February 06, Colombo (LNW): In a landmark move aimed at resolving land ownership issues for over two million Sri Lankans, the eagerly anticipated “Urumaya” program is set to be officially launched on February 5 in Dambulla. Tourism, Lands, and Sports and Youth Affairs Minister Harin Fernando unveiled the details of the program during a press briefing at the Presidential Media Centre, emphasizing its goal of providing permanent land ownership solutions.

The initiative is poised to benefit over 10,000 land licensees currently holding Ran Bhoomi, Jaya Bhoomi, and Swarna Bhoomi licenses, as their licenses will be converted into freehold deeds, granting them full ownership of their land. This transformative step is expected to bring about a significant improvement in the lives and livelihoods of millions grappling with land ownership uncertainties.

Minister Harin Fernando stressed the program’s significance as a pivotal step towards building a stable and prosperous Sri Lanka. The “Urumaya” initiative underscores a commitment to addressing long-standing land issues, providing citizens with the security and freedom that accompanies land ownership.

The official launch on February 5 is anticipated to usher in a new chapter for many Sri Lankans, offering them a brighter future rooted in secure land ownership. Minister Harin Fernando reflected on the challenges faced by the nation, likening it to a critically ill patient two years ago. He drew parallels between essential yet uncomfortable treatments administered by a doctor and the adjustments made under President Ranil Wickremesinghe’s leadership, which were deemed crucial for the nation’s recovery.

The Minister emphasized that challenges are embraced not for personal glory but for the sake of the country’s success, citing his role in revitalizing the tourism industry as an example. He pointed to the lifting of the ban on cricket as a significant victory and a beacon of hope, symbolizing the potential for future achievements.

Acknowledging that the journey is far from over, Minister Harin Fernando highlighted the “Urumaya” program as a special initiative to bring about positive change for over two million people in Sri Lanka. The program aims to empower citizens by granting freehold land deeds, fostering a new era of stability and prosperity.

In addition to the “Urumaya” program, the Ministry takes pride in an ambitious initiative aimed at igniting the entrepreneurial spirit of the youth. This program seeks to empower a million young minds, positioning Sri Lanka for a golden age of rural revival and innovation.

February 06, Colombo (LNW): Five to six years ago, Sri Lanka Rugby, which had been going on for many years, changed its recent history and took a unique path as a sport. Not for the politics, we also stood up for that regime, which kept its back straight so that if even Asia tried to reach its own country and lay hands on it beyond their limits. Due to the harsh memories, we have in recent history, a different story happened. Foreigners were deployed to play in matches and had to strip in front of the world. We are still paying the fine.

The Rugby account gradually became empty while holding various carnival tournaments, inviting the country’s leader, and keeping the authorities get credit marks, and working on their existence outside of Rugby. It was the debt that went up.

As a result, the team led by Rizly Illyas demonstrated a genuine rugby personality, capable of standing independently with a distinctive identity. Even if he resigns as he should strategically go forward with that foam, we expected Sri Lanka Rugby to go ahead with that backbone. Following the acceptance, we hoped that there would be a proper investigation within the official system regarding the matters that caused the ban on behalf of Sri Lanka Rugby and that there would be a request to ask the facts from both sides as the defense and the complaint. But the Acting President, who is in a daze with the power he has suddenly received, is intoxicated by the random surprise, instead of working to confirm the previous opinion, he is pushing himself to the point of praising and flipping by himself the opposite opinions. However, it is evident now that the rugger personality we witnessed during that period has dissipated following Illyas’s departure. The current Acting President, who was the head of a sub-committee, has begun to backtrack even the decisions taken by the sub-committee under his leadership. The remaining members of the executive committee must decide whether to get on his swing or not.

When a sub-committee led by him declared that the league champions Kandy Team would withdraw from the Clifford Cup, Kandy Club was banned from the Clifford Cup, affecting this year as well. They decided to leave because the Rugby administration did not act to provide their stadium, the Nittawela Rugby Stadium. Instead, they were provided with a stadium in Kandy as an alternative. The reason for this was the decision of the Rugby administration not to allow any sports club to play at the designated stadium where they act as hosts. No matter how well and vigorously the tail wags, the dog has the right to wag it. The Rugby administration’s decision at that moment prevented the tail from becoming the dog and keep the tail in right place.

But now, the Acting President is now exerting his influence on the Executive Council, asserting that it is imperative to include Kandy in this year’s Clifford Cup, citing the birth story of the Kandy Sports Club. Now it can be seen that Sri Lanka Rugby has reached the state of showing the form of a dog that wags its tail as needed, because several tails that have worked to hinder the administration of rugby in the past are showing this hilarious type of dog wag tails.

From now on, based on the importance of the birth of a sports club, the rugby administration, which is the paternity of the national responsibility of the sport, not tailgating, but the signal that comes from this is dangerous. The foundation of an administrative operation that took the lead in changing many rights, the scandal, the debt load, etc., caused by rugby dancing to their tune by having a group of people sit on a few chairs to administer rugby, was lost in this way. It is sad that with that escape, the useless pieces of stone that were trying to be stuck somewhere that could have been seen before have appeared and started acting like mountains.

At another moment, In another instance, if the Asia president appoints his amicable ex-president, who has been associated with the most disgraceful stain on Sri Lanka Rugby, to lead , the personality that the current leadership has developed as Sri Lanka Rugby, which indicates that he is ready to show his work to the level of saying “Yes Sir” It feels like it is slowly melting away.

It is well known to the Acting President that through the crises caused by directness last season, the Asia President managed to use to down the Sri Lanka Rugby , which has more history than him, with the help of Sri Lankan own personnel, and succeeded in the rugby game of his country, which in the Asia Rugby region.

Despite that, the people who opposed the Sri Lanka Rugby should prove the size of their backs by whether they become puppets in hands or not. Or the extent of their love for rugby. Also, if an investigation has been conducted through the ministry and told to leave, Hassan Sinhawansa’s course of action should be to exit his profession. Also, the Acting President should take appropriate measures for that. This non-departure also shows that it is necessary to think about whether only the outgone president had the desire to create a background where he could work independently for Sri Lanka Rugby last season and to maintain it. If this is not the case, the Acting President should keep the decisions of the sub-committees that he led as before and not act to spoil the personality of Sri Lanka Rugby by fulfilling the needs of the people who are hindering it at this moment.

Also, Sinhawansa should refrain from allowing individuals, including himself, who hindered the organization, to assume leadership roles. At times, it is determined that stepping down is more important than remaining. Rather than persisting in a position by any means and wielding power arbitrarily, people who come stepping down for the truth will stay in society. Is there any possibility to think Sri Lanka Rugby like that? We are awake and waiting to see if the pride that has been built up in recent times will be folded in two and will be twisted by ‘Sir theory’ and will be crushed or will fight. What is happening now is the tail wagging the dog according to the visible movements.

Whether this tail represents Sri Lanka Rugby as a whole or the actions of an individual or a group is discerned through the conduct of the entire Executive Council.

February 06, Colombo (LNW): Sri Lanka–UK collaboration has opened a crucial investment corridor to effectively represent Sri Lanka to attract foreign investments. It has focused on various sectors pertinent to investment and trade relations

This was disclosed by High Commissioner of Sri Lanka to the UK Rohitha Bogollagama who underscored key objectives in facilitating the SL-UK Chamber of Commerce business roundtable meeting.

The Sri Lanka High Commission in the United Kingdom successfully organised this business roundtable on 26 January between the Sri Lanka–UK Chamber of Commerce and Foreign Minister Ali Sabry. The event marked a significant milestone in fostering trade and investment relations between Sri Lanka and UK.

Sri Lanka-UK Chamber of Commerce President Shehan Silva emphasised the significant growth the chamber has experienced since its establishment two years ago.

The roundtable successfully convened experts from various industries, such as tea, tourism, banking, and finance, contributing to the development of the strong institution it has become today.

At the meeting several crucial factors were addressed concerning Sri Lanka’s economic environment and its suitability for foreign investment.

Key points included leveraging talent within the technology industry, the stability of the Sri Lankan rupee, and the streamlined process for foreign investment especially in the Colombo Port City Project and repatriation of funds.

The highlights also encompassed Sri Lanka’s potential as a hub for finance and technology, with specific references to projects such as the solar power initiative and advancements in renewable energy.

In wrapping up the session, Foreign Minister Ali Sabry outlined the current economic challenges faced by Sri Lanka in 2022 and the subsequent need for policy adjustments.

He said that despite setbacks, Sri Lanka has emerged strong in a short span of time, a feat he attributed to the country’s strong institutions, democracy, and independent judiciary.

The Minister expressed confidence in overcoming difficulties and highlighted the Government’s commitment to creating an investor-friendly environment.

In relation to Sri Lanka’s foreign policy, he emphasised the nation’s dedication to upholding an independent foreign policy and engaging with countries exclusively on commercial terms.

Articulating that ‘in a multipolar world, Sri Lanka understands that Sri Lanka needs everyone to work with’, he expressed optimism about the growing influence of the Global South.

This alignment positions Sri Lanka to effectively address challenges and seize opportunities in the evolving multipolar landscape. Foreign Minister Sabry extended an invitation to foreign investors, encouraging them to explore the myriad of opportunities in Sri Lanka.

He highlighted the nation’s robust institutions, democratic stability, and strategic location as compelling factors for investment consideration.

February 06, Colombo (LNW): Sri Lanka is set to explore granite exports with the aim of earning much needed foreign exchange as the local demand for granite has come down in recent times, industry ministry sources said.

As per Volza’s Sri Lanka Export data, Granite export shipments from Sri Lanka stood at 43.4K, exported by 1,379 Sri Lanka Exporters to 1,747 Buyers. Sri Lanka exports most of it’s Granite to United States, India and Maldives

Sri Lankan granite imports are set to reach 4.4 million kilograms by 2026, showing an average growth rate of 3.3% year on year.

Since 1999, domestic demand for Sri Lankan granite has increased by an average of 7.9% every year. In 2021,

Sri Lanka was ranked 30th in the world, with Thailand overtaking it at 3.6 million kilograms. The UK, Russia and Denmark were placed 2nd, 3rd and 4th respectively in this ranking

The Cabinet of Ministers recently approved the immediate export of granite stocks, paving the way for a potential economic boost. Cabinet Co-Spokesman and Minister Bandula Gunawardena

Cabinet approval has been granted for the appointment of a committee to study the facts and submit a report with recommendations on the possibility and appropriateness of exporting up to one million metric tons of granite.

Cabinet Co-Spokesman and Minister Bandula Gunawardena said at present, the requirement of Granite for construction and development activities in the country is relatively low and the livelihoods of the miners engaged in the granite mining industry and the communities associated with it have been severely affected due to this.

The livelihoods of the miners engaged in the granite mining industry and the communities associated with it have been severely affected due to this, he pointed out. .

Minister Gunawardena further said that a stock of granite removed during the construction of Hambantota Magampura port is currently piled near the administrative building of the port area and in the Hambantota new hospital premises and the said granite stock needs to be removed immediately.

Taking into account a proposal presented by the Minister of Environment, the Cabinet of Ministers approved to take necessary steps for the immediate export of the said granite stocks under the supervision of the Geological Survey and Mines Bureau.

Cabinet Co-Spokesman and Minister Bandula Gunawardena outlined the dire circumstances faced by the quarry sector, with 50,000 workers witnessing a significant impact on their livelihoods due to the economic downturn.

He said the construction industry is grappling with challenges amid the economic crisis, experiencing reduced domestic demand, prompting the Government to explore opportunities for the export of granite resources.

February 06, Colombo (LNW): Consequent to the government’s decision to cultivate one million indigenous herbs across Grama Niladari divisions (GN Divisions), a memorandum was presented to the cabinet to obtain legal status for calling for expressions of interest for the commercial cultivation of cannabis.

The aim is to cultivate cannabis as a medicinal herb to produce indigenous medicines for the export market .

State minister Sisira Jayakody said the 1971 Ayurvedic Act has been amended to allow for herbal cultivation. The attorney general’s draft will be submitted to the cabinet for approval, he said.

The expected legalization of cannabis exports will earn huge foreign exchange for the country. Investors will be chosen through the Ayurvedic Council, he said.

Meanwhile the Sri Lanka Ayurvedic Drugs Corporation (SLADC) has achieved its highest profit in years in 2023, recording a notable Rs. 195 million, State Minister of Indigenous Medicine Sisira Jayakody revealed yesterday.

He said this achievement marks a significant turnaround for the SLADC, highlighting the positive impact of the new management’s strategies.

“This profit is the highest since 2017,” Jayakody stated, emphasizing the remarkable progress made by the SLADC under its new leadership. He attributed this success to the implementation of effective measures by the new management, which have revitalized the corporation’s operations and financial standing.

State Minister Jayakody said in celebration of the 76th National Independence Day, the Government has launched a program to cultivate 1 million indigenous herbs across the country thereby boost domestic production of medicinal herbs and to reduce reliance on imports.

The program’s first phase began yesterday and will continue until 7 April. It focuses on all Grama Niladhari (GN) Divisions across the country, ensuring widespread participation and impact.

This initiative recognises the abundance of medicinal plants in Sri Lanka and aims to address the long-standing issue of importing indigenous medicines.

By promoting domestic cultivation, the program seeks to establish indigenous medicine as a viable commercial industry.

It also aims to reduce the cost of imported raw materials used in medicine production, ultimately saving valuable resources and strengthening Sri Lanka’s self-reliance in the healthcare sector.

Government-owned vacant lands are being repurposed for a novel initiative: cultivating medicinal plants.

February 06, Colombo (LNW): In an endorsement of President Ranil Wickremesinghe’s leadership, Sri Lanka Freedom Party National Organizer, MP Duminda Dissanayake, declared the President as both the country’s luck and a catalyst for significant changes that no other politician would dare to undertake.

Speaking at the inauguration ceremony of the ‘Jayagamu Sri Lanka’ People’s Mobile Service at Salgado Grounds in Anuradhapura on the 31st, Dissanayake emphasized the transformative impact of President Wickremesinghe’s initiatives. He noted that if these changes had been implemented two decades earlier, the nation might have been in a more favorable situation today.

Dissanayake acknowledged the party’s previous opposition to Wickremesinghe until 2015, but revealed a shift in stance after that period. He highlighted the skepticism surrounding Wickremesinghe’s capabilities and the perception that he became President by default. However, Dissanayake suggested that luck, both for Wickremesinghe and the country, played a role in the positive developments.

The SLFP National Organizer praised Wickremesinghe for instituting extensive changes that, according to Dissanayake, go beyond the typical actions of a politician. He emphasized the importance of understanding and appreciating these changes, asserting that if similar reforms had been implemented two decades earlier, the country might have avoided its current challenges.

Dissanayake cautioned about the potential consequences if the public fails to grasp the significance of these changes for the future generations. Despite acknowledging that not everyone may be pleased with certain decisions made by the government, he urged the necessity of proceeding with essential changes for the betterment of the nation.

In conclusion, Dissanayake emphasized the inevitability of change, stressing that the government must press forward with necessary reforms, even if met with objections.

February 06, Colombo (LNW): Keheliya Rambukwella, who is currently under remand custody, has communicated to President Ranil Wickremesinghe in writing his decision to resign from the position of Minister of Environment.

President Wickremesinghe has accepted Rambukwella’s resignation request, according to reports.

Consequently, the appointment of a new Minister of Environment is anticipated in the coming days.

Rambukwella, facing allegations related to the procurement of substandard human immunoglobulin during his tenure as the Minister of Health, has been remanded until the 15th of this month following orders from the Maligakanda Magistrate Court.

February 06, Colombo (LNW): Foreign Affairs State Minister Tharaka Balasuriya has staunchly defended President Wickremesinghe’s recent foreign travels, countering criticisms by underscoring their significance in fortifying Sri Lanka’s international ties and forging new partnerships.

Rejecting assertions that the trips were unnecessary, Balasuriya emphasized the vital role they play in preventing Sri Lanka from becoming isolated on the global stage. He argued that fostering robust foreign relations is integral to the country’s development, asserting that the President’s visits are instrumental in establishing connections and promoting cooperation with other nations. Dismissing criticisms as unfounded, the State Minister emphasized the pivotal contribution of these trips to Sri Lanka’s progress.

During a media briefing titled ‘Collective Path to a Stable Country’ at the PMC on Thursday (1), the State Minister outlined recent endeavors to attract investment and rebuild the nation.

Sri Lanka’s diplomatic focus has centered on economic recovery and international collaboration, with President Wickremesinghe engaging the business community in discussions on rebuilding the nation and attracting investment at the World Economic Forum in Davos. The President’s participation in the Non-Aligned Movement Summit in Kampala addressed broader geopolitical concerns, emphasizing Sri Lanka’s proactive approach to securing its future through international partnerships and strategic economic planning.

The State Minister highlighted President Wickremesinghe’s participation in the G77 + China Summit, where discussions delved into pressing issues such as climate change and epidemic threats. The importance of managing economies in the face of these challenges and transitioning towards a green economy was emphasized.

Balasuriya defended the President’s foreign trips, acknowledging criticisms but dismissing them as baseless. He underscored the benefits of participating in international conferences, citing the opportunities they provide to build new connections and strengthen existing relationships. According to the State Minister, these engagements are crucial for a country seeking to avoid isolation and achieve progress.

In addition, Balasuriya pointed out that direct engagement with private sector leaders during these trips opens doors for political leaders to make development decisions tailored to specific needs and investments, fostering collaboration and potentially accelerating progress.

The recent foreign visits not only solidified the ‘offline policy’ with a renewed focus on domestic affairs but also addressed the imperative of preventing regional spill-over from conflicts in Ukraine and the Middle East. Collaborating with regional leaders, the State Minister expressed confidence in containing these conflicts and emphasized the contribution of these interactions to global peace.

4 February 2024: Since being granted independence in 1948, Sri Lanka has been run by three family dynasties whose unaccountable, corrupt and incompetent regimes have led the country into various crises: economic, political and social – including in the form of constitutional riots, two insurrections and a thirty-year long civil war. Currently the country is bankrupt and under the whims of international financiers. These families have successfully hidden their venality and incompetency, by demanding and being granted extra powers like the ones enjoyed under the executive presidency, and other special legalisation. Thus, they have made their decisions and extra judicial actions opaque and without being accountable.

Any hope that the economic meltdown and the popular protest movement (Aragalaya) might usher change are fading by the day. The political elite, if the Rajapaksa clan is an indication, are busy finding scapegoats, be they foreign elements or local, for their incompetence and greed. Instead of making their actions open to scrutiny and thus accountable, they are back to their same old diversionary trickery. For example, take the proposed counterterrorism law which gives even wider powers to supress dissent and hide their extra judicial actions. Also, sadly, the discriminatory policies and exclusion of minorities persist, further fanning the flames of communal disharmony. Meanwhile the structural, political, economic, and constitutional changes needed to ensure that there will be no further economic and political meltdowns are ignored. What follows is an assessment of these issues.

The current socio-economic situation

Sri Lanka’s economy collapsed in 2022, and it was the worst economic crisis in the country’s history. Economic crises have been a recurring feature of the country since the 1950s. In May 2022, Sri Lanka defaulted on its sovereign debt for the first time due to a series of adverse events: a loss in fiscal revenue in 2019 due to terror attacks that impaired tourism; and the global Covid-19 pandemic in 2020-2021. Compounding it were the bad economic policies adopted in 2021, notably a ban on imported chemical fertilizers – an attempt to halt an ongoing decline in foreign exchange (FX) reserves. This led to a rise in agricultural prices and dramatically low harvests. FX reserves had fallen to less than USD2bn in early 2022. Without access to international financial markets since sovereign credit rating downgrades in 2020, the government had no choice but to call for a debt restructuring. In March 2023, the IMF approved a 48-month USD2.9bn Extended Fund Facility to help the country get back on track.

The government’s response to economic challenges in compliance with conditions set by the International Monetary Fund (IMF) has come under intense scrutiny. The response has embarked on a policy of undermining human rights and exacerbating the plight of the people rather than alleviating their hardship. This is reflected in the shocking revelation that more than 17 percent of the population are food insecure, requiring urgent assistance. According to the United Nations, an alarming 31 percent of children under the age of 5 are malnourished, highlighting the severity of the crisis. Nothing is being done to alleviate their hardship.

With ongoing issues of corruption, wastage, and mismanagement being conveniently ignored, the economic burden that has been caused by the incompetence and greed of the ruling elite has been shifted to those who can ill afford it and played no role in the country’s economic collapse. Introduced are regressive policies such as increased Value Added Tax (VAT). From the beginning of 2024, VAT will be increased from 15 to 18 percent and will be applied to 97 essential goods, including essentials like fuel, cooking gas and fertilizer. An 18% VAT has been introduced even for basic necessities such as food and textbooks. Measures of social protection are not only inadequate but also politicized, leaving vulnerable communities in dire straits. Meanwhile the profitability of companies has been sacrosanct with more than half a million jobs being lost.

The indebtedness of ordinary people is on the rise: 31 percent of Sri Lankan households depend on loans to make ends meet; 24 percent are dependent on money lenders and 23 percent on bank loans. As of June 2023, the country’s staggering household debt reached more than 7 percent of the GDP. At the same time the top one percent of Sri Lankans own 31 percent of the total personal wealth, while the bottom 50 percent only owns less than 4 percent of the overall wealth in the country.

The Sri Lankan military continues to occupy land in the North and the East that formerly belonged to Tamil and Muslim communities. In trying to circumvent international pressure on the regime concerning human rights violations during the days of the armed conflict, a National Unity and Reconciliation Commission has been established, but its potential to enact meaningful change remains doubtful.

The government is trying hard to get the Anti-Terrorism Act (ATA), passed which is presented as a new and improved version of the Prevention of Terrorism Act (PTA). The Bill gives the president, police, and the military broad powers with no accountability, to detain people without evidence, criminalize speech without clearly defined parameters, and arbitrarily ban mass gatherings. The regime got its Online Safety Bill through the Parliament that will see the curtailing of free speech online. These developments clearly show that kicking out Sri Lanka’s political old guard has not necessarily translated into long-term reforms when it comes to governance and human rights.

No need to remind that the country’s armoury of draconian legislation and unaccountable powers of the executive president was astutely and repetitively used to suppress the nonviolent ‘Aragalaya’ movement.

The future

The IMF-dictated program for the sale (i.e., privatization) or closure of 430 public sector institutions will result in the loss of half a million jobs. Corporate taxes are being kept low while exorbitant taxes are levied on working people, the primary ones being higher income tax, value added tax (VAT) and various import duties.

The IMF staff report warned that the social unrest could re-emerge, fuelled by falling real incomes. Causes for unrest are the very policies the government is implementing such as, a regressive tax rate hike and cost-recovery pricing in the energy sector, insufficient anti-corruption efforts, and delayed local elections. The report also pointed to the impact of the worsening global situation. External risks arise in part from intensified regional conflicts, including Russia’s prolonged war in Ukraine and the conflict in the Middle East, resulting in commodity price volatility, and a sharp global slowdown, which could reduce capital flows and lead to a sharp exchange rate depreciation.

Despite this forecast, the IMF stubbornly insists that its austerity program which includes many of the above policies must be implemented to the letter. Its concern is not with the wellbeing of Sri Lankans but to ensure the repayment of Sri Lanka’s foreign debts and the boosting of the profits of investors. President Wickremesinghe is in complete agreement: “There is no alternative other than implementing IMF policies.” Meanwhile those who can pay and are the cause of the crisis get off scot-free, once again.

The domestic debt-restructuring plan passed by Parliament mostly cuts the retirement savings of private sector workers, which critics claimed to have spared the banking sector, international creditors, and individual domestic creditors from bearing their share of the economic burden. Moreover, wages have not kept up with rising costs, contributing to heightened poverty and food insecurity. Combined with the government’s efforts to raise revenue through increasing electricity bills and income taxes, Sri Lanka’s economic recovery has been felt unevenly by different segments of its population, eliciting protests and even union strikes.

Sri Lanka’s external finances are fragile, as reflected in continued annual current account deficits and a high level of external debt (estimated at around 80% of GDP). FX reserves as of mid-2023 covered less than one third of the external debt repayments due in the next 12 months (well below the adequate ratio of 100%) and less than two months of imports (well below the favourable ratio of four months).

To tackle these structural imbalances, no viable alternative economic development program has been developed. Production necessary to satisfy the basic needs of the people of Sri Lanka and an export diversification that moves away from the high dependence on the traditional sectors such as tea, rubber and coconut, textile, clothing, and tourism sectors remains essential for long term economic viability. Yet again those items are not on the agenda. The main opposition parties parrot the same mantra and talks about renegotiating the IMF deal, but the austerity agenda will not be subject to any negotiations.

Conclusion

As can be seen, the government has not taken the necessary steps for tackling the fundamental governance issues arising from rampant incompetence, wastage and corruption among the political and bureaucratic circles. Despite a change in government, there has been no structural, political and constitutional reform. It’s depressing human rights record remains just the same and is worsening. Humanitarian assistance and diplomatic efforts are essential to address the country’s pressing issues and ensure that the government adopts policies that will benefit all citizens of Sri Lanka.

Despite the previous year’s mass struggle protests having kicked out the previous government, many of that regime’s economic and political realities remain the same. After coming to power through a parliamentary coup d’etat, President Ranil Wickremesinghe is primarily concerned with retaining power at any cost, with the expectation that the socio-economic woes will be lessened. In the process proving his legitimacy ahead of the ‘would-be’ presidential elections in 2024. To ensure his success at the next Presidential election, he cynically and unscrupulously postponed local elections that were scheduled for early March 2024 indefinitely, citing a lack of funds. Yet, the expenditure of the government on many other fronts did not indicate such a lack of funds.

Ranil Wickremesinghe presidency continues to resort to familiar authoritarian and anti-democratic practices to quell dissent, not only against the minority communities, but also against all political dissent, in toto. With presidential elections set to take place in 2024, Sri Lanka is at an important crossroad regarding its economic and political future. There is a necessity to choose between implementing politically convenient band-aid solutions or resolving the structural problems that predate the crisis.

If not, Sri Lanka’s outlook will remain grim with political stagnation and periodic economic crisis being the norm as in the past; making 2024 a critical year for Sri Lanka. As the government and the opposition gear up for elections, there is a danger that government in power, like those in the past will squander acquired loan moneys for election gimmicks, leading to further bailouts from the IMF in the future, and being forced yet again, to enact unpopular structural reforms which will unfairly burden the citizenry of the country.

As the economic catastrophe of 2022, and the periodic early ones, the long civil war, two insurrections, numerous riots and an increasing authoritarian tendency have amply shown, if the system of governance is not fixed, Sri Lanka will be forced to relive its past tragedies. As compatriots, it is incumbent upon us to ensure that this does not happen again. We need to support those political parties and currents that look at changing our system of governance and constitution, to make it less opaque and more accountable, where the rule of law prevails and where the rights of all citizens are respected. In tandem, there must also be an insistence on a more viable and fairer economic system.

This article outlines why central bank policy statements nowadays are nothing but turning wrong pages of the monetary books relating to the present policy stance around the world and why the world needs new practical mandates-based policy books for central banks in the interest of the general public living in the digital civilization.

Background of present monetary policy stance – US, UK and EU

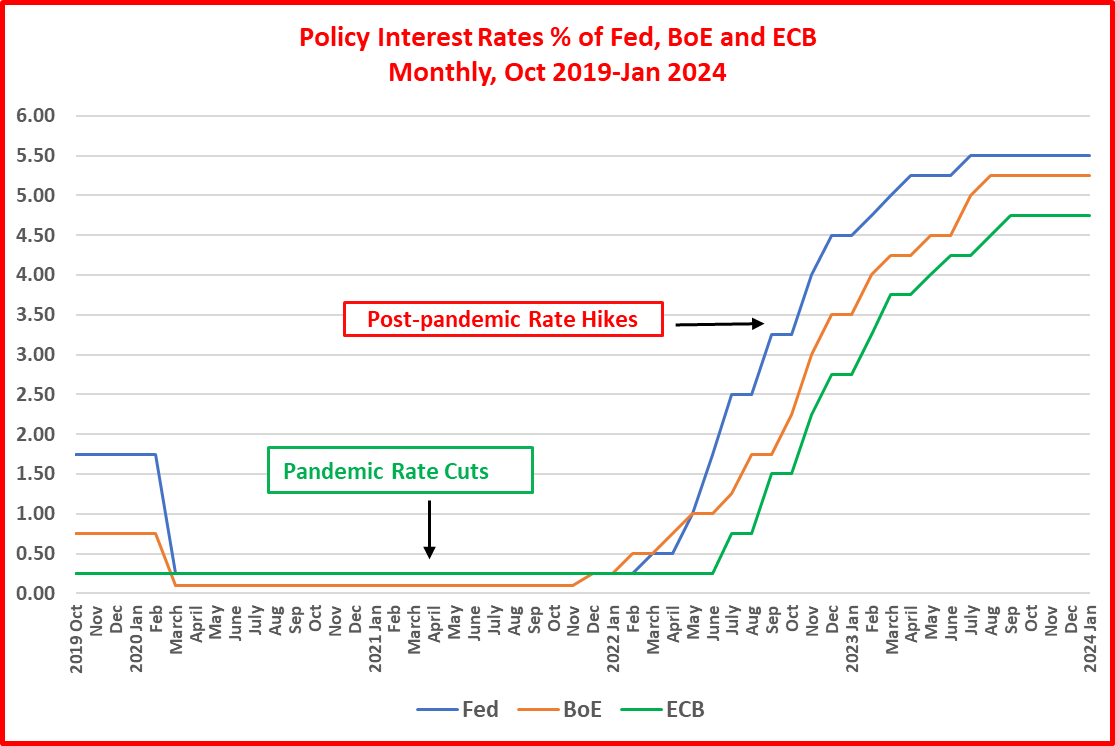

At the dawn of the new year, three major central banks, i.e., US Federal Reserve (Fed), the Bank of England (BoE) and the European Central Bank (ECB), decided in January 2024 to maintain their restrictive monetary policy stances at present levels. This comprises of keeping the policy interest rates unchanged and continuation of quantitative tightening (balance sheet reduction) as has been announced. Keeping policy interest rates unchanged has been the easy and favourite policy decision made in the past 4-6 months.

Accordingly, their policy interest rates at present are 5.25%-5.50% for the Fed, 5.25% for the BoE and 4.00%-4.75% for the ECB. This is the 4-6 months in the row of keeping policy rates unchanged. The present level is an increase of 5.25% for the Fed, 5.15 for the BoE and 4.5% for the ECB from their levels in December 2021, i.e., 0-0.25% for the Fed, 0.10% for the BOE and -0.50%-0.25% for the ECB (see the Chart below).

Their reference to the uninterrupted and competitive hikes in policy rates so far since the beginning of 2022 has been the control of inflation back at the long term target of 2% to maintain the price stability (see inflation Chart below).

During the past six months, inflation in these countries has been steadily falling from the peak towards 2% long term target. The latest inflation rates are 3.4% in the US (peak 9.1% in June 2022), 4% in the UK (peak 11.1% in Oct 2022) and 2.9% in the Euro Zone (peak 10.6% in Oct 2022). Therefore, markets are pricing significant policy rate cuts in 2024 and 2025 in line with fast falling inflation rates.

However, all three central banks state that,

policy stance is sufficiently tight with policy rates at peak,

although inflation has significantly fallen in the past six months, it has not fallen sustainably towards 2% and remains significantly elevated from the target and,

therefore, the present restrictive policy stance needs to be kept until the confidence is fully achieved towards reduction in inflation sustainably at 2%.

Views expressed by the Fed Chairman Jerome Powell at the last press conference held on 31 January 2024 confirm above position. Three highlights are noted below.

“Inflation has eased from its highs without a significant increase in unemployment. That is very good news. But inflation is still too high, ongoing progress in bringing it down is not assured, and the path forward is uncertain.”

“The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. We will continue to make our decisions meeting by meeting.”

We believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.

Accordingly, almost all central banks who follow a similar monetary policy model have tended to follow suit on same reasoning with slight changes in the language.

However, an insight into the recent monetary policy and macroeconomic environment across the globe shows that central banks operate in a global policy cartel are turning wrong pages of the policy book at this time too to justify the restrictive monetary policy stance being continued at presently levels.

Monetary policy books – Cover and inside pages

The policy book has a cover page and a large number of inside pages.

The cover page for most central banks is designed to market its objective as the maintenance of price stability. The control of annual inflation at a pre-announced target, i.e., 2% in developed market economies (5% in Sri Lanka), is marketed as the price stability.

The inside pages present how the monetary policy is implemented and its effects are felt on the wider economy to hang around the inflation target. Therefore, these pages present policy instruments and transmission of their impact towards the price stability/inflation target.

The spread of inside pages is so wide that central banks are able to link anything under the sun to the monetary policy and price stability. Therefore, the story of policy implementation and transmission is quite simple in theory.

First, the policy instrument practiced by most central banks is the overnight interest rates set for their credit transactions through reserve balances of banks. Reserve balances are the conduit used for money printing and credit creation in the monetary system on a regular basis. Therefore, these overnight rates known as policy interest rates are set as policy targets for overnight interest rates on inter-bank lending that settles through bank reserve balances at central banks.

Therefore, in a fractional reserve-based system of money creation by banks, policy interest rates and inter-bank interest rates are close substitutes. As such, the prime conduit for the transmission of the monetary policy towards the price stability is considered as the inter-bank interest rate.

The demand side of the economy is considered as the intermediary of the transmission between the monetary policy and price stability as the policy assumes to affect prices in the economy through changes in the aggregate demand. This is expected primarily through changes in employment and wages in line with Phillip curve hypothesis. Therefore, it is the labour market that is primarily expected to assist the level of price stability preferred by central bank monetary policies. This is the reason why all central banks are generally against wage increases.

The routes, speed and size of the policy transmission are conceptually set out in the most part of inside pages.

Global monetary cartel

Although central banks paint respective monetary policy stories towards domestic price stability and inflation control, their policy models, timing and languages emanate from a global cartel of central banks.

First, except for the Euro zone, almost all countries have sovereign currencies and relevant monetary policies. Countries in the Euro zone have a common currency, Euro, and a common monetary policy implemented by the common central bank, ECB.

Second, while countries have own sovereign currencies, they are highly dependent on hard currencies of few sovereign nations used to access the global economy. These hard currencies are known as reserve currencies. Nearly 83.7% of reserve currencies held by central banks in the world are US Dollar (US currency), Sterling Pounds (UK currency) and Euro. This means that the prime source of the creation of sovereign currencies is the holding of reserve currencies by respective central banks. Therefore, monetary policies of the US, UK and Euro zone together have direct implications on monetary policies of countries which hold reserve currencies. In this, the US monetary policy is a leading force as the US Dollar represents a dominant 59% of global reserves.

Third, monetary policies operate in a global network combined with three blocks.

The US monetary policy directly transmitting to countries that hold nearly 59% of reserve currencies in US Dollar.

The US, UK and Euro monetary cluster that competes each other for maintaining interest rates differentials unaffected by respective monetary policy decisions. This cluster is augmented by other developed countries such as Canada, Australia and Switzerland who are in the periphery of the global reserve currency group.

Developing countries that hold reserve currencies led by the US Dollar.

As the dominant reserve currency is the US Dollar, the global monetary policy network primarily centers at the US monetary policy actions.

Fourth, the global conduit of policy transmission is the short-term international capital flows that depend on interest rate differentials between domestic currency and reserve currencies and sovereign risks.

Fifth, a network of money dealers operates on betting of likely monetary policy path and decisions, i.e., policy interest rates across the world, and trading money for speculative profit by moving markets. They are not bothered on any stability theories other than maximization of speculative profit through insider techniques. For this purpose, they study and interpret policy statements to the letter and spirit to figure out the phase of the monetary policy actions and the size. In fact, they drive monetary policies too as central banks take market trends and developments as early guiding signals.

In this context, policy books of the developing countries are only monetary theory books with fictitious cover and inside pages because the monetary policies they practice are primarily aimed at foreign capital inflow at the edge of US interest rates to maintain foreign currency reserves for the management of the exchange rate stability and balance of payment. Therefore, their policy books with the price stability cover is only a public deception as monetary policy in these countries is nothing but day-to-day money printing to stabilize reserve balances and inter-bank lending operations. The policy transmission beyond is only an untested hypothesis, given the low development of financial system and markets.

Rate cut quandary at present

At the beginning of the rates hike cycle to fight rising inflationary pressures, the expectation of central banks was the resulting rise in unemployment and reduced wage income with significant economic slow-downs. This is usual policy transmission believed by monetarists in line with Phillip curve version of the relationship between inflation, unemployment and aggregate demand.

Therefore, central banks and markets have been in continuous talks on whether the present cycle of significant monetary tightening would result in soft landing or hard landing outcome with inflation down back to targets over time. The soft landing means getting inflation down with a moderate increase in unemployment without a recession. Hard landing means getting inflation down with a significant increase in unemployment with a recession.

Therefore, central banks and markets speculated various modes of landing depending on their beliefs and understanding of monetary policy transmission where nobody had any suspicion over the adverse impact of monetary tightening expected on employment and growth. In fact, most favored such adverse outcomes as compared to unfavoured impact of inflation on all people.

For example, the Fed Chairman Gerome Powell at the hearing of Senate Banking and Finance Committee held on 07 March 2023 responded that the envisaged loss of employment about 2 mn to a higher unemployment rate of 4.4% (compared to 3.4% at the time) consequent to the monetary tightening would be justified socially as, not 2 mn prople loosing employment, but all citizens would suffer from presently spreading high inflation. Therefore, some members of the Committee labeled the Fed Chairman as a cruel person. Further, at the monetary policy press conference held on 15 June 2022 he stated that unemployment risen to 4.5% to get the inflation back down to 2% would still be a strong and favorable outcome, given the historically low unemployment rate of 3.7% at that time.

However, economic growth, labour markets, employment and wage growth have become stronger without any signs of deterioration despite the significant monetary tightening during the past two years. Therefore, central banks believe that the prevailing conditions of strong economy are hidden signs of continuously underlying inflationary pressures that could be escalated if the monetary policies are prematurely relaxed with rate cuts. That is the reason why central banks around the world state that inflation has not fallen sustainably at longer term targets.

If so, the stronger economy despite the significant monetary tightening during the past two years is strong evidence for non-existence of the policy transmission at this time as elaborated in inside pages of the policy book. The stronger economy at present is a result of three main factors.

First, monetary tightening commenced in the middle of reopening of economies from the pandemic. Therefore, the recovery of global supply chains at a gradual phase has expanded the production capacity and growth without any slow-downs caused by highly restrictive monetary conditions. This recovery helped a steady decline in unemployment and steady growth in wages.

Second, new IT inspired and innovated by the pandemic response has improved the productivity across the world.

Third, new labour force and employment structure based on work from home arrangement and new time management systems has helped stronger labor markets and productivity enhancement inducing economic growth with lower unemployment.

Therefore, monetary tightening at such a magnitude is seen a severe policy mistake as high inflationary pressures reported in the second half of 2021 was a result of the historic supply side contraction consequent to the pandemic disruption of global supply chains.

Therefore, global inflationary pressures have been a transitory phenomenon which did not require such a magnitude of monetary tightening across the globe. However, although central banks initially believed this transitory version of inflation, later they happened to give up it and believe inflationary pressures of permanent nature influenced by old monetarists.

It now shows that inflation has started falling on the consumer price index base effect as supply chains and employment have been recovering gradually with the ease of pandemic restrictions. The delayed reopening of China from the pandemic also kept inflationary pressures elevated as China was a major exporter of low prices and low inflation in the world.

Therefore, it is clear that the monetary tightening that has been contagious across the globe at an unexpected rate and speed during the past two years is a macroeconomically flawed decision of central banks. Such flawed decisions are ample in the global monetary history. The best instance is the rapid monetary tightening by the Fed during 2018-19 period causing an unwarranted wave of global tightening and economic slow-downs. The present Fed Chairman accepted it as a policy mistake and promised not to repeat it this time. However, the fact that consequences of such policy mistakes to living standards around the world are not rectifiable and reimbursable is a serious policy governance issue at the global front.

Consequences of present global wave of monetary tightening

It is not disputed of the appropriateness of the ultra loose monetary policies implemented by central banks to deal with macroeconomic uncertainties of the global pandemic in 2020 and 2021. It is observed that economists and policymakers never had any idea of macroeconomic implications of the pandemics and policies required to deal with them.

Therefore, the only option available to governments in the pandemic was to spend for the welfare of the public, households and businesses. This was immensely aided by new money created by central banks (i.e., Fed balance sheet increased by nearly 110%) at interest rates close to zero mostly similar to what they did during the global financial crisis 2007/09. Therefore, central banks interpreted the monetary relaxation at this time as the policy stance taken to prevent disturbances to financial stability. Therefore, no monetarists raised concerns over possible inflationary pressures of such spending through money creation, given the need to help come out of the humanitarian crisis caused by the pandemic at all costs.

However, the prematurely tightening of monetary policies before getting the supply side resettled sent shock waves across the countries and global economy. These are the policy created shocks that are not second to lockdown policies followed by governments in respect of the pandemic. Some of these shocks are listed below.

The increase in the cost of production via high interest rates adding to permanent pressures on inflation.

The public debt service difficulties due to high interest rates and emergence of debt unsustainability concepts.

Wide-spread bankruptcies of businesses and households due to high interest rates, debt rollovers and debt service difficulties.

Bankruptcies of less developed countries due to high global interest rates, disrupted access to foreign capital for the rollover of debt, resulting currency crises and debt default. Sri Lanka, Zambia, Ghana and Ethiopia are the frontline defaulters of this global wave while many countries such as Pakistan struggle in the periphery of the default path.

New round of global poverty across the world.

However, central banks continue to turn pages of their policy books to support the continuation of restrictive monetary policies despite these consequences.

The IMF also supports such restrictive stances of the old monetarists. According to recent media reports (02 February 2024), the IMF Managing Director has stated that “the IMF sees a greater risk to the global economy if central banks start cutting interest rates too soon than if they move “slightly” too late.” Further, its first Deputy Managing Director stated at the World Economic Forum 2023 that markets cutting interest rates in expectation of near-term policy rates cuts would be a risk to the control of inflationary pressures by monetary policies. Therefore, the IMF also is a shadow player behind policy books of central banks to endanger the growth of the world economy.

In contrast, some Fed officials commented towards the end of last year that further policy rates hikes would not be necessary to bring inflation back down to 2% target if markets adjusted interest rates upward. Market analysts commented on this as an official attempt to outsource the Fed’s job to markets.

Therefore, price stability focused policy books of central banks are highly controversial texts that even frontline economists would not be able to establish their benefits to the people and human development of the present world.

Sri Lankan monetary tightening page- A dump outlier

Sri Lankan economy confronted a full scale of crisis on all fronts, public debt, foreign currency, disruption and contraction of supply chains and bank credit crunch. While this was originated by the pandemic, it continued with the political crisis leading to significant uncertainties and hyper inflationary pressures.

However, the central bank interpreted hyper inflationary pressures as a direct result of money printing during the pandemic. Therefore, it followed a hyper monetary tightening through policy rates increased by 10.5% to 16.5% pushing yield rates of auctions of government securities from 7%-8% to historic highs of 30%-33% (see Chart below). In addition, government foreign debt was deflated with a total debt (domestic and foreign) restructuring proposal as a part of the monetary solution to the country’s economic crisis. Therefore, the whole economy was devastated causing long-term structural problems to the economy and living standards. Despite the ambitious monetary policy pages frequently turned by the central bank, more than two years have elapsed without any sign of sustainable recovery of the economy and living standards.

The monetary tightening commenced in April 2022 to forestall inflation rising towards 30%. However, inflation peaked at 69.8% in September 2022 unexpectedly due to market uncertainties created by the political crisis and debt default-based monetary tightening. Therefore, with thee political crisis eased gradually, inflation started falling fast to 35.5% in April 2023 which further fell to 1.3% in September 2023. Therefore, the central bank commenced policy rates cutting cycle in May 2023 when the reported inflation was 35.5% in April compared to the official inflation target of 5% where the index base effect was dominant on reduced price pressures due to the fast recovery of civil society and markets from the political crisis.

This shows that the pages of the policy book turned by the central bank was completely wrong for hyper monetary tightening as hyper inflationary pressures were transient effects of the political crisis cum pandemic. If inflationary pressures of this magnitude exist in the country due to money-driven demand, it would take many years to get it down back to the pre-pandemic levels. Therefore, consequences of the monetary policy mistake at this time will last for at least a decade before commencing a path of recovery.

No trust in the policy model

Policy interest rates-based monetary policy models presently followed by central banks have fundamental design problems that cast doubt on their stated role in public interest.

First, reserve balances and inter-bank lending constitute a negligible quantum of the monetary and financial system. For example, total reserves, i.e., the sum of reserve balances and fiat currencies, are mostly 2%-6% of bank money/credit created in countries. Therefore, changes in policy interest rates cannot have such a wide transmission across the economy where credit creation is largely determined by other risk factors.

Second, the policy transmission depends on interest sensitivity of economic activities. However, other than theoretical interpretations, central banks have no idea of the connection between interest sensitivity and price stability. Therefore, inflation analysis used by central banks is nothing but identification of relative price movements of the commodity basket in the consumer price index underlying the inflation calculation. However, inflation in the monetary policy theory is a macroeconomic phenomenon connected with excess demand fueled by the high monetary expansion in the economy. Therefore, it is frustrating that central banks do not have analytical tools to asses the policy effectiveness on the inflation control and price stability other than standalone, micro commodity analysis.

Third, many developing countries such as Sri Lanka do not have financial markets and inclusion that can pass effects of policy interest rates and reserve balances across businesses and households throughout the country to affect the demand side of the economy and prices in general. Therefore, turning policy pages in these countries similar to what the Fed does in the US economy with highly developed markets has no practical relevance. Therefore, monetary policy in these countries in the present model is only another bureaucracy. The best example is the super tight monetary policy implemented by Sri Lankan authorities in 2022 and 2023 pushing yields of government securities to 30% aimed at inflation control despite the collapsing economy due to the pandemic plus political crisis of the history. It is surprising how the central bank commenced cutting policy rates in May 2023 at the time of inflation reported around 30%.

Fourth, in modern economies operating on money, disparities in wealth and income are directly connected with the disparity in the distribution of credit and financial services across the economic sectors and market participants where the central banks are the core of the distribution system. However, central banks resort to trickle down effects of inter-bank market and reserve balances across all segments of production, utilization and wealth creation. Therefore, present monetary policies do not have a role in a socially fair process of human development in the present generation as they are only wholesale money printing businesses at arbitrary rates.

Fifth, the step-wise manner in which policy rates are changed and other instruments are added in cycles of several years indicates that central banks themselves are not aware of the real policy transmission. For example, present policy rates cycle is nearly 25 months long and no central bank is aware of when it ends or dials back. One page of the policy book is about the tightening cycle of few years followed by a relaxing cycle of several years. To hide their unawareness of the policy adequacy and transmission, they say that the policy is highly data dependent and they wait for more data to move gradually on a meeting-by-meeting approach. The state money-based monetary policy is now about 100 years old in the world while central banks are still unaware of its capacity and effectiveness in respective countries other than what is predicted in the tribal monetary theory.

Need for a new monetary book

Present monetary policy book has been designed on the relationship between money, production and prices in tribal currency societies. Therefore, the book predicts the increase in general prices or inflation as the direct result of the increase in the money stock where the demand side and supply side of the economy are separated with significant time lags. Therefore, central banks are given the mandate to control inflation or preserve the price stability through regulating the money stock. This is the core of the policy book.

However, this is a meaningless hypothesis in modern monetary economies with the majority of money being digital money created by private banks in their books whereas the demand side and supply side are integrated by digital money and markets without long lags. Therefore, the old monetary book is outdated in the modern macroeconomic environment. Accordingly, the price stability-based monetary policy book is only an old faith which has no role in modern digital monetary economies.

Therefore, mandates given by statues to central banks to preserve the stability of prices and economies and maximize employment and real incomes are unachievable, theoretical stuffs. That is why such stable economies are not found in the world despite long aged central banks. Therefore, the public never can trust monetary books of central banks. For example, the mandate of the Fed is the price stability, maximum employment and moderate long-term interest rates. However, the Fed always turns the pages for price stability with 2% inflation measured from personal consumption expenditure and has no idea of other two duties. All three duties in the mandate are highly theoretical macroeconomic concepts that can be interpreted in many alternative ways. For example, the Fed states that 2% inflation balances the price stability and maximum employment.

As the price stability is central bank mandate, whenever prices tend to change substantially in economies, central banks tend to change policy interest rates and monetary conditions as set out in their policy books, irrespective of specific factors behind such price changes whether they are demand side or supply side or external shocks. What they state is that the price stability is their mandate with interest rate as the policy instrument available to discharge the mandate.

For example, At a recent US Senate hearing, when a Senator queried the rationale of monetary tightening at the time of supply-side driven inflationary pressures at present, the Fed Chairman responded that the price stability was the mandate given by the Congress to the Fed with the interest rate as the policy instrument and, therefore, the Fed had no option but to raise interest rates to comply with its mandate. Parallelly, governments also finger at independent central banks for any inflationary pressures to wash their hands from inflationary concerns while central banks blame governments for fiscal deficit as the bottleneck that prevents them from preserving the price stability. Therefore, the world does not need economic theories to prove the irrationally of price stability mandates given to central banks.

However, the monetary policy is blessed with a wide array of instruments that can be suitably mixed up to deal with both demand side and supply side in coordination with government fiscal and other social policies depending on development needs and priorities of the countries. Therefore, the present monetary policy books suffer from fundamental design problems as they are based on a single instrument of overnight inter-bank interest rates and resulting market mechanism. This is due to the lack of knowledge on modern macroeconomic management subject. Therefore, governments must resolve this monetary design problem without delay if they are interested in further human development in modern economies.

If the policy resolution is difficult, the alternative is to find practical mandates. The primary nature of operations of present central banks shows that they only can stabilize the credit and banking system through a regular system of printing and lending of reserves to banks to support the general public trust in the state monetary system. This is the monetary book actually practiced by central banks in real world although they often turn pages of price stability covered books to show the public that they undertake money printing while preserving the price stability despite the fact that no country in the world enjoys the price stability. However, pages of books are turned like those of monetary theology.

Therefore, it is duty of lawmakers to ensure that central banks are entrusted with realistic mandates if they are really interested in a new round of human development in modern digital civilization. Otherwise, state trust-based money and central banking will be extinct in few decades to come as they continue to operate bureaucratically on the tribal faith of sovereign currency systems.

(This article is released in the interest of participating in the professional dialogue to find out solutions to present economic crisis confronted by the general public consequent to the global Corona pandemic, subsequent economic disruptions and shocks both local and global and policy failures. All are personal views of the author based on his research in the subject of Economics.)

P Samarasiri

Former Deputy Governor, Central Bank of Sri Lanka

(Former Director of Bank Supervision, Assistant Governor, Secretary to the Monetary Board and Compliance Officer of the Central Bank, Former Chairman of the Sri Lanka Accounting and Auditing Standards Board and Credit Information Bureau, Former Chairman and Vice Chairman of the Institute of Bankers of Sri Lanka, Former Member of the Securities and Exchange Commission and Insurance Regulatory Commission and the Author of 12 Economics and Banking Books and a large number of articles published.

The author holds BA Hons in Economics from University of Colombo, MA in Economics from University of Kansas, USA, and international training exposures in economic management and financial system regulation)