[Colombo, Sri Lanka] IMM Consult, a leading migration consultancy firm headquartered in Dubai, is excited to announce the grand opening of its newest office in Colombo, Sri Lanka. This expansion marks another significant milestone for IMM Consult as it continues to thrive and make strides in the field of immigration consulting services.

Founded in Dubai by Mr. Shameer Nizar and Mr. Ghulam Madni, IMM Consult has rapidly become a trusted name in migration consulting, demonstrating a commitment to excellence and a mission to assist individuals and families in navigating immigration processes. The company has already established a robust presence in Dubai, and the opening of this new office in Colombo reinforces its dedication to providing unparalleled support to clients.

Specializing in migration services for the esteemed 5 Eyes countries – Canada, the United Kingdom, Australia, the United States of America and New Zealand – IMM Consult stands out in the industry for its unique focus. The company’s in-depth knowledge and expertise in handling the intricate immigration processes of these highly sought-after destinations set them apart.

IMM Consult takes pride in its customer-centric approach, delivering customized solutions tailored to the unique needs and circumstances of its clients. With a team of highly experienced migration consultants and legal personnel, the company ensures personalized attention and precise guidance throughout the immigration journey.

Shameer Nizar, Co-Founder IMM Consult, said “We are delighted to bring IMM Consult’s expertise to Colombo, Sri Lanka. Our commitment to excellence and personalized service remains unwavering as we strive to make the migration process smoother for individuals and families.”

Ghulam Madni, Co-Founder IMM Consult expressed “The opening of our new office in Colombo reflects our vision to expand our footprint strategically. We look forward to contributing to the migration journey of clients in Sri Lanka, offering our specialized services for the esteemed 5 Eyes countries.”

The new branch in Colombo, Sri Lanka will further strengthen IMM Consults’ presence in the region, offering comprehensive migration consulting services to individuals and families looking to migrate to the 5 Eyes countries. The expansion aligns with the company’s vision to make the immigration process smoother, more efficient, and stress-free for clients around the world.

As IMM Consult celebrates another successful year of achievements and milestones, the company remains committed to excellence, integrity, and client satisfaction. We extend an open invitation to all interested parties and well wishers to join us in celebrating this exciting chapter of growth and success.

For Further information and inquiries regarding our migration offerings, contact us at +94 77 798 2379 or visit our website at https://www.immconsults.com/

")

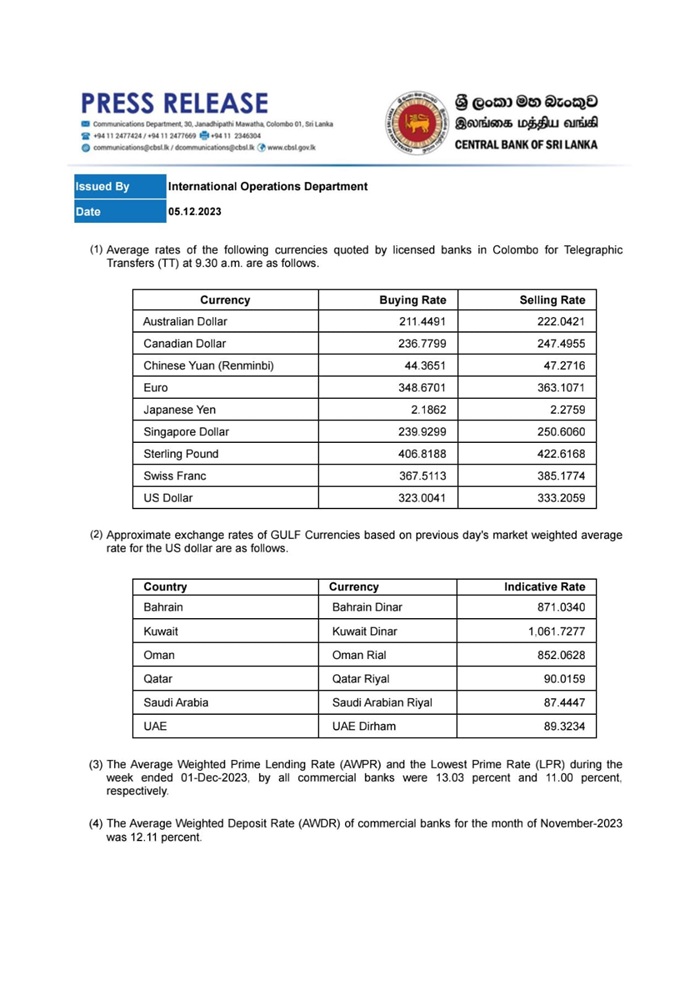

official exchange rates")