In a move aimed at alleviating the financial burden on senior citizens, the government has made the decision to refund the five percent withholding tax that has been imposed on the interest and taxable income of senior citizens. This refund will come into effect after September 10, provided that the interest income remains below Rs. 100,000 per month. Finance State Minister, Ranjith Siyambalapitiya, announced this significant decision, which was made in collaboration with Finance Minister President Ranil Wickremesinghe, taking into account the circumstances faced by senior citizens.

During his role as the chief guest at the tenth Annual General Meeting of the Inland Revenue Assessors’ Union (IRAU) in Colombo on August 29th, the State Minister shared these details. The withholding tax, amounting to five percent, had been instituted starting from January 1, 2023, impacting not only senior citizens but also individuals with an annual interest income exceeding Rs. 1.2 million.

Recognizing the concerns and appeals from senior citizens whose monthly interest income falls below Rs. 100,000, the government has approached the matter empathetically. Negotiations were held with the Inland Revenue Department to address this issue. Consequently, a decision was reached to refund the five percent that had been deducted as withholding tax from the interest income of senior citizens who earn less than Rs. 100,000 per month. This corrective measure is set to take effect from September 10 onward, providing some relief to the affected seniors.

Tragedy struck on the Colombo-Kandy main road last night, August 29th, as a head-on collision between two buses in the Kajugama area claimed one life and left nine others injured.

According to initial reports, the incident involved a privately-operated bus carrying a group of employees and a bus operated by the Sri Lanka Transport Board (SLTB). The collision occurred when the private bus attempted to overtake another vehicle and crashed head-on into the SLTB bus, which was en route from Kattankudy to Colombo.

Regrettably, the 44-year-old driver of the private bus lost his life in the collision. Among the casualties, four women and five others sustained injuries from the impact. The deceased driver’s body has been transported to Wathupitiwala and Warakapola hospitals.

As the investigation unfolds, the driver of the SLTB bus has been apprehended and is currently in police custody. The Nittambuwa Police are diligently conducting further inquiries into the incident to ascertain the full scope of the tragedy. This unfortunate event serves as a poignant reminder of the importance of road safety and vigilance while traveling.

In a remarkable celestial event, the sun’s apparent southward journey will position it directly over the latitudes of Sri Lanka, gracing the island nation with its overhead brilliance from August 28th to September 7th this year.

As of today, August 30th, several towns in Sri Lanka will experience the sun directly overhead around 12.11 noon.

These towns include Talaimannar in the Mannar district, Iramiyankulam in the Vavuniya district, Karappukutti in the Trincomalee district, and Palampasi in the Mulathivu District.

Prevailing showery condition is expected to continue in south-western part of the Island during next few days.

Showers will occur at times in Western, Sabaragamuwa, Central and Northwestern provinces and in Galle and Matara districts. Fairly heavy showers about 75mm can be expected at some places in Western and Sabaragamuwa provinces and in Galle and Matara districts.

Showers or thundershowers will occur at several places in Eastern and Uva province and in Mullaitivu districts during the evening or night.

Fairly strong winds about (40-45) kmph can be expected at times in western slopes of the central hills, western and Sabaragamuwa provinces.

General public is kindly requested to take adequate precautions to minimize damages caused by temporary localized strong winds and lightning during thundershowers.

On the apparent southward relative motion of the sun, it is going to be directly over the latitudes of Sri Lanka during 28th of August to 07th of September in this year. The nearest towns of Sri Lanka over which the sun is overhead today (30) are Talaimannar (Mannar district), Iramiyankulam(Vavuniya district), Karappukutti (Trincomalee district), Palampasi (Mulathivu District) about 12.11 noon.

This story is about Junious. Please do not think that I made a mistake in naming the hero and misspelling Junious for genius. I quite understand some people’s misunderstanding of that sort because an impression has been created and kept for a long time that Junious was in fact the genius. That is far from the truth. A Junious is rightly called Junious, as you will see when you read this story.

The Junious was a practical “trickster”. And, being a successful trickster far beyond what the people of that trade has achieved, he even created the impression of being a great statesman, a great politician and you can add whatever other titles to his acclaimed greatness.

A “Junious” belongs to a generation of people who came by big fortune, which they could have never expected or even in the latter time, grasp. They were overwhelmed by the enormous fortunes that fell on them. That such people will lose their minds in such a process, is quite normal. They should not be blamed for imagining themselves to be what they never were and never could be.

A good parable about how fortunate they were could be explained from an example from a different place. That place is known as Cambodia. From about 1975 – 1978, a big fortune fell on a man who was mostly unknown and could never have achieved anything worthwhile due to some political leaders in the United States taking to their heads to bomb Cambodia, and to bomb most mercilessly. To put it shortly, hundreds and thousands of people who were killed due to these bombings also produced another vast population, which fled their villages and rushed to the only place which could be called a City in their country, called Phnom Penh. All of a sudden, the whole City became filled with a far far bigger population than it could ever accommodate, and the result of such a situation is unrest of all sorts.

This brought a great fortune to a group of people who were in the jungles, living miserable lives and even afraid of some big massacre, which may all destroy them, like millions of people were destroyed just few years earlier in Indonesia when due to a great misconception that Indonesia may become Communist and add to the strength of Communism in the region. The American establishment, with the help of the some military leaders who were looking for some big fortune to come their way, massacred millions of people who had any sort of connection to the Indonesian Communist Party. The people who went underground in Cambodia were expecting a similar catastrophe to fall on them, and that was one of the reasons why they have left their cities where they were earlier working as social democrats and are now working as militant guerrillas in the forest.

But, when an old upsurge of people was taking place in the Capital of their City, they saw that the fortune was beckoning them. They walked to their Capital from their hiding places and as they expected, they were received with overwhelming enthusiasm by the people who were wholly desperate and were looking for some form of hope. They thought that this significant group of guerrillas emerging from the jungles to be much more mightier than they ever were and embraced them with great enthusiasm.

Suddenly, a ruling “elite” was formed just overnight. They had the control or their hope for the entire country. And, they did what many who go crazy would do and try to realise the wildest dreams they had about achieving what they thought was a new world of new Cambodian people, without the intelligentsia who would tell them what to do and without any King to give them orders. So, there began to be unleashed the fortune of this small group of people which brought about the greatest misfortune that is ever known, in the history, not only of their country, but also one of the greatest misfortunes, that a humanity has experienced in the world.

Three years went by this way, and during that time, over one seventh of the population of Cambodia vanished, which meant that they were killed due to starvation and other physical misfortunes, as well as political misfortunes of being suspected and killed as possible spies or traitors.

In order to make the story short, we may tell the next stage when the whole country collapsed under the weight of such a huge misfortune. And when with the invasion led by foreign powers with the people from Cambodia itself who had fled for security to the neighbouring country, the Pol Pot Regime fell and whoever that remained of that regime fled into the jungle. And people, for their part, not realising that the worst nightmare of their lives is over, and still fearing for their lives, fled as refuges to neighbouring countries such as Thailand. Whatever and whoever, that remained out of the more educated classes, also fled to other countries which welcomed them, like for example, the United States and also many countries in Europe.

As for the main cities of Cambodia, they remained completely abandoned and as one well known journalist described, “Cambodian cities look like places which had been hit by a nuclear bomb.” Everything had come to a standstill. If a car was left somewhere in 1975, it was there at the same place even by the early 1980s. That was the situation of all buildings, including all houses in these cities of Cambodia, particularly to the only really worthwhile place to be called a livable place, Phnom Penh.

People who have fled their villages and whatever place they stayed, and also had lost many of their family members, still did not have the will to return. However, as it always happens, few adventurous ones migrated slowly to the city, and found the empty houses and empty spaces everywhere. Some of them just stayed for a short rest, but then they found that there was nobody to object to their presence and gradually they realised that these houses had no occupants, and that therefore, they could occupy them. So they began a period of slow migration, from refugee centres to the country, which had no organised way of life, but had empty spaces where they could settle and remain undisturbed.

This part of the Cambodian story is merely told in order to illustrate how great misfortunes bring about sub-fortunes for some people at certain times.

That was the situation of a small group of people that began to emerge from out of the depth of the miseries,which was a part of the Sri Lankan way of life (we call it the “Sri Lankan way” only in terms of present day references). Out of the colonial takeover of Cambodia, gradually there emerges a small number of people who having leant to be providing services to the new colonial power, were able to get certain advantages which were far beyond what the rest of the population could aspire for. They became landlords of large lands and there emerges a few families which would dominate whole areas. The only significant people of a particular area will be the particular dominant family, while the rest were nobodies and knew that they were nobodies.

The colonial power that came, did not stay for a very long time. They stayed only for about 130 years or so, and by the latter part, they had begun to realise that they have to leave. That provided the fortunes for those small groups of families, which had built the links with the colonial power. However, the fortunes were far bigger than what they expected, if they had any expectations at all that could be achieved within a short time. The colonial power was not merely giving them properties and other benefits. They were in fact giving the whole country to the charge of “these people.” Political power itself was given to them. They became Jupiter, Apollo and Zeus, just overnight. And this sense of enormous wonder of a big fortune that has fallen on them, that conditioned the mind, soul and all expectations of this small group of people.

In short, they went mad. They went mad with the kind of fortunes that they had begin to enjoy and to collect fortunes for their families.

The mind and the soul of Junious was formed within the framework of those fortunes that came from their colonial patrons, who could not keep these fortunes for themselves, any more. Essentially, from the very beginning, it carried the elements of madness.

It is natural for mad people to make a mess of things. That is what the country has been experiencing all this time. The fall of the economy and everything else is merely the result of such madness, that for all purposes seems incurable.

PMD: Minister of State for Finance, Shehan Semasinghe, said that among the 2 million Aswesuma beneficiary families, phased payments have commenced for 1.5 million families. In the first phase, a total of Rs. 4.395 billion have been successfully transferred to the bank accounts of 689,803 beneficiaries. Semasinghe stated that the second category’s monetary provision will be enacted starting next week. He conveyed these updates during a press conference held today (29) at the Presidential Media Center under the theme ‘Collective Path to a Stable Country.’

Highlighting that around Rs. 15 billion is earmarked for assisting the 1.5 million shortlisted beneficiary families, the State Minister emphasized the prompt release of necessary funds for their support.

Queries concerning fund matters can be directed to the hotline number 1924 on weekdays from 10 a.m. to 9:00 p.m. Moreover, allowances for disabled individuals, the elderly and kidney patients have already been disbursed.

Minister Semasinghe underlined that if Aswesuma benefits were acquired through fraudulent means, legal action would be initiated against such persons and in such cases, efforts to reclaim the disbursed funds will not be hesitated upon.

State Minister Semasinghe further said;

“The government has initiated the disbursement of funds for the initial group entitled to benefits. Presently, 689,803 beneficiary families have received a total of approximately Rs. 4.395 billion in their bank accounts.

Among the beneficiaries, 1.5 million families qualify for relief, with an additional 1 million families having submitted applications. Approximately 100,000 families are engaged in protests. In light of these considerations, a collective total of 2 million beneficiary families are selected for relief. Parliament has granted approval to provide benefits to these 2 million low-income families through the Aswesuma relief program.

Currently, funds for the first batch have been released, with plans to distribute funds to the second group in the upcoming week. For inquiries or information related to this matter, individuals can contact the hotline at 1924.

The funds being disbursed pertain to the month of July, with future arrangements to provide funds for August. The program ensures consistent and guaranteed benefits without any gaps. Notably, these relief measures are provided alongside elderly and disability allowances.

The Samurdhi Institute plays a pivotal role in uplifting these families, especially the most vulnerable among them. This empowerment is crucial as beneficiaries will need to reapply for insurance next year. The Aswesuma program aims to assist those who genuinely require support, ensuring the allocation of benefits to families in need.

With the empowerment of individuals, the necessity for continuous benefits diminishes. Concurrently, investigations are underway to identify instances of false information submission for illegitimate gains. The Aswesuma Act includes provisions for recovering funds obtained through false means. Recovered funds are then redirected to beneficiaries on the waiting list.”

Meanwhile, the Chairman of the Aswasuma Welfare Benefit Board Mr. Jayantha Wijayaratne, said:

“The endeavour is underway to extend benefits to eligible families through the Aswasuma program. A sum of Rs. 5 billion has already been deposited into the accounts of 791,000 out of the current 1.5 million qualifying families. Presently, over 683,000 of these families have successfully received their funds. The remaining 111,000 beneficiaries are scheduled to receive their payments in the coming days.

The second group is set to receive their funds in the following week, with the aim of disbursing the entire amount before September 15th. All individuals meeting the qualifying criteria are assured of receiving benefits. Consequently, there is no reason for unnecessary apprehension. All eligible individuals are guaranteed monthly benefits, and there is no need for any doubts in this regard.”

Colombo (LNW): The Cabinet of Minister has granted approval to import 92.1 million eggs from India during the next three months, as per a proposal by the President in his capacity as the Minister of Finance, Economic Stabilisation and National Policies.

Accordingly, 92.1 millions eggs will be procured for a period of three months, through the State Trading (Misc) Corporation based on the recommendation made by the standing procurement committee appointed by the Cabinet.

Accordingly, quotations will be called in from Indian companies recommended by the Department of Animal Products and Health in this regard.

The move comes in with the objective of stabilising the prices of eggs in the local market.

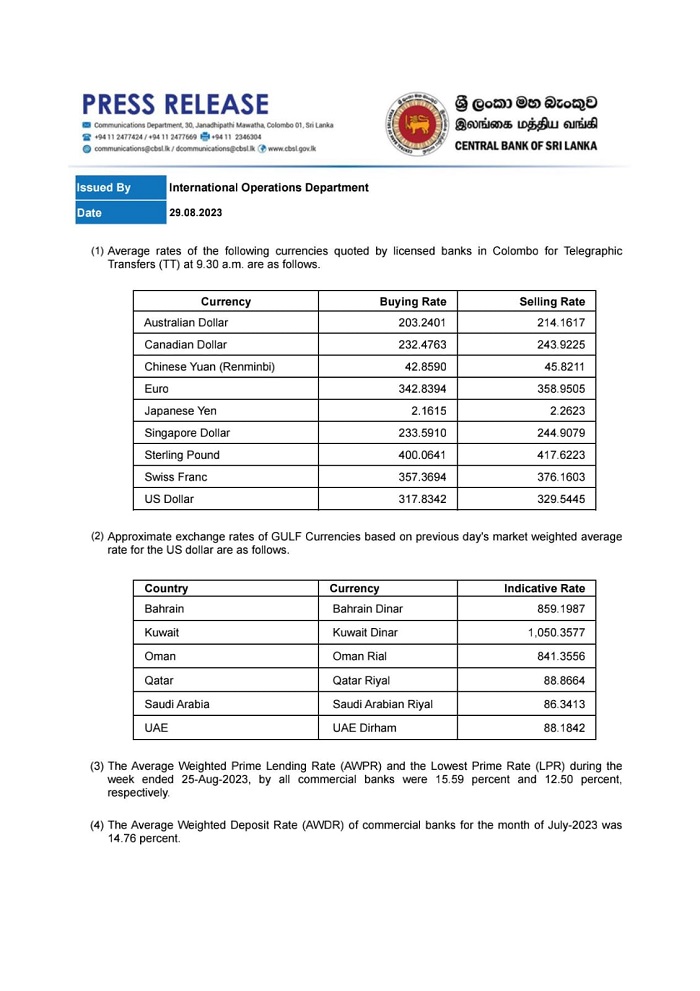

Colombo (LNW): The Sri Lanka Rupee indicates a slight fluctuation against the US Dollar today (29) in comparison to yesterday, as revealed by the official exchange rates list issued by the Central Bank of Sri Lanka (CBSL).

Accordingly, the buying price of the US Dollar has dropped to Rs. 317.83 from yesterday’s Rs. 317.96, and the selling price has increased to Rs. 329.54 from Rs. 329.52.

Meanwhile, the Sri Lanka Rupee indicates a subtle depreciation against several other foreign currencies, including Gulf currencies.

The IMF programme needs to be used to negotiate debt restructuring with commercial and multilateral creditors. It would create space to spend on priorities such as food and fuel. However, the country needs to urgently reinstate its fiscal responsibility, with a prescribed annual cap on fiscal deficits. A medium-term debt management plan updated for a certain period should be formulated and implemented with that cap limiting the expansion of non-concessional loans.

Necessity of Inclusivity

Stakeholders need to stop over-politicising economic issues, as populism has deeply clouded effective decision-making. What we need is the development of an inclusive, consensus-based and egalitarian approach towards a national development framework. The country needs to aggressively diversify its open economy, especially those that are mostly dependent on primary commodities, primitive value-added products, exports of human resources and tourism. Currently, the open economy is dependent on the export earners that are subject to significant volatility due to price fluctuations and regional instabilities.

A green and sustainable approach

Sri Lanka has a great potential for greener and sustainable economic development by utilizing its renewable energy sources and value-added industrial clusters such as for minerals processing. However, IMF debt restructuring, while not improving the country’s economic conditions, will only prolong its indebtedness. Instead, policies need to be formulated and implemented so as to ensure the population’s basic needs are met by guaranteeing the safety of food, energy and water. Significant cuts to unnecessary handouts and wastage in government and public service delivery will be necessary. This can include cutting down the size of the government including both the executive and legislature.

Performance evaluation

Performance targets need to be established in key result areas such as public finance, education, energy, health, and transport. Aggressive restructuring of state-owned enterprises can be carried out without selling them to the private sector. For example, hiring competent managers and firing inefficient ones, providing subsidies to those most in need of assistance, and trimming government expenditure by cutting down on excess political appointments. Education, health and energy need to remain as state flagship initiatives but be made efficient and result focused.

Alternatives and national dialogue

To come out of the current poly crisis, there are certain possibilities that could be adopted as alternatives; for example, progressive taxation, open governmental transactions, independent debt audits and prioritising social protection. However, all of these should be underpinned by a national public dialogue. This is about national social movements genuinely leading the national public dialogue in a transparent manner, where the behaviour and agenda of vested interest groups, both domestic and external, are curtailed. This involves sitting down together with civil society organisations, trade unions, government members, feminist collectives, human rights groups, NGOs, and community development organisations.

Vital role of government

The government’s guiding role in the economic and social development of a country is vital. As such, promoting a small government in developing countries where public services are essential and in extreme demand is misplaced. Instead of a bloated public service, there should be a service which is a productive, effective and people oriented. In the long term, we need to establish a skilled public service, where public servants bound by service charters will treat the general public fairly, with respect and courtesy, while catering towards satisfying people’s socio-economic needs. As demanded in many developing countries, Sri Lanka needs to implement a rights-based approach towards economic and social development.

Assured failure

The panaceas of neo-liberal economists do not eliminate periodic crises but generate worst ones over time. In the short term those panaceas reduce budgetary income received via tax receipts. However, businesses will demand governments reduce taxes on profits and investment, while the public will demand more services and provisions. Thus, such unplanned, competitive and antagonistic production relations will allow the state coordinated long-term regulative and growth strategies to fail.

Rights busting

Neoliberalism has succeeded in union busting and restricting workers from participating in political and institutional decision making. Throughout the world, union memberships have fallen and continue to fall. Another factor in this equation is the power within trade unions being moved away from grassroot workers to a growing bureaucracy. This bureaucracy receives increased privileges under a conservative form of leadership with its display of political timidity as their main characteristic. Trade unions do not represent politics of protest anymore.

Paralytic left

Though the Left works in the belief that capitalism has been always weak, decadent, and is in its final death throe, capitalism has survived under many guises. Yet, if able to unite under a single banner, workers may have more power than ever before. We are aware that capitalism is moving from one crisis to another, but it has not broken down yet and has not lost its political control. Moreover, the working class and the Left have not seen much of a surge. Rather neoliberalism has strengthened, pretending to be the best solution to the crisis generated by itself.

Diversity and exclusion

Instead of working together, activists in Sri Lanka try to undermine each other. Unfortunately, this is also a global experience. If everyone worked together instead of undermining each other, the situation could have been made better. Thus, people do not have any other choice to come out of this poly-crisis, but to confront this catastrophe holistically. Instead of dwelling solely on current issues, activists may need to focus on where it makes an impact, honestly acknowledging the challenges society is faced with and working towards long-term solutions for addressing the root causes of inequality and injustice.

A shared burden

Therefore, it is imperative for us to unite and bring to power a government with the political will and commitment that will share the burden of debt restructuring with those who can bear that burden without destroying the lives of people who are already at a disadvantage due to existing systemic issues. It is the affluent and the elite that are the most astute at using loopholes in the existing system to evade taxes. They then launder their ill-gotten gains in offshore tax havens. They need to be compelled to pay their fair share of tax. They also need to be held accountable for the lax in many cases of criminal and corrupt activity they have partaken in for many a decade. Everyone must keep in mind that the revenue and expenditure of a government are the commonwealth of all the people, not of a select few. Fiscal and monetary policy must be adapted accordingly.

This article is not arguing for building a socialist economy or a self-sufficient economy. However, it rejects the prevalent neoliberal model of capitalist production that is accompanied by corruption, mismanagement, waste, and lack of transparency and accountability and the sacrifice of national interests and sovereignty to satisfy international financial interests.

Sri Lanka needs to pursue an economic development strategy that is efficient, sustainable and equitable. The priority must be to produce in the country, the maximum amount of its essential commodities, i.e., goods and services necessary for the well-being of its inhabitants that can be sustainably and efficiently produced, while also utilising global markets to optimise the use of its resources to enhance overall national welfare.

Sri Lanka should avoid unsustainable imports and associated international indebtedness that result in ‘boom and bust ‘ cycles while undertaking appropriate investments and implementing appropriate policies to harness and enhance the natural and human resources needed for the country’s sustainable long-term development.

central bank policy interest rates are overnight or very short-term risk free rates on central bank’s money printing-based credit operations,

credit operations of the rest of the monetary economy are taken place at various degree of risks,

interest rates are the prices of risks such as real business and inflation and,

therefore, policy interest rates-based monetary policy cannot drive market interest rates and credit flows unless central banks implement risk sharing and mitigation tools in the monetary policy.

In that context, this part II of the article shows why the Central Bank of Sri Lanka (CB) which pursues a policy interest rates-based monetary policy model along with its subsidiary policy tools introduced to support the monetary policy model like a God-given policy strategy is bound to fail.

The rationing of standing facilities effective from 16 January 2023, the cut of statutory reserve ratio (SRR) by 2% effective from 16 August and monetary order setting maximum lending rates of banks effective from 25 August are the three subsidiary tools covered in this article.

This article helps CB and other policy economists to learn simple market economic principles before they resort to such monetary market controls.

Rationing of standing facilities effective from 16 January

Standing lending facility only up to 90% of the SRR of the bank on the day.

Standing deposit facility only up to 5 days/times a month.

This is a rude violation of the economic principle of policy interest rates corridor model. In the model, inter-bank overnight interest rates are expected to prevail in the policy rates corridor as standing facilities are provided limitless at respective policy interest rates. Accordingly, policy interest rates are the price controls that are maintained through the unrestricted printing/supply of money by the CB. Therefore, if the CB imposes rationing on standing facilities (controls of market quantity), inter-bank market prices will move beyond the controlled prices depending on the supply and demand available in the market.

This is simple economics that any sensible person understands from the state price controls in commodity markets. The outcome of price control and rationing is no exception to the monetary market. However, as policy interest rates are static numbers on the paper kept by the CB, they will remain like other controlled prices that are used in the computation of the consumer price indices.

The objective of the CB for the new rule was to activate the dormant inter-bank market struggling from the financial bankruptcy of the economy and to bring down market interest rates through the liquidity already available in the market without policy rates cuts and injection of new liquidity from money printing.

However, data show that inter-bank interest rates continued to stay at high levels as the market activity did not rise. Therefore, the CB had to cut policy interest rate twice by total of 4.5% unexpectedly, i.e., 2.5% on 31 May and 3% on 30 July. Further, the CB has commenced reverse repo auctions (overnight and term basis) at an excessive scale on a regular basis to inject new liquidity to the inter-bank market in order to cover up the curtailed/rationed standing lending facility. Further, the most of reverse repo rates were cheaper than the standing lending facility rate without any justified reasons.

Finally, the use of the risk free policy interest rates corridor to target overnight inter-bank interest rates on risky lending is unfounded in economics and finance.

Therefore, the CB has miserably failed on the policy interest rates model and rationing tool.

SRR cut by 2% effective from 16 August

The CB in its press release dated 9 August stated that the SRR cut by 2% would release about Rs. 200 bn of new liquidity on a permanent basis to the domestic money market and reduce the cost of funds and lending rates of banks which will support the expansion of credit flows to the economy.

However, the utter failure of the CB on the SRR cutting tool is testified by the CB’s monetary order issued on 25 August prescribing maximum interest rates on bank lending products.

First, this is not a new liquidity injection, but only an increase of free reserves of banks at the existing liquidity. The new liquidity comes only from the money printing by the CB which continues with reverse repo auctions and lending to the government.

Second, there is no basis to state that bank credit flows will expand. It is the old monetary theory to state that credit creation will expand due to SRR cut and vise versa on the assumption of credit as a byproduct of deposits. According to the modern monetary theory, if there is demand for good credit, banks can first lend through book entries and then find the liquidity from other sources inclusive of money market and borrowing from the CB as part of managing the liquidity of the whole bank. Therefore, bank lending is not a business carried on pre-deposit mobilization whereas deposit business in fact is a byproduct of credit business in modern banking. Therefore, it is incorrect to state that banks will expand credit just because of the SRR cut as the CB states.

Third, the SRR cannot influence in interest rates on bank credit business as the SRR cannot determine and affect credit risks of bank borrowers and the economy. Everybody knows the alarming credit risk in the current context of the economic bankruptcy and impaired credit and investment portfolios of the banking sector.

Therefore, the reduction in the cost of funds and market interest rates and resulting expansion of bank credit flows due to the SRR cut are just a part of the old monetary policy story of the CB.

Monetary order on maximum interest rates on lending products effective from 25 August

This is a normal act of bureaucratic price control to make political leaders feel happy that regulatory authorities act against unfair traders and markets. The CB also has followed this sort of price control from time to time for same purpose when the CB fails in the policy interest rates-based monetary policy model, so called market-based monetary policy.

Price controls on products such as coconut and egg testify that the authorities have no knowledge on the mechanism of respective markets. The same is true for CB’s price controls on banking service products although the CB employs international economists to study and recommend such market controls.

It is surprised why this order has been expeditiously issued under the Monetary Law Act already repealed by the new Central Banking Legislation awaiting the Speaker’s signature where the CB does not have such regulatory powers in the new legislation. Therefore, this order is to vacate very soon.

Highlights of maximum interest rates prescribed in the order are as follows.

18% on pawning facilities

23% on pre-arranged temporary overdrafts

28% on credit card balances

In respect of other credit facilities (both new and existing) whose interest rates are less than 13.5%, a reduction of interest rates as least by 2.50% by 31 October 2023 and by further reduction of 1% by 31 December 2023

Reduction of penal interest rate on all credit products immediately to a level not exceeding 2%

The meaningless of the order as a bank credit market regulation is presented by following facts.

Interest rates are fixed by pricing the risks of credit products. However, the CB does not have a mechanism to gage the maximum risk each product encounters in order to fix the maximum interest rates. Further, the CB does not operate any credit risk insurance or mitigation measures to ensure that maximum risks are consistent with maximum interest rates. Therefore, setting of numerical limits on interest rates is meaningless.

The order refers to recent cuts in policy interest rates (by 4.5%) and SRR (by 2%) as the basis for the reduction in market interest rates. However, as pointed out above, risk free policy interest rates and bank reserves are not a basis for affecting interest rates on risky credit products unless the CB provides credit risk mitigation instruments such as refinance and credit guarantees.

The order also refers to the considerable easing in monetary conditions where interest rates of banks and financial institutions remain excessive and are not in line with current monetary policy stance. This is a flawed statement due to several reasons.

First, liquidity shortages reported from the bankrupt economy (i.e., government, banks, businesses and households) does not show any easing of monetary conditions. The CB does not give supporting figures to justify this order. In contrast, the fact that M2b annual monetary growth has declined from 16% in July 2022 to 6.2% in July 2023 and the reduction of the monetary base/reserve money from Rs. 1,436 bn in July 2022 to Rs. 1,374 bn in July 2023 (annual growth reduced from 35% to negative 0.9%) proves the opposite of the monetary easing. Therefore, the base statement in the order itself is flawed.

Second, high interest rates structure at present is in fact is a result of excessive interest rates forced by the CB through Treasury bill rates pushing from around 8% at the beginning of 2022 to around 32% towards the end of 2022 and default of public debt management. The CB also issued a monetary order on 21 April 2022 to remove maximum interest rates that prevailed at that time on credit card balances, pre-arranged temporary overdrafts and pawning advances and to force banks to raise interest rates of all banking products. However, the CB has just forgotten its reckless history and now blames banks for high interest rates. The CB unnecessarily mentions excessive interest rates charged by financial institutions although the order does not apply to them.

If banks comply with these interest rates ceilings due to unofficial threats of the CB being the bank regulator, they will immediately cut credit flows and entertain only customers and economic activities of lowers risks. This in fact will slow down credit expansion and will be a severe blow to the recovery of the economy already contracted by the unnecessarily tightened monetary policy pursued by the CB since the beginning of 2022, despite the economic crisis.

CB monetary policy economists must be well aware from both market economic principles and recent experiences that such maximum interest rates imposed for reducing the interest rates structure invariably fail. The plight of the most recent interest rates caps is as follows.

As per monetary order dated 26 April 2019, deposit rates up to 3 months were linked to standing deposit facility rate less a margin of 0.50% and other term deposits were linked to 364 day Treasury bill yield rate less 0.50% to plus 2.5% across the tenure. This was supported with a SRR cut of 2.5% to enhance the efficiency of the monetary transmission mechanism and expand credit flows. However, the order was withdrawn on 24 September 2019 after 5 months.

In contrast, a monetary order was issued on 24 September 2019 prescribing caps on lending interest rates on grounds and characteristics similar to the present order, for example, 28% on credit card advances, 24% on pre-arranged temporary overdrafts and reduction of penal interest rate to a level not exceeding 4%.

The caps were further reduced by the monetary order dated 21 August 2020 in view of the ultra relaxed monetary policy for the Corona-affected economy, i.e., 18% on credit card advances, 16% on pre-arranged temporary overdrafts, 10% on pawning and reduction of penal interest rate to a level not exceeding 2%.

All these caps were removed by the monetary order dated 21 April 2022 stated above as part of the high interest rates policy of the CB.

The monetary order does not contain a mechanism to ensure the compliance including the penalties in terms of the legislation. Further, the latest order issued on 28 August 2023 has not revoked the previous order dated 21 April 2022 and, therefore, banks have the option to choose the order they prefer. Therefore, abuses are unavoidable.

Therefore, the latest monetary order is simply a reopening of the old file on interest rates capping subject without any idea on its effectiveness as well as the current credit market conditions, given the bankrupt economy and the default of government debt.

Interim Remarks

The CB just look at monthly consumer price index-based statistical/annual inflation numbers and announces these bureaucratic price controls by resorting to the old monetary theory and waits till the next shock to the economy.

The recent history of such monetary policy tools (risk free policy rates model and price controls cited above) shows that they cannot influence various classes of credit risks confronted by modern monetary economies that operate on credit markets. Further, the CB does not have data to establish the effectiveness of such tools in the past.

As the CB does not implement any monetary tools to amend credit risk structure of economic activities, the present monetary policy model and money market control tools are baseless on macroeconomic grounds.

Therefore, monetary policy decisions of the CB are nothing but reopening of the old files to mislead the national leaders that the CB is dynamically engaged in recovering the bankrupt economy through enhanced monetary transmission mechanism and credit flows across the economy where the policy statements are nothing but meaningless words meant only for relevant economists and officials of the CB.

In that context, the CB’s monetary policy is not in a position to help recover the bankrupt economy unless it invents tools that are efficient in sharing and mitigating credit risks of priority sectors and activities. However, the CB is able to make billions of profit on its risk free monopoly money printing business carried out on very short-term basis with wholesale money dealers.

The danger of the attempt to implement such baseless policy tools and false statements is the uncertainties and bottlenecks created in markets and adverse impact on the recovery and stability of the economy. The literature on abuses of such bureaucratic controls at levels of both market participants and authorities is well known.

In general, unlike in developed market economies, interest rate is not a material factor to drive credit flows in Sri Lanka. What most matter are the access to credit and risks. Therefore, such credit market control tools will only be on the paper amongst the countless number of regulations relating to economic activities.

Interest rates/yield rates of government securities are well within the direct control of the CB. Therefore, the CB’s normal practice has been to set the yield rates in order to influence in interest rates in credit markets. However, the CB does not seem to reduce weekly Treasury bill yield rates during the past two months but sets ceilings on bank interest rates. Therefore, the CB should set the example for lower interest rates by first cutting the yield rates of government securities operating at its hand.

Therefore, national leaders are advised to think twice whether this is the national monetary policy that the country needs at this juncture to recover the public from the present bankruptcy as the monetary policy is not a rocket science but a concept-based intervention in the monetary side of the economy by the government for the benefit (creation of wealth and living standards) of the general public.

Overall, the tendency of the policy authorities in general to lie bravely to the public is normal. However, the present CB management lying to this extent and frequency as revealed from policy statements without specific economic research findings should be subject to serious concerns of the public, given its stability mandate.

(This article is released in the interest of participating in the professional dialogue to find out solutions to present economic crisis confronted by the general public consequent to the global Corona pandemic, subsequent economic disruptions and shocks both local and global and policy failures.)

P Samarasiri

Former Deputy Governor, Central Bank of Sri Lanka

(Former Director of Bank Supervision, Assistant Governor, Secretary to the Monetary Board and Compliance Officer of the Central Bank, Former Chairman of the Sri Lanka Accounting and Auditing Standards Board and Credit Information Bureau, Former Chairman and Vice Chairman of the Institute of Bankers of Sri Lanka, Former Member of the Securities and Exchange Commission and Insurance Regulatory Commission and the Author of 12 Economics and Banking Books and a large number of articles published.

The author holds BA Hons in Economics from University of Colombo, MA in Economics from University of Kansas, USA, and international training exposures in economic management and financial system regulation)

")

")