Colombo (LNW): Defence State Minister Premitha Bandara Tennakoon today (05) announced plans for the government to empower women to lead the tri forces in the country.

Currently, women in Sri Lanka can only attain the rank of major, particularly in the army.

Accordingly, the government intends to amend military laws to facilitate the promotion of women, ultimately allowing them to head all three forces, Minister Tennakoon said.

Emphasising the historical roles women have played in Sri Lanka, Tennakoon stressed the need for greater efforts to ensure gender equality and equal status for women.

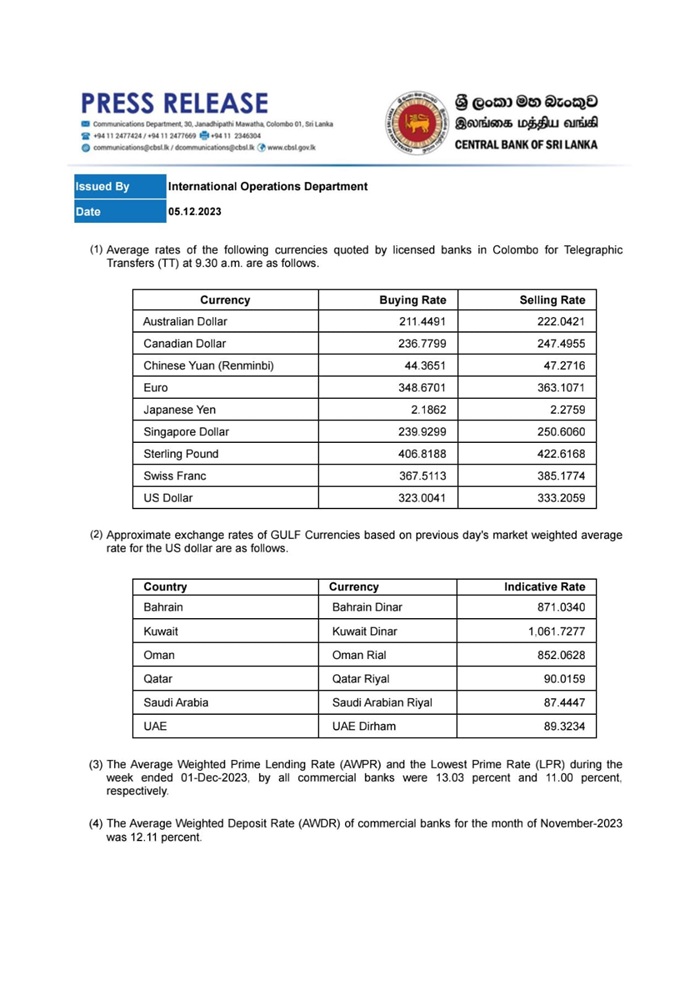

Colombo (LNW): The Sri Lankan Rupee (LKR) today (05) indicates a slight fluctuation against the US Dollar in comparison to yesterday, as per the official exchange rates issued by the Central Bank of Sri Lank (CBSL).

Accordingly, the buying price of the US Dollar has increased to Rs. 323 from Rs. 322.89, and the selling price has dropped to Rs. 333.20 from Rs. 333.32.

Meanwhile, the Sri Lankan Rupee indicates a slight appreciation against several other foreign currencies.

Reporters Without Borders (RSF) is greatly concerned over the disappearance of Minnie Chan, a reporter for Hong Kong daily South China Morning Post, who went missing in China in late October after she covered Beijing’s security forum.

Some friends of Minnie Chan, asenior reporter working for Hong Kong daily South China Morning Post (SCMP)and specialised in defence issues, publicly expressed concerns that she might be detained as they hadn’t been able to reach her since late October, when she covered a Xiangshan Forum, a three-day security conference held in Beijing.

Chan’s latest story, looking at China’s response to the war in Gaza, was published on the SCMP‘s website on 1 November 2023. In answer to an inquiry by Kyodo News, an SCMP executive stated that the journalist was “on personal leave” in Beijing “to handle a private matter”, and refused to give more details over “privacy concerns”. On the same day, SCMPalso threatened to take legal action against independent media outlet Hong Kong Free Press following its coverage of the reporter’s disappearance.

“We are deeply concerned by Minnie Chan’s disappearance as it has become a common practice for the Chinese regime to kidnap journalists and arbitrarily detain them for months in black jails, where they are deprived of their rights and often tortured. We urge Beijing to immediately disclose her whereabouts and, in case she is detained, to proceed with her immediate release.”

Cédric Alviani RSF Asia-Pacific Bureau Director

Frequent disappearances of journalists

It is reportedly not the first time a journalist from SCMP, a media outlet owned by the Chinese technology company Alibaba, goes silent after a work trip to China. According to TV channel Al Jazeera, one of Chan’s colleagues went missing for nine months in 2022, and was later assigned to another department covering less “politically sensitive” news.

In recent years, several journalists and press freedom defenders had been kidnaped or secretly detained incommunicado, to be later confirmed as held in custody by the regime, including publisher Gui Minhai, who was kidnapped in Thailand in 2015, journalist Yang Zewei, who was kidnapped in Laos in May 2023, and publisher Lü Hua, who was revealed to be detained, four months after his disappearance in April 2023.

Since Chinese leader Xi Jinping took power in 2012, he has been conducting a large-scale crusade against journalism, as revealed in RSF’s report The Great Leap Backwards of Journalism in China published in December 2021, which details Beijing’s efforts to control information and media within and outside its borders.

Hong Kong ranks 140th out of 180 in RSF’s 2023 World Press Freedom Index, having plummeted down from 18th place in the span of two decades. China itself ranks 179th out of 180 in the 2023 RSF World Press Freedom Index and is the world’s largest captor of journalists and press freedom defenders with at least 121 detained.

REPORTERS SANS FRONTIÈRES / REPORTERS WITHOUT BORDERS (RSF)

Colombo (LNW): The Education Ministry has announced a reduction in school grades from 13 to 12 as part of new educational reforms, Minister Susil Premajayantha revealed.

Presenting the progress for 2023 and plans for 2024 during the Ministry of Education’s budget presentation, it was revealed that the reforms aim to provide every child with the opportunity to complete school in 17 years.

Under the proposed changes, the age classification for education includes 4 years for pre-school, Grades 1-5 for the primary section, Grades 6-8 for the junior section, and Grades 9 to 12 for the senior section.

The Ministry of Education plans to allocate a percentage of marks for the Grade 5 scholarship exam from school-based evaluations and exams, with a proposal to simplify the exam and eliminate competition.

Additionally, the reforms include the introduction of general level examinations in Grade 10 and advanced level examinations in Grade 12.

The number of subjects for O/L exams will be reduced from 9 to 7, focusing on Information and Communication Technology (ICT), Technical and Professional Skills, and Religion and Values.

Officials highlighted that over 80,000 students fail the Ordinary Level examination annually and assured that no child would fail under the new reforms. All students passing the Ordinary Level exam will have the opportunity to pursue vocational training courses.

A-level subjects will be categorised into academic and vocational education, providing a path for each student to obtain a degree. The Ministry of Education added two new subjects to academic studies, increasing the total from 6 to 8.

Additionally, 10 subject areas under practical studies will offer opportunities for children to obtain degrees in vocational fields.

Colombo (LNW): The container port terminal being built in Colombo by India’s Adani Group is mostly being paid for with funds from a US government agency.

Analysts say it unveils a new type of public-private partnership being rolled out as part of the Quad grouping’s infrastructure push.

A US-funded port project in Sri Lanka that is partly owned by a private group close to India’s ruling party could signal a new form of partnership to counter growing Chinese influence in the Indo-Pacific region.

The Adani Group, controlled by Indian billionaire Gautam Adani and with businesses ranging from ports to edible oils, is developing the Colombo West International Terminal project in Sri Lanka’s capital and holds a 51 per cent stake in the project, backed by more than US$500 million in funding from a US government agency.

Sri Lankan conglomerate John Keells Holdings and the state-run Sri Lanka Ports Authority hold the remaining stakes.

India and the United States – alongside Australia and Japan – form the Quad diplomatic network, whose leaders have said they are focused on providing an alternative to Chinese infrastructure projects for developing nations.

The new Sri Lankan port terminal, resembling a public-private partnership, would appear to be their first such endeavour.

Analysts say the move signals a new determination on the Quad’s part to guard against smaller nations leaning too heavily on China and its arterial trade and military routes. Another terminal at the port is run by China Merchants Port Holdings Co Ltd.

Cedomir Nestrovic, a professor of geopolitics at the ESSEC Business School Asia-Pacific in Singapore, said it would be too simplistic to characterise the US-funded project as just another business deal.

He said geopolitical interests could be seen in the fact that the US$553 million in financing from the US International Development Finance Corporation, a federal government agency, represents nearly four-fifths of the US$700 million required to build the terminal.

There are not many other cases “where America has invested institutionally in this way, with this amount of money,” Nestrovic said. “The political motivation is part of the larger rivalry that exists between the United States and China.”

US efforts to contain China militarily through the presence of American troops in South Korea and Japan have been expanded into the economic sphere via the larger Quad grouping and the push “to ‘cut the grass’ of Chinese investments”, Nestrovic said.

Colombo (LNW): Sports Minister Harin Fernando, in accordance with powers vested with him under the Sports Act, and has appointed a new Sports Council headed by Dr. Maiya Gunasekera replacing its former chairman Arjuna Ranatunga.

Dr. Maiya Gunasekera an old royalist rugby doyen excelled in basket ball and athletics with an indepth knowledge in sports who held the chairmanship of national sports council thrice has to come back again to clear the mess in Sri Lanka’s key sports.

He rendered a yeoman service in cleaning sports administration including cricket rugby foot ball and athletics as and he was appointed to head the sports council under former ministers Gamini Lokuge, C.B.Ratnayake and Mahindananda Aluthgamage.

Dr Maiya volunteered services as a surgeon at the battle front during North East war and saved a number of officers and men who were severely injured

His appoinyment to the helm local sports council is positive sign of resurging cricket rugby and foot ball administration tainted in corruption and irregularities tarnishing the countrys image in sports internationally.

Respected sports administrator Dr Maiya’s very first tasks are to work with the sports ministry to persuade the ICC to lift the cricket ban against Sri Lanka,ensure the country’s participation in the upcoming Asian Games 2023, due to the stalemate position of the governing body, Sri Lanka Rugby Assopciation (SLRA).

The Expert Study Committee appointed to recommend a new Sports Act in Sri Lanka has submitted its report to President Ranil Wickremesinghe.

The Committee, chaired by. Jagath Fernando anothr royalist rugby giant, has made a number of recommendations to comprehensively change the existing legal framework and administrative structure for sports in Sri Lanka.

One of the primary recommendations of the Committee is to establish a National Sports Development Authority (NSDA) to regulate and supervise all sports development activities in the country.

The NSDA would be responsible for formulating policies and strategies for sports development, and would have full supervision over National Sports Associations.

Although the Sports Law has been criticised much in recent times, it is unlikely to undergo major changes in the new proposals.

The much is dependent from Dr Maiya Gunasekera in making radical changes for the revival of sports in Sri Lanka as he has learned of books and men, and learned to play the game from Royal College Colombo.

Doctor Indrajith Maiya Gunasekera a leading surgeon by profession, well known as ‘Maiya’ both in the field of Sports and Medical fraternity is one of them who excelled in both fields.

In 1972 he was called for National duties soon after he joined the Colombo Medical College as a medical student.

While attending classes there he also engaged himself in rugby and played in the third and fourth Rugby Asiad held in Hong Kong and Sri Lanka respectively, under Y.C.Chang’s captaincy.

He joined CR and FC in 1978 and went on to play until 1981. He finally called it a day as a rugby player and opted to get into administration and coaching.

His first assignment was coaching his school from 1992 to 1995 during which he produced several talented players who donned the National jersey while transforming some of them as doctors.

Coinciding with coaching Royal he was assigned as the National Rugby coach from 1993/94 season for the Hong Kong sevens team

He completed his entire medical career while involved in sports which is a rare occasion never happened before and will never happen again.

Colombo (LNW): The United States is highly impressed by Sri Lanka’s efforts and commitment to combating climate change through innovative initiatives.

President Ranil Wickremesinghe engaged in a crucial conversation yesterday (04) with U.S. Special Presidential Envoy on Climate Change, John Kerry, emphasizing Sri Lanka’s commitment to combating climate change through innovative initiatives, official source said.

In the discussion, President Wickremesinghe outlined the Government’s ambitious proposals, prominently featuring the establishment of a Climate Change University.

The President shed light on the comprehensive plan designed to address climate challenges and foster sustainable solutions.

A major focal point of the conversation was the critical issue of raising the necessary funds to effectively tackle climate change, the President’s Media Division (PMD) said.

President Wickremesinghe stressed the imperative of private sector involvement to augment financial resources for climate-related projects.

President Wickremesinghe extended an invitation to Mr. Kerry, urging him to visit Sri Lanka and witness first-hand the on-going efforts and initiatives being undertaken by the country in its commitment to combat climate change, a s enior official said..

Meanwhile Billionaire philanthropist and Microsoft co-founder Bill Gates noted that his Bill & Melinda Gates Foundation (BMGF) is committed to support Sri Lanka in building a robust and climate-resilient nation, he added.

In a significant development at the 28th Conference of the Parties (COP28) in Dubai, President Ranil Wickremesinghe engaged in a strategic meeting with Mr. Bill Gates, Co-Chair of the Bill & Melinda Gates Foundation (BMGF) today (03), the President’s Media Division (PMD) said.

The discussions revolved around collaborative efforts to address global challenges and enhance Sri Lanka’s pivotal role in the world’s tropical belt.

During the meeting, the Billionaire philanthropist and Microsoft co-founder expressed the commitment of the BMGF to support Sri Lanka in building a robust and climate-resilient nation, the statement said.

The Foundation, which is already involved in initiatives in Sri Lanka, pledged to deepen its engagement with the country. Specific areas of focus include agriculture modernization and the establishment of data systems for agriculture.

The collaboration also aims to strengthen Digital Public Infrastructure and enhance Sri Lanka’s expertise in climate and adaptation.

President Wickremesinghe highlighted Sri Lanka’s green initiatives presented at COP28, seeking the support of the BMGF in advancing these sustainable projects.

The President emphasized the need for collective action to address pressing environmental issues and underscored Sri Lanka’s willingness to play a constructive role in the global effort.

Colombo (LNW): The construction industry’s outlook for the next three months is positive, mainly due to the gradual recovery in the economy and the expected increase in project work according to the Central Bank’s Purchasing Managers’ Index (PMI) for Construction Industry – October 2023.

However, the firms are concerned about the upward tendency in energy-related costs and the impact of the upcoming tax revisions, said the Central Bank which compiles the Index.

It said the Total Activity Index reached the neutral threshold of 50.0 in October 2023 after twenty consecutive months of contraction.

“Several respondents mentioned that some of the suspended Government-funded projects recommenced at a limited scale during the month.

However, the industry operates with a low level of available work since most of the ongoing projects are in their final stages,” CBSL said.

New orders declined at a slower pace in October compared to the previous month. Many respondents had observed a gradual increase in sizable tender opportunities, mostly scheduled to be commenced in the first half of next year.

Employment remained contracted since the companies operate with limited staff under current circumstances. Further, quantity of purchases declined, yet at a slower pace during the month.

Moreover, several respondents highlighted the pressure emanated from the increase in energy-related expenses. In the meantime, suppliers’ delivery time slightly lengthened during the month.

The Budget 2024 is being presented at a critical time for our country. The country is still battling with the unprecedented economic crisis which had a profound negative impact on our economy.

However, the situation has been slowly, but steadily improving as a result of the progressive and active role played by the current Government in winning support from the IMF to help us in tiding over the crisis and the progress made in negotiating with creditors to restructure the loans.

While this has eased the hardship to some extent, a lot remains to be done. While the country can see a light at the end of the tunnel, we are still not out of the woods.

The Budget 2024 needs to consolidate on the painful gains made by the country in the last one year and pave the way for continuing the painful restructuring that we need to tread to overcome the crisis.

While the Government needs to begin focusing on long-term strategic and structural development challenges, the country faces insurmountable challenges in loan restructuring and repayments.

Reducing the trade deficit and balance of payments will have to be a major focus in the upcoming budget. More than ever, we have to focus on catalysing investment and improving our productive capacity.

Colombo (LNW): The Hambantota International Port (HIP) is gearing up to expand its operations into a refinery, energy hub, and container transshipment, Chief Operating Officer of the HIPG Tissa Wickremasinghe disclosed.

Wickremasinghe emphasised that there is a need for a holistic approach to container handling in Sri Lanka, aiming to capture a vast potential market under a unified national brand. By doing so, there could be cost-cutting benefits for manufacturers in the Indo-Pacific region and the Far East seeking access to Gulf, European, and African markets, he noted.

HIP has gained recognition for its excellence in handling vehicle transshipment, earning a ‘amongst the best in the world’ benchmark. The port recently received an appreciation certificate from shipping line MOL for achieving ZERO damage operation and maintaining safe Pure Car Carrier (PCC) cargo handling.

HIP, the only ISO certified port in Sri Lanka with a focus on Quality, Health, Safety, and Environment (QHSE), attributes its success to stringent practices, protocols, and best-in-class technology.

Yuri Kannangara, General Manager Operations of HIPG, highlighted the importance of modern port management systems, cargo tracking technology, and advanced communication tools in maintaining high standards.

The port’s commitment to safety is evident through clear signage, designated pathways, emergency response plans, and regular drills.

Colombo (LNW): The Court of Appeal yesterday (04) was apprised of an alleged plot to assassinate the former Director of the Criminal Investigation Department (CID), Shani Abeysekera.

The Attorney General reportedly disclosed to the court that the State Intelligence Service had unearthed information related to a conspiracy intending to cause harm to Abeysekera through a staged car accident.

This revelation occurred during the consideration of the writ petition filed by Abeysekera, who sought an order instructing the Inspector General of Police (IGP) and other respondents to provide adequate security due to perceived life threats.

The AG’s statement was conveyed by the Additional Solicitor General to the Court of Appeal’s two-judge bench, consisting of Justices Nisshanka Bandula Karunaratne and Vikum Kaluarachchi.

Previously, the court had directed the Victims and Witnesses Protection Authority to submit a report detailing the nature of the threats against the ex CID Chief.

During the court session, the Additional Solicitor General presented the report from the Victims and Witnesses Protection Authority, confirming threats to Abeysekera’s life and revealing specifics of the purported conspiracy to orchestrate a fatal car accident.

The legal representative appearing for Abeysekera highlighted the inadequate security provided, citing the allocation of only an old motorcycle and three police officers for protection. The lawyer further alleged that despite an order from the Victims and Witnesses Protection Authority to the IGP for ample protection, it had not been fulfilled.

Considering the presented facts, the Court of Appeal Judge Bench scheduled a convening on December 14 to issue an appropriate order regarding the petition.

official exchange rates")