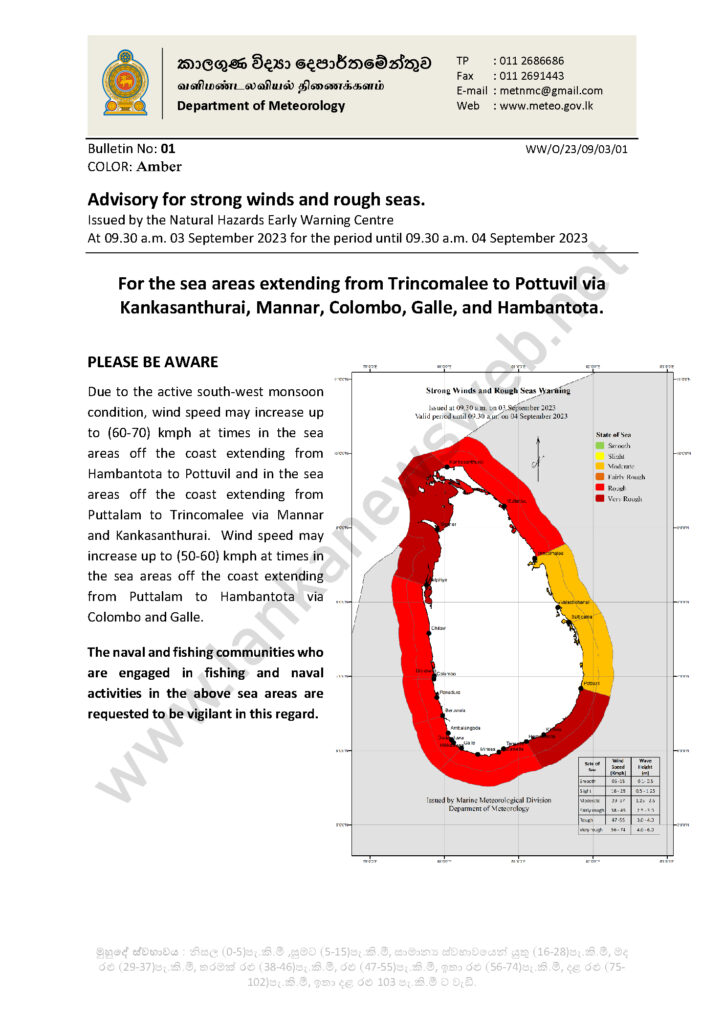

Colombo (LNW): Due to the active South-West monsoon condition, wind speed may increase up to 60 – 70 kmph at times in the sea areas off the coast extending from Hambantota to Pottuvil and in the sea areas off the coast extending from Puttalam to Trincomalee via Mannar and Kankasanthurai, the Natural Hazards Early Warning Centre of the Department of Meteorology said in a warning today (03).

Wind speed may increase up to 50 – 60 kmph at times in the sea areas off the coast extending from Puttalam to Hambantota via Colombo and Galle, the statement added.

The naval and fishing communities who are engaged in fishing and naval activities in the aforementioned areas are urged to be vigilant in this regard.

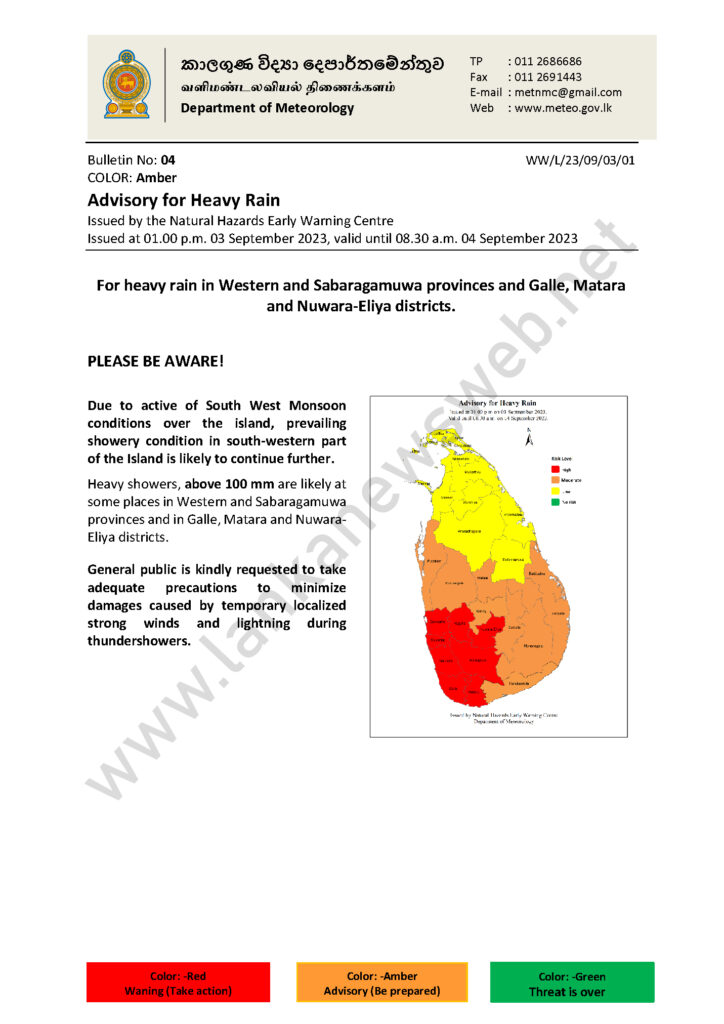

Meanwhile, due to the active South West monsoon conditions over the island, prevailing showery conditions in South Western part of the island is likely to continue further, the Centre said in a separate heavy rain advisory note.

Heavy showers, accordingly, above 100 mm are likely to occur at some places in Western and Sabaragamuwa Provinces and in Galle, Matara and Nuwara Eliya Districts.

The general public is urged to take adequate precautions to minimise damages caused by temporary localised strong winds and lightning during thundershowers.

Colombo (LNW): Sri Lanka in a bid to strengthen its export earnings has opened its second Coconut Triangle in the Northern Province, linking Jaffna, Mannar and Mullativu Districts, announced Plantation Minister Ramesh Pathirana.

The newly established Coconut Triangle will contribute to the coconut export revenue, and subsequently attribute to the varied array of coconut-based products craved by the global market, the Minister emphasised.

Estimates suggest that coconut-related exports this year could yield as much as USD 700 million, and it is expected that coconut exports will pump a US$ 2 billion into the island nation’s forex earnings.

Sri Lanka has a historical reputation of supplying coconut to the overseas market, whilst using two-thirds of the coconut yield for domestic use. In the backdrop, the necessity to optimise export prospects has been identified, thereby reevaluating the distribution for the global market, Pathirana pointed out.

This bold move has been initiated with the overarching goal to reinforce the nation’s position in the global coconut market and spur economic advancement in the Northern region of the island through augmented coconut farming and refinement.

World (LNW): Heath Streak, a Zimbabwean cricketer and cricket coach who played for and captained the Zimbabwe national cricket team, has passed away earlier this (03) morning, his wife confirmed.

Streak has been battling with colon and liver cancer, and passed away in the early hours of this morning, Nadine Streak wrote in a Social Media post.

“In the early hours of this morning, Sunday the 3rd of September 2023, the greatest love of my life and the father of my beautiful children, was carried to be with the Angels from his home where he wished to spend his last days surrounded by his family and closest loved ones. He was covered in love and peace and did not walk off the Park alone. Our souls are joined for eternity Streaky. Till I hold you again,” she wrote.

Singaporeans have chosen Tharman Shanmugaratnam as their next president – but many would have let out a small sigh of disappointment as they did so.

By Tessa Wong

On Friday, the former top minister won a record 70.4% of the votes, comfortably beating two other candidates in the country’s first contested presidential election in more than a decade.

Mr Tharman was always the clear frontrunner. Urbane, well-spoken and intelligent, he is highly regarded by Singaporeans and consistently polls as one of the island’s most popular politicians.

Which was why, when Mr Tharman announced several months ago he was quitting the ruling People’s Action Party (PAP) to run for president, many Singaporeans were baffled by what they viewed as a waste of his potential.

The role of president is a largely ceremonial one that holds little power, apart from having some say on the use of Singapore’s sizeable financial reserves. It has even less say in public affairs – the government, which has the power to remove the president, has made it clear the president cannot speak too freely and has likened the role to the British monarch.

It is a figurehead role that many see suitable for a pleasant, uncontroversial person to inhabit, as has been the case with past presidents. But Mr Tharman is much more than that.

Besides helping to helm Singapore’s political leadership as finance minister and deputy prime minister, the former economist has also held top council positions at global institutions such as the United Nations and the International Monetary Fund (IMF). At one point, he was even tipped to head the IMF.

Some Singaporeans thought that if he ever left the PAP, he would go on to make his mark in the international arena.

Even more hoped he could be prime minister. A survey some years ago saw him poll as the first choice to become PM after incumbent Lee Hsien Loong steps down. In general elections, Mr Tharman’s constituency often scores the highest after Mr Lee’s.

Part of this popularity stems from the fact that as a long-time deputy, Mr Tharman’s reputation has been shielded from the slings and arrows of public criticism which Mr Lee has had to bear.

But the 66-year-old has also cultivated a gentlemanly image, and has refrained from engaging in personal attacks unlike some other politicians. This has played well with an electorate that likes its leaders genteel and statesmanlike.

Many felt he had the chops and stature to become that almost mythical creature – the first non-Chinese prime minister of Singapore – and break a glass ceiling that the government has long insisted is concrete.

Famous for their racial realpolitik, PAP leaders often reiterate that Singapore, a Chinese-majority country, is not ready to accept a minority PM.

Mr Tharman kept mum on this topic until last week when he said he felt Singapore was ready, sharpening the sting of disappointment among his supporters.

But Mr Tharman has also insisted he would not be good at being PM, and with the PAP’s new leadership waiting in the wings, it could be said he was already on his way out. One theory is the PAP wanted him to run for president to help shepherd the next generation of leaders.

And so, he chose to run for president instead. Although Singapore has had non-Chinese presidents in the past, Mr Tharman is the first one voted in by the public.

His supporters could claim his victory as a win for representation and a repudiation of racism. In the lead-up to the election, some social media posts insisted that Singapore must have Chinese leaders. Mr Tharman’s two competitors were both Chinese.

Image caption, Ng Kok Song came in second behind Mr Tharman, with about 16% of the vote

Ironically he has also blown apart the argument for a key PAP racial policy.

Prior to the presidential election in 2017, the government passed laws ensuring some polls would be restricted to minority race candidates. They argued the rules were needed to ensure better representation of minorities in Singapore, which include Malays, Indians, and Eurasians.

Those rules did not apply this time, so Mr Tharman has proven that a minority race candidate can win under their own steam – and resoundingly so.

For this reason, his victory “is certainly a win for race relations” in Singapore, said Mathew Mathews, a principal research fellow specialising in race at the Institute of Policy Studies.

But he added that the results “don’t necessarily mean that Singapore society is race-blind”, as race would likely be a bigger factor in a more even competition. The other candidates had CVs less distinguished than Mr Tharman’s, or were less known.

Questions of influence

As with any election in Singapore, this one was seen partly as a referendum on the PAP, which has suffered rare political scandals recently.

Though Mr Tharman’s landslide win can be largely attributed to his personal popularity which has always outstripped the PAP’s, it also “shows that the party brand is not so toxic such that the association with it drags a person down”, noted Walid Jumblatt Abdullah, an assistant professor in social sciences at Nanyang Technological University.

Still, the victory has also been overshadowed by questions about the PAP’s influence. Mr Tharman was widely seen as the government-backed candidate.

Though he has insisted he will act independently, few believe this to be true of a man who has been one of the PAP’s most loyal team players.

This election also saw renewed disgruntlement over its opaque and restrictive criteria. A potentially popular candidate, George Goh, was disqualified while a more controversial one, Tan Kin Lian, who had been accused of sexism and racism, was let in.

Mr Tharman’s win may have thus deepened the perception that the presidential race is increasingly rigged by the government.

There was even a movement urging Singaporeans to spoil their ballots in protest, though in the end that percentage was around the usual average of 2%, which showed “the overwhelming majority viewed this election worth partaking in and legitimate”, Dr Abdullah said.

Mr Tharman ran on a campaign promising “respect for all”, including “respect for different views and political leanings”.

But it is not certain how he would achieve that as president in a system perceived as perpetuating the PAP’s power – a system he helped to shape for decades.

Colombo (LNW): The Central Bank’s PMI index value for the construction industry stood at 43.2 in July indicating contraction in the building sector.

Survey respondents say tendering opportunities centre on foreign-funded projects, while private clients wait for further price reductions before embarking on new endeavours

Construction firms optimistic about next 3 months, with expectations of economic recovery, drop in interest rates, lower material costs, and ongoing negotiations with Govt.-funded projects

Sri Lanka’s construction industry continued to face headwinds in July 2023, amid lack of new projects with a total activity index value of 43.2.

The Central Bank said industry players have grappled with challenging conditions, but there are glimmers of hope on the horizon.

One notable trend has been the cautious optimism arising from a gradual decline in material costs. While many firms have remained dormant in the face of the industry’s challenges, ongoing projects have found a more conducive environment due to this cost relief.

The Statistics Department of the Central Bank has been conducting the PMI survey for construction activities since June 2017, delivering key industry insights to the Central Bank, assisting the policy formulation process

Additionally, some Government-funded projects, which had been temporarily suspended, cautiously resumed operations on a modest scale during the month. The new orders component showed contraction in July, albeit at a slower rate.

Respondents noted that tendering opportunities primarily revolved around foreign-funded projects, while private clients appeared to be waiting for further reductions in costs before committing to new construction ventures.

Sub-contract openings have also been scarce, as firms with existing projects on hand possess surplus capacities.

On the employment front, firms continued to downsize, retaining only essential staff members. Quantity of Purchases saw a decline as well, as most firms adopted a wait-and-see approach, fulfilling only short-term requirements.

However, there was some stability in suppliers’ delivery time, and some respondents mentioned the increasing availability of supplier credit facilities.

Despite the prevailing challenges, the sentiment among construction firms for the next three months remained broadly positive. Several factors contributed to this optimism include; expectations of an economic recovery, decreasing interest rates, the subsiding of material costs, and ongoing negotiations regarding the recommencement of Government-funded projects that had previously been put on hold.

Responding to rapid changes in the economic landscape of Sri Lanka, Government of India (GOI) has increased the financial allocation for various grant projects being implemented across the length and breadth of the country

Financial allocation has been increased by upto 50% in case of 9 ongoing projects which are being executed under the India-Sri Lanka High Impact Community Development Project (HICDP) framework.

The overall financial commitment for these 9 projects currently stands at close to SLR 3 billion, after the increase. These projects cut across sectors ranging from education and health to agriculture, among others.

GOI has completed more than 60 grant projects under the HICDP framework, covering all the 25 Districts of Sri Lanka. In addition, 20 other projects are under different stages of implementation.

GOI’s overall development cooperation partnership portfolio in Sri Lanka is around USD 5 billion, of which USD 600 million is grant.

Colombo (LNW): Sri Lanka‘s recent proposal by the authorities to impose a minimum room rate on hotels in the city of Colombo has come under criticism of tourism sector stakeholders and economic experts.

This proposal, set to take effect from 1 October 2023, stipulates rates of $ 130 for 5-star hotels, $ 100 for 4-star hotels, and $ 80 for 3-star hotels.

While the authorities argue that this measure aims to counter underpricing by higher-tier hotels, Advocata economic think tank warned the policy threatens to undermine the growth and vitality of the tourism sector.

“It places an unnecessary burden on hoteliers already grappling with the challenges posed by the global pandemic and subsequent economic crisis. Further, it undermines the country’s competitiveness in the regional tourism market,” it added.

The Advocata Institute strongly urges authorities to reconsider this ill-advised proposal, noting that this policy undermines competition and oversteps seriously the role of the Government in a competitive market economy, the stated policy framework of the Government.

“Pricing acts as a reflection of the quality of services offered by hotels and serves as a differentiating factor.”

“If prices fail to accurately represent the services provided, customer dissatisfaction can ensue, especially when compared to more competitively priced options in neighbouring countries such as Thailand and Vietnam,” it added.

This is supported by a comment made by the Sri Lanka Association of Inbound Tour Operators (SLAITO) which states that “before implementing such prescribed rates, it is crucial to generate demand and interest in Sri Lanka.

Adopting these rates will render Sri Lanka uncompetitive and result in a loss of clients, even when compared to hotels in New Delhi, with which they are currently competitive”.

Advocata opines the imposition of minimum room rates restricts hotel owners’ flexibility in setting prices by market demand and effectively stifles healthy competition among various establishments.

The tourism industry experiences fluctuations in demand that correspond to seasonal and weekly trends. Such demand patterns necessitate the ability of hotels to tailor their pricing strategies to capitalise on peaks and optimise profitability.

“Every hotel has its unique room pricing considerations depending on factors such as location, size of the hotel, market demographics, level of competition, and type of service offered to name a few.

The uniform imposition of minimum rates disregards the diverse range of hotels and accommodations available in Sri Lanka, catering to various budgets and preferences. This one-size-fits-all approach disregards the crucial factor of consumer choice.

Imposing minimum room rates on a certain type of accommodation whilst disregarding alternate forms of accommodation available within the city of Colombo such as guest houses and Airbnbs, undermines the effectiveness of this policy,” it explained.

Colombo (LNW): In the backdrop of Sri Lanka Central Bank’s delay in implementing the domestic debt restructuring process, the United States government has asked a federal court in New York to delay judgment as it may intervene in the case between the Government of Sri Lanka and Hamilton Reserve Bank.

Hamilton Reserve Bank has sued the SL government for the recovery of US$250 million in bonds that it has defaulted last year, the global economic media giant Financial Times has reported from New York.

Governor of the Central Bank of Sri Lanka (CBSL), Nandalal Weerasinghe who was named amongst the 21 Bank Governors listed in the Global Finance has accepted the fact that they have not been able to complete commitments under the US$3 billion IMF extended fund facility programme.

The reason for the delay in the fulfilment of IMF EFF commitments was the ongoing court cases against debt optimization programmes, Weerasinghe who was amongst the 10 governors who earned an ‘A-’ grade claimed.

Sri Lanka has filed a motion to stay the judgment of U.S. District Court for a period of six months until it carries out negotiations on sovereign debt restructuring with sovereign and commercial creditors (foreign governments and foreign funds including banks).

The United States Attorney for the Southern District of New York, Damian Williams, has sent a letter dated August 30 2023 to U.S. District Judge Denise Cote, the judge hearing the case, to inform the court of the “potential participation of the United States Government” in the case.

“The United States is actively considering whether to file a Statement of Interest with respect to the pending motion to stay”.

“The United States expects that it will be in a position to inform the Court of its potential participation in this matter, and to file its Statement of Interest should it be authorized to do so (by the Department of Justice), no later than October 2, 2023,” the letter states.

“The Government respectfully requests that the Court reserve decision on the pending motion to stay until the United States has had an opportunity to submit any such statement of interest,” the letter adds.

The case was filed in June 2022 after Sri Lanka declared bankruptcy and defaulted on $1 billion of this particular bond issue, of which Hamilton Reserve Bank holds $ 250 million.

A judgment in favor of Hamilton Bank would potentially prevent the GOSL from including the bonds held by Hamilton Bank in any debt restructuring process.

Sri Lanka’s Finance Ministry has not yet issued a statement on the latest developments in the case. Sri Lanka Central Bank Governor expressed confidence in fulfilling the commitments and implementing all reform targets before the next Executive Board Meeting of the International Monetary Fund (IMF) in November 2023.

Colombo (LNW): Newly appointed United Nations Resident Representative Marc-Andre’ Franche expressed appreciation over Sri Lanka’s economic recovery from an unprecedented crisis last two years and assured continuous support for the development process, Prime Minister’s Media Division divulged.

He said this when he called on Prime Minister Dinesh Gunawardena at the Temple Trees yesterday.

He noted that Sri Lanka is heading back in the right direction, but cautioned that the next couple of years will be very difficult for not only Sri Lanka but most of the countries due to the global economic downturn.

The Prime Minister said several steps have been taken to increase food production and ensure food security. “We also plan to diversify exports as in the long run we have to, not only be self-sufficient in food, but also increase foreign exchange earnings through exports,” he said.

The Prime Minister also briefed the UN representative about the steps taken for solving the grievances of the people who suffered due to 3 decades of conflict.

He pointed out that over 95% of the lands in North and East taken over during the conflict has been returned to the owners, land mines were removed so that the farmers could cultivate their lands, LTTE detainees have been released and fisheries livelihoods have returned to normalcy.

UN Representative Franche thanked Sri Lanka for the valuable services rendered by Sri Lankans who served in the UN system over the decades.

He acknowledged that the Office of Missing Persons and other institutions have made remarkable progress in their work and requested steps to speed up the remaining work.

Prime Minister Gunawardena thanked the United Nations for the support given to Sri Lanka and expressed confidence that the Resident Representative would take it to a higher level.

UN Representative commended the progress made by Sri Lanka in achieving the country’s Sustainable Development Goals (SDGs), recognising the efforts undertaken to address pressing social and environmental challenges, the PMD statement said.

Sri Lanka PM had updated the UN chief on the progress made in Sri Lanka’s economic recovery and debt restructuring efforts. He had also presented the Sri Lankan government’s “ambitious climate prosperity plan”.

He outlined significant strides achieved in the process of economic recovery and the ongoing initiatives to restructure the country’s debt”, the PM’s MD statement said.

It added that the Premier had also highlighted Sri Lanka’s commitment to implementing sustainable economic policies and fostering a resilient financial framework to ensure long-term stability.

In terms of climate prosperity, the government has implemented comprehensive strategies aimed at mitigating the adverse impacts of climate change while promoting sustainable development.

The plan emphasises the importance of renewable energy, conservation efforts, and climate-resilient infrastructure, it said.

Minister of Energy Kanchana Wijesekara says the QR Code based fuel rationing system has been suspended: fuel shed owners say this rationing system was only of academic interest after the fuel pump prices were more that doubled, as most customers purchased much lower quantities of fuel as against the quota.

Analysts express shock upon learning from Dr Wasantha Bandara of the National Patriotic Collective that China’s plan to rescue SL from economic crisis in 2022 had been shattered following the unilateral declaration of bankruptcy by CB Governor Nandalal Weerasinghe: also refer to the previous CB Governor Ajith Nivard Cabraal’s affidavit to the Supreme Court wherein he has asserted that a USD 10.7 bn “pipe-line of inflows” was in place when the hasty debt default announcement was made on 12April’22.

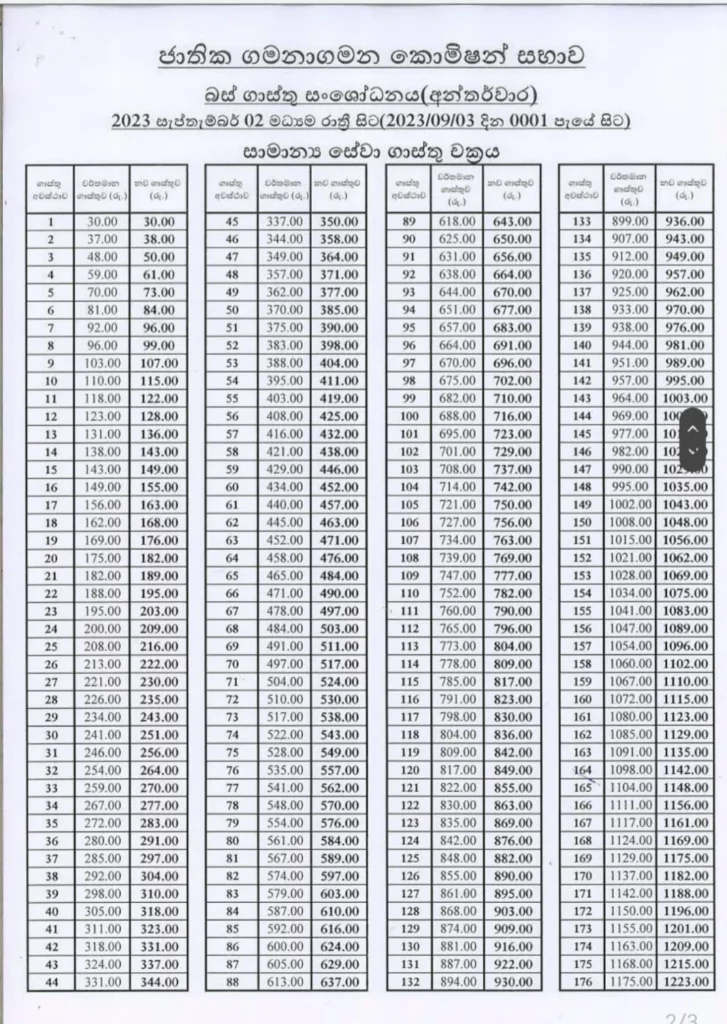

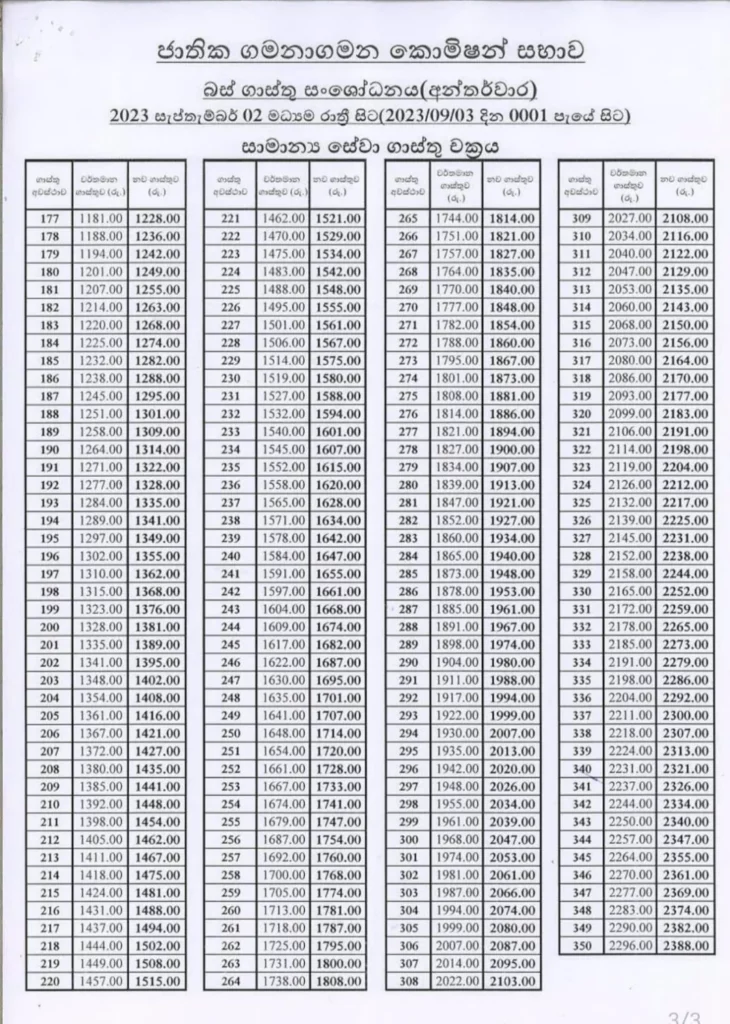

Representatives of the Transport sector propose to the National Transport Commission to increase bus fares by 4% and to keep the minimum bus fare unchanged: Assn of Container Transporters say Container haulage charges will be increased by 5%.

Central Bank tweets that its Governor Dr Nandalal Weerasinghe has been rated “A-” by the “Global Finance Magazine” based “on inflation control, economic growth goals, currency stability, & interest rate management”: analysts question the credibility of this claim since Sri Lanka announced bankruptcy, experienced its highest inflation & interest rates, suffered quarterly economic contractions of over 10% per quarter, and the LKR displayed wide fluctuations, during Weerasinghe’s tenure: analysts also express amusement that the CB has tweeted this news as this “Global Finance Magazine” has only 9,693 followers on Twitter, 8,300 followers on Facebook & a worldwide “circulation” of just 50,000.

Disaster Management Center says 20 districts affected by the dry spell: Agriculture and Agrarian Insurance Board says more than 60,000 acres of paddy fields destroyed by the dry weather: overall, 279,892 people affected.

The US Govt asks a US Federal Court in New York to delay judgment in the case between the SL Govt and Hamilton Reserve Bank (which has sued for the recovery of USD 250mn in bonds that the SL Govt defaulted last year), as it may intervene in the case: previously, the SL Govt had filed a motion to stay the judgment for a period of 6 months until it carries out negotiations on debt restructuring with sovereign & commercial creditors.

Monetary Board cancels the Finance Business Licence of Bimputh Finance PLC with effect from 1September’23: says the financial condition of BFP has deteriorated due to deficient capital level, poor asset quality & continuous losses and no satisfactory progress has been made to revive the critical condition.

Diplomatic sources say Japanese PM Fumio Kishida is scheduled to visit SL next week, on his way to the G-20 Summit in New Delhi: PM Kishida is likely to meet President Ranil Wickremasinghe to discuss the SL’s debt restructuring and future investment opportunities.

UNDP Report reveals that “a lack of education, and the ability to adapt to disasters are factors that make most people feel vulnerable” in SL: also says several districts, including Puttalam, Batticaloa, Mullaitivu, Kilinochchi, Ampara, Vavuniya, & Nuwara Eliya, exhibit multi-dimensional vulnerability, “highlighting the need for focused interventions to address factors like disaster preparedness, debt relief, water source accessibility, & female education”.

England Womens Cricket team slumps to its 1st defeat by SL in T20 internationals: SL levels series with this historic win at Chelmsford: ENG-W 104 (18): SL-W 110/2 (13.2): Chamari Athapaththu 55 in 31 balls.

")