over 160 companies and 123 brands in the global market with the strength of more than 15, 000 employees.

It is a major player in many industries such as banking and finance, hospitality, cement, hydropower, telecommunication, and education.

The company is a major player in the financial services sector in Nepal and Nabil Bank where it is the largest shareholder and is listed as the largest private bank in the Nepalese Stock Exchange.

This is not the first time CG has set its sights on Sri Lanka. It holds major shares in several high-end properties, luxury hotels and resorts across the country and is further expanding its investments towards the financial services sector as well.

This comes as a reaffirmation of its commitment to Sri Lanka, by being a source of support and strength during these challenging and transitioning times, whilst reiterating the foreign investor confidence in Sri Lanka.

This is a major milestone for Union Bank to have such an international powerhouse as the main shareholder.

Dr Binod K. Choudhary, Chairman of CG Corp Global said, “This is a major investment towards the financial service sector in Sri Lanka and to Union Bank.

The Bank has had a strong track record and has further potential to grow and do greater things to achieve more milestones in the banking sector.

“We are taking a strategic growth approach to make Union Bank to be amongst the top private commercial banks in Sri Lanka” he added.

This growth expansion could see further consolidations and acquisitions. The acquisition and transition of Nabil Bank to become Nepal’s largest bank is a fine example.

Based on CG’s core competencies and expertise, we want to also look at the possibility of Union Bank’s expansion to emerging and frontier markets such as Africa, Nepal, and Bhutan.

It is great to be associated with this well-reputed and well capitalised bank in Sri Lanka. I believe, together much can be done as we move forward, he claimed.

Colombo (LNW): Minister of Power and Energy, Kanchana Wijesekera, announced that a comprehensive proposal pertaining to the restructuring of the Ceylon Electricity Board (CEB) is scheduled for submission to the Cabinet next week.

SrI Lanka government will be introducing a mechanism immediately for a systematic approach to revise the electricity bill once every six months. Minister of Power and Energy, Kanchana Wijesekera disclosed.

A cost effective electricity tariff formula is to be devised using mathematical models and data processing in consultation with energy experts in the country.

The formula will be a complex one as it has to determine the tariff for several segments of electricity users without any discrimination and reasonable manner taking into account all cost factors in energy generation.

These factors include, fuel prices, cost for a unit of power generation, energy mix, taxes, rupee fluctaions against the dollar, overhead costs , etc.

Minister Wijeskera said that all these factors will be made known to the public along with the fuel formula mechanism after its finalization soon.

The Minister providing additional insights remarked that the Public Utilities Commission had recently approved a revision of electricity tariffs for the Electricity Board.

Consequently, preparations we made to implement an approximate 18% rate adjustment, effective from the 21st of October, with subsequent rate evaluations for the coming months, he added.

This price revision adheres to the government’s policy framework established in conjunction with the International Monetary Fund (IMF).

Pursuant to this framework, no state enterprise is permitted to draw funds from the Treasury to cover its financial losses.

Addressing a prevalent misconception within society, the Minister clarified that the Electricity Board is not confined to revising tariffs only twice a year.

Provisions are in place for tariff adjustments in cases of emergency and the necessary cabinet approval has been secured for this purpose.

“As of today, we are utilizing only 65.81% of the reservoir capacity, a stark contrast to the 84.41% capacity utilization observed by October 22, 2022. This represents a considerable 20% decrease.

Comparatively, the hydroelectricity production from our reservoirs in 2022 reached 5,364 gigawatt hours, a significant decline from 5,639 gigawatt hours in 2021.

By October 22, 2023, the figure stands at 2,893 gigawatt hours, only half of the corresponding output in the preceding years. With a mere 70 days remaining in the year, there is uncertainty regarding our ability to meet these targets.

Consequently, the exploration of alternative measures is imperative to ensure the continued supply of electricity, he said.

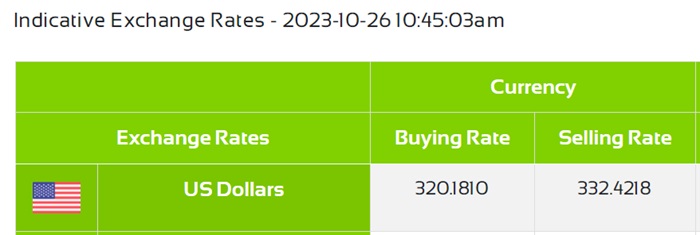

Colombo (LNW): The Sri Lankan Rupee (LKR) happens to be fluctuating against the US Dollar today (26) compared to yesterday, as per leading commercial banks in the country.

At Peoples Bank, the buying price of the US Dollar has dropped to Rs. 320.18 from Rs. 320.91, and the selling price to Rs. 332.42 from Rs. 333.18.

At Commercial Bank, the the buying price of the US Dollar has increased to Rs. 320.16 from Rs. 318.50, and the selling price remains unchanged at Rs. 33.50.

At Sampath Bank, the buying and selling prices of the US Dollar remain steady at Rs. 322 and Rs. 332, respectively.

Colombo (LNW): Former Commander of the Sri Lanka Army and respected Senior Officer, Gen. L P Balagalla RWP RSP VSV USP ndc IG has passed away in Army Hospital, Colombo.

His funeral arrangements will be notified later.

Balagalle pursued medical studies before enlisting in the Ceylon Army as an Officer Cadet on 5 April 1965. After undergoing training at the Army Training Centre in Diyatalawa, he earned his commission as a second lieutenant in the 4th Regiment, Ceylon Artillery on 5 April 1967.

Participating in counter-insurgency efforts during the 1971 JVP Insurrection, Balagalle later trained at the Indian Army School of Artillery in Deolali between September 1971 and February 1972.

He revisited the institution between August 1977 and September 1978 for advanced training and earned his qualification as an Instructor Gunnery (IG).

After completing the Intelligence Staff Officers Course in Pune between August and October 1975, Balagalle took on roles within military intelligence during the 1980s.

Holding the position of General Staff Officer and later the Principal Staff Officer of the Joint Operations Command as a major, he significantly influenced the Vadamarachchi Operation and the quelling of the 1987-1989 JVP uprising. In 1989, he furthered his education in the UK, attending the Intelligence Security Administration Course.

Promoted to lieutenant colonel, Balagalle held pivotal positions, becoming the inaugural Director of Military Intelligence and Commanding Officer of the Military Intelligence Corps from 1990 to 1994. He took charge of the 4 Brigade, the Artillery Brigade, and Area Headquarters Wanni in 1994. In 1996, he attended the National Defence College.

After being promoted to major general, Balagalle led multiple divisions and undertook several military operations. He was soon appointed Deputy Chief of Staff and subsequently Chief of Staff of the Army, also serving as Colonel Commandant of the Military Intelligence Corps between 1997 and 1998.

On 24 August 2000, Balagalle was promoted to lieutenant general and assumed the role of Commander of the Sri Lankan Army, marking him as the first officer to receive local training at the Army Training Center and then rise to this rank. Under his leadership, Sri Lankan troops began participating in UN peacekeeping missions.

Furthermore, he played a crucial role in establishing the Institute of Peace Support Operations Training in collaboration with the US Army Pacific Command.

On 10 October 2003, Balagalle was appointed as the Chief of the Defence Staff (CDS), becoming the first active Army Commander in Sri Lanka to hold this role. As CDS, he notably became the first foreign military leader to visit the line of control post the ceasefire agreement between India and Pakistan.

His service also saw him attending major defence conferences in Hawaii and Singapore. Lieutenant General Shantha Kottegoda succeeded him as the Commander of the Army on 30 June, but Balagalle continued as CDS until his retirement on 1 September 2005, achieving the rank of general.

Colombo (LNW): Seylan Tikiri, a distinguished Children’s Savings brand in Sri Lanka, is delighted to unveil its recent partnership with the Wildlife and Nature Protection Society (WNPS) to organise a trip to the Elephant Transit Home (ETH) in Udawalawe.

Crafted to enchant the Society’s Young Explorers, this outing was aimed at fostering a love for nature and wildlife.

The day kicked off with an enlightening talk by the devoted vets at ETH, offering the young attendees invaluable knowledge about elephant behaviour and the admirable efforts at the transit home.

The young explorers were subsequently escorted to the veterinary facility, where they had the unique opportunity to observe two critical treatment procedures, shedding light on the care and commitment essential to safeguard these magnificent animals.

A standout moment was the touching experience of feeding the baby elephants, an activity that the children found deeply engaging, underscoring the significance of conservation and fostering a sense of compassion for animals.

Demonstrating their commitment to community involvement, the children took part in a community service task, cleaning the ETH car park, thus instilling values of environmental care and teamwork.

The day concluded with an afternoon tea, organised by the children in honour of the vets, staff, and volunteers at the Elephant Transit Home, a gesture underscoring the importance of collective efforts in wildlife conservation and recognising the dedication of those championing wildlife protection.

This event further showcases the fruitful collaboration between Seylan Tikiri and WNPS. As a leading junior savings brand, Seylan Tikiri is dedicated to presenting children with unforgettable experiences through creative educational initiatives.

In today’s digital era, this excursion offered a special chance for children to engage with nature, emphasising the importance of conservation and environmental responsibility.

True to its ethos, Seylan Tikiri is dedicated to orchestrating diverse events year-round for the Tikiri Kids’ benefit. These activities not only inspire positive behaviours but also offer precious experiences during their formative years, all the while championing savings.

Parents keen to offer their children a host of advantages, from bonus interest to gift vouchers, are encouraged to set up a Tikiri account for those under 15. To get started, visit the nearest Seylan Bank branch or ring 200 88 88.

SLPP MP Namal Rajapaksa says the recent Cabinet reshuffle is a mere change of posts & not an effective solution for the country’s problems: asserts it’s the state’s responsibility to ensure that a mechanism is in place for discussions to be held with all political parties involved in the decision-making process when running a coalition Govt such as the incumbent administration.

State Finance Minister Ranjith Siyambalapitiya says 7 vehicles that were suspected to have been imported using electronic vehicle import licenses given to migrant workers, were taken into custody by the Customs: investigations commence to find the other vehicles suspected to have been sold in a similar manner.

Minister of Power and Energy Kanchana Wijesekera says Cabinet has granted approval to develop 200 MW of Floating Solar on the Samanalawewa reservoir: expressions of Interest to be called for 2 projects of 100 MW each from international and local developers to invest in these floating solar power plants.

Foreign Ministry says the Chinese research vessel “Shi Yan 6” is scheduled to arrive at the Colombo Port today for “replenishments”.

State Minister of Women and Child Affairs Geetha Kumarasinghe says 168 girls under the age of 16 were reportedly sexually abused, in September’23.

State owned Milco company’s Chairman Renuka Perera held hostage at the company’s head office: 13 employees arrested by the Police in this regard.

Govt removes one-time high level LTTE operative Emil Kanthan from the list of “proscribed” persons & organisations: gazette to this effect published by Defence Secretary (retd) General Kamal Gunaratne.

Cabinet gives approval to amend the Shop and Office Act to empower women to work during night-time hours: aim of amendment to provide more opportunities for women, particularly women working in information technology.

SJB “economic guru” MP Harsha Silva says domestic & international debt restructuring mechanisms must be comparable: pledges to fight to ensure the EPF will receive any benefits offered to international creditors if the economy grows above IMF predictions: prior to April’22 however, Silva was at the fore-front calling for restructure of SL’s sovereign debt, free-floating of LKR, raising of taxes, and a tight IMF programme.

Samitha Dulan wins the Silver medal in the Men’s Jevelin throw (F64), Janani Dhananjana wins Silver in the Women’s Long Jump event (T47), Kumudu Priyangika wins Bronze in the Women’s Long Jump event (T47), & Palitha Bandara wins Bronze in Men’s Shot Put (F63) at the Asian Para Games 2023.

Colombo (LNW): The U.S. Agency for International Development (USAID) has partnered with Gunadamin Elephant House, a division of Ceylon Cold Stores PLC, to create Sri Lanka’s first plastic recyclable collection network and material recovery facility, focusing on women’s involvement.

Launched in Dickwella, Matara, the initiative has so far collected 1,175 kilograms of plastic waste and aims to expand across five coastal provinces.

The initiative empowers economically disadvantaged women from fishing communities, turning them into key plastic collectors.

Women are trained, equipped, and then compensated for collecting recyclable plastics and metals. Viridis manages the recycling process.

This approach not only boosts environmental conservation but also promotes women’s active roles in the community and supports a shift towards a circular economy in Sri Lanka.

Full Statement:

The United States, through the U.S. Agency for International Development’s (USAID) Ocean Plastics Reduction Activity, and Gunadamin Elephant House of Ceylon Cold Stores PLC (CCS) have solidified their alliance through a Memorandum of Understanding. This collaboration aims to establish Sri Lanka’s inaugural plastic recyclable collection network and material recovery facility, led by women, emphasising the separation and processing of recyclable materials.

Initially launched in Dickwella, Matara, this partnership, supported by Soba Kantha Environmental Management and Community Development Foundation and Viridis Pvt Ltd, a leader in Sri Lankan plastic recycling, has successfully gathered 1,175 kilograms of plastic waste. The goal is to broaden the initiative’s scope across five coastal provinces, partnering with grassroots women’s organisations. These partnerships aim to identify and empower economically disadvantaged women from fishing communities, transforming them into active plastic collectors and environmental stewards.

“The United States, through its longstanding relationship with Sri Lanka, believes in the transformative power of collaboration,” remarked Christopher Powers, Director of the Office of Economic Growth, USAID Sri Lanka and Maldives Mission. “This partnership epitomises that belief, promising not just environmental conservation but also championing women’s roles in leading the change.”

Daminda Gamlath, President Consumer Foods Sector, John Keells Holdings from CCS conveyed, “Gunadamin Elephant House’s unwavering commitment to responsible plastic disposal and waste management initiatives has garnered recognition within the community. Through this visionary partnership, our aim is not only to enhance our efforts in plastic collection but also to empower women, fostering a resilient and environmentally conscious Sri Lanka. This collaboration represents a unique and powerful synergy that exemplifies the potential for positive change when sustainability and women’s empowerment join forces.”

As part of the initiative, women identified as potential recyclable collectors are trained and equipped to safely gather specific types of waste — plastics and metals that have the potential for profitable recycling. With the backing of Ocean Plastics Reduction, Gunadamin Elephant House and Viridis, these women are provided with essential tools, such as gloves, scales, and collection bags. Grassroots organisations then receive the collected waste at their dedicated collection centers.

Viridis takes the helm during the recycling phase, ensuring that the valuable plastic and metal waste is efficiently processed. In return for their contributions, the women are compensated. This model exemplifies a circular economy: plastics and metals consumed are reintroduced into the value chain, significantly reducing pollution and thereby closing the loop and moving Sri Lanka one step closer to a circular economy. Beyond its environmental benefits, this initiative also strengthens the local economy, as the women’s earnings directly benefit their families and the wider community. Moreover, through their active involvement, these women play a pivotal role in promoting eco-conscious practices within their neighbourhoods.

At its core, this collaboration represents more than mere plastic collection; it’s a strategic shift towards sustainable economies and a conscious effort to position women in sectors from which they’ve historically been sidelined. It builds economic resilience and empowerment pathways for women in communities that need it most.

The USAID Ocean Plastics Reduction Activity, with its five-year focus, is committed to reducing environmental plastics, enhancing solid waste management practices, and magnifying recycling initiatives in both Sri Lanka and the Maldives. This collaboration is emblematic of USAID’s broader mission: championing environmental stewardship while driving socioeconomic empowerment.

With a 150-year legacy, Elephant House is a cherished brand, deeply ingrained in Sri Lankan households, known for its trustworthiness and commitment to societal betterment. Gunadamin Elephant House stands as the Corporate Social Responsibility arm of Elephant House. This project falls under the Waste Management pillar, which, together with the Community and Sustainable Sourcing pillars, forms the holistic approach of Gunadamin Elephant House towards sustainable and responsible practices.

")