Colombo (LNW): Renowned Sri Lankan singer Athula Sri Gamage has passed away at the age of 60, confirmed his family sources.

He was undergoing medical treatment at Sri Jayawardenepura Hospital when he passed away.

Colombo (LNW): Renowned Sri Lankan singer Athula Sri Gamage has passed away at the age of 60, confirmed his family sources.

He was undergoing medical treatment at Sri Jayawardenepura Hospital when he passed away.

Colombo (LNW): The newly appointed Iranian Ambassador to Sri Lanka, Alireza Delkhosh, made a courtesy visit to Prime Minister Dinesh Gunawardena at the Temple Trees yesterday (06).

During their meeting, Ambassador Delkhosh emphasised the long-standing friendship and close socio-cultural ties between Iran and Sri Lanka, dating back to ancient times.

He expressed his commitment to enhancing economic and cultural relations between the two countries during his diplomatic tenure.

Priemier Gunawardena welcomed Iran’s investment opportunities in various sectors, including agriculture, industry, and energy, in addition to acknowledging Iran’s support for Sri Lanka’s development efforts and assistance during its economic challenges.

The meeting was attended by Secretary to the Prime Minister Anura Dissanayake and K. Soheil, Chief of the Economic & Consular Section of the Iranian Embassy.

Colombo (LNW): The Criminal Investigations Department (CID) has taken a statement from Health Secretary Janaka Sri Chandragupta in relation to the alleged case involving substandard Human Immunoglobulin in Sri Lanka.

This case has seen the recent arrest and detention until November 15th of the owner of Isolez Biotech, who is accused of supplying substandard Human Immunoglobulin to the Ministry of Health’s Medical Supplies Division.

The suspect is a 57-year-old resident of Raddolugama.

It was revealed that 22,500 vials of substandard Human Immunoglobulin, made using human blood, were obtained through falsified documents.

Initially, it was believed that these vials were imported, but it was later discovered that they were produced within Sri Lanka.

Former Minister of Health, Keheliya Rambukwella, previously disclosed that the Health Ministry had received saline or a similar solution, which was falsely labeled as Human Immunoglobulin.

The estimated value of this medicine stock is nearly Rs.1 billion.

official exchange rates")

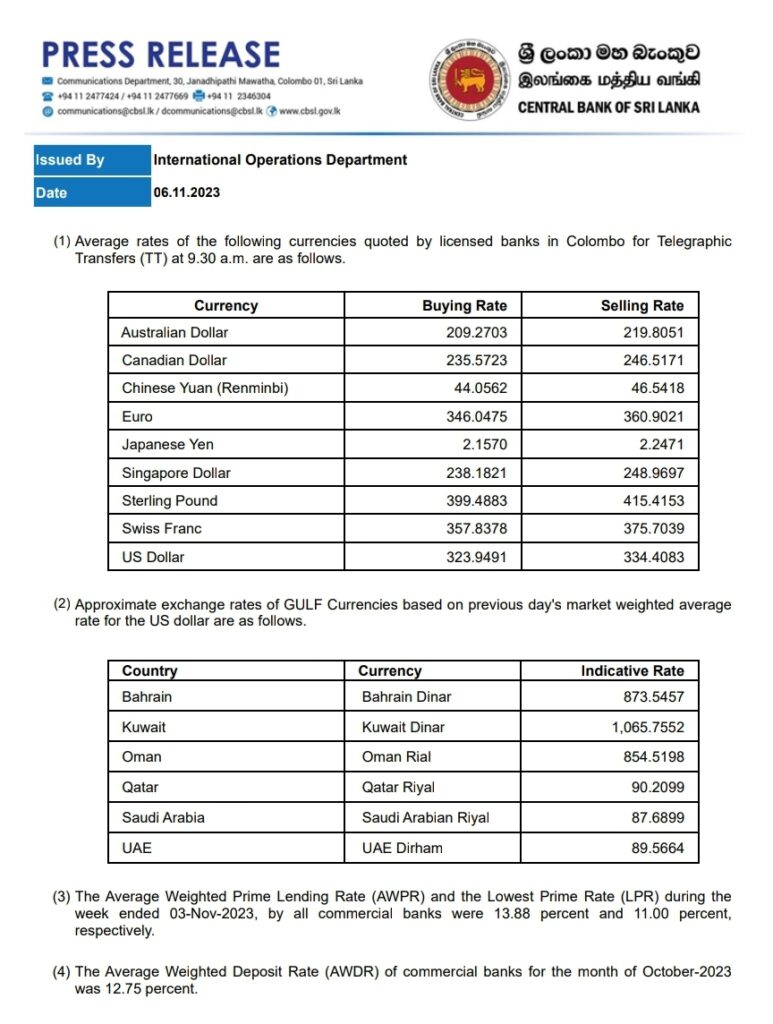

Colombo (LNW): The Sri Lankan Rupee (LKR) indicates slight depreciation against the US Dollar today (06) in comparison to last week’s Friday, as per the official exchange rates issued by the Central Bank of Sri Lanka (CBSL).

Accordingly, the buying price of the US Dollar has increased to Rs. 323.94 from Rs. 323.65, and the selling price to Rs. 334.40 from Rs. 334.13.

")

Colombo (LNW): The Sri Lankan Rupee (LKR) indicates somewhat a sharp appreciation against the US Dollar today (06) in comparison to last week’s Friday, as revealed by leading commercial banks in the country.

At Peoples Bank, the buying price of the US Dollar has dropped to Rs. 321.40 from Rs. 322.38, and the selling price to Rs. 331.52 from Rs. 334.19.

At Commercial Bank, the buying price of the US Dollar has increased to Rs. 323.13 from Rs. 322.63, and the selling price to Rs. 333.50 from Rs. 333.

At Sampath Bank, the buying price of the US Dollar has dropped to Rs. 322 from Rs. 324, and the selling price to Rs. 332 from Rs. 334.

Colombo (LNW): The Ceylon Chamber of Commerce (CCC) advocated for a new economic model that emphasises export-led investment and tourism, as well as promoting the private sector’s role as an engine of growth to establish a sustainable business environment.

This proposal was made during the India-Sri Lanka Business Summit in Colombo, attended by key figures, including Sri Lankan Premier Dinesh Gunawardena, India’s Minister of Finance and Corporate Affairs Nirmala Sitharaman, and others.

While acknowledging India’s support during Sri Lanka’s financial crisis last year, the Chairman of the Ceylon Chamber of Commerce, Duminda Hulangamuwa, stressed that Sri Lanka should not overly rely on bilateral support from regional countries.

He emphasised the importance of an export-led investment approach to ensure economic growth and stability, highlighting the potential for increased trade with India, especially as the world’s economic focus shifts towards South Asia.

Sitharaman expressed enthusiasm for strengthening bilateral relations and urged Sri Lanka to explore new avenues for economic sustainability and growth, highlighting the energy and pharmaceutical sectors as high-growth potential areas.

She also emphasised the role of digitalisation in India’s economic landscape and encouraged Sri Lanka to embrace digitalisation for transparency, efficiency, and inclusivity.

The Vice Chairman of the Ceylon Chamber, Krishan Balendra, highlighted the significance of tourism as a short-term solution to increase foreign exchange earnings, particularly by tapping into outbound tourism from India.

Industry leaders also supported the export-led strategy and called for greater market access in India, including increasing garment exports to promote bilateral trade and benefits for both countries.

Colombo (LNW): Agriculture and Plantation Industries Minister Mahinda Amaraweera proposed a Cabinet Paper aimed at slashing the cost of Muriate of Potash (MOP) fertiliser by 50 percent.

Currently, state-owned fertiliser companies have 28,600 metric tons of MOP fertiliser in their warehouses.

Dr. Jagath Perera, Chairman of government-owned fertiliser companies, emphasised that reducing the price of MOP fertiliser would lead to a 50 percent cost reduction.

The Cabinet Paper, outlining this reduction, has been submitted for approval to the President.

Minister Mahinda Amaraweera made this announcement on the 5th while commencing the development of the Walasmulla Omara village as the second stage of an agribusiness village.

By: Staff Writer

Colombo (LNW): President Ranil Wickremesinghe praised CEAT-Kelani Tyres for its remarkable journey from a State-owned enterprise (SOE) to a symbol of successful privatisation.

Speaking at it in a momentous event marking 25 years of business excellence, Wickremesinghe reminisced about the challenging birth of Kelani Tyres and the pivotal role it played in Sri Lanka’s history.

He paid a tribute to CEAT-Kelani Tyres Chairman Chanaka de Silva’s tireless efforts to bring the company to present stauus overcommig challenges which was his forte from his school days at Royal College as the fiery opening bolwer memarsed schll boy cricketers in 1960s.

Royal had a devastating combination of fast bowlers, (Darrel) Lieversz and (Chanaka) De Silva. They managed to bundle out the Peterites for 42 and 38 runs at Reid Avenue.

At that time Royal also beat Ananda, another start-studded side bowling them out, and they had to get only 82 runs to win and we managed to bowl them out for 76 runs.

“Kelani Tyres was situated in Kelaniya, adjacent to Biyagama, which falls within my electorate. When I assumed the role of Minister of Industries, I recognised the need to close this facility. Kelani Tyres had earned its reputation,” he stated.

He highlighted the tough decisions and battles faced in the process of privatising the company.

“A decision was reached to sell off Kelani Tyres. We initiated the standard process and requested bids. Chanaka was the initial bidder, but for reasons unknown, President Premadasa did not favour it.

This scenario repeated twice, with Chanaka de Silva , being the primary bidder each time, yet he remained unsatisfied. I finally said, ‘Sir, I cannot continue to provide reasons.’

The situation remained the same on the third attempt. At this juncture, we had to make a decision, one that would determine whether we were selecting the best bid or favouring industry giants.”

The President also spoke about the establishment of CEAT in Sri Lanka, a collaboration that became a reality in 1993.

“The next stage involved CEAT and Kelani uniting, a partnership forged in Balapitiya. The Silva’s and the Soysa’s decided to join forces, a decision with its own interesting history.

Chanaka’s father Aarti, in the early 60s, was a member of the SLFP, representing C.P. De Silva. Ajit’s father and Tilak’s father were members of the UNP and part of our working committee.

In 1965, when Mrs. Bandaranaike decided to acquire Lake House Press, my father was the Managing Director.

Ajit’s father and Chanaka’s father collaborated, brought Bandaranaike down and made Dudley Senanayake the Prime Minister in the 1965 election. So that is how our connections go back. In the process, Mahinda’s father lost the election. Regardless, the two companies joined forces and today, we celebrate their 25th anniversary.”

The President recognised CEAT-Kelani as a model of Indo-Lanka cooperation, serving as an example for those seeking to enter the Sri Lankan market.

“This partnership exemplifies successful Indo-Lanka cooperation, serving as a model for those considering entering the Sri Lankan market,” he commented.

CEAT Kelani Holdings manufactures nearly half of Sri Lanka’s pneumatic tyre requirements and exports about 20% of its production to 16 countries in South Asia, the Middle East, Africa and the Far East.

By: Staff Writer

Colombo (LNW): The United States District Court has granted Sri Lanka’s request for a six-month halt on Hamilton Reserve Bank’s (HRB) lawsuit against the country, US media reports said.

HRB has filed a case against Sri Lanka over the 2022 defaulted sovereign bond, claiming that the St Kitt’s-based bank has accumulated a big portion of the defaulted bond, and calling for immediate repayment.

Sri Lanka filed a cross-motion to stay the proceeding to facilitate the restructuring of its external debt, which had garnered support from the country’s bilateral creditors.

In an earlier instance, the United States government wrote the trial judge informing its decision to intervene in the case, and asked the court to reserve the decision on the motion to stay until it had an opportunity to submit a statement of interest.

In her ruling on November 2, Judge Denise Cote suggested that a stay order would not substantially harm HRB’s interests.

“The Court recognises that a stay will prejudice the plaintiff’s ability to obtain a prompt judgement.

The requested stay, however, is not indefinite. Sri Lanka seeks a six-month stay of this litigation while it conducts sovereign debt restructuring negotiations with sovereign and commercial creditors.

Moreover, if Hamilton prevails on its claim at some future date, any judgement will be subject to pre-judgement interest. Accordingly, the prejudice to the plaintiff is limited,” the judgement read.

“A judgement for Hamilton would provide an incentive to other bondholders to engage in line-jumping litigation and deter commercial creditors from participating in the restructuring negotiations.

A breakdown in restructuring negotiations could threaten Sri Lanka’s progress towards these IMF targets, its economic recovery, and the well-being of its citizenry,” the judgement further said.

Meanwhile, FT.COM, which has been closely following the case, said it appears that HRB does not control enough of the bond in question to block the use of collective action clauses.

Earlier, HRB claimed to possess US$ 250 million of the bond in question. The bond’s clauses state that if 75 percent of holders agree to a restructuring deal, it becomes binding on all. With US$ 250 million, HRB can block any deal it disagrees with.

However, according to the recent judgement, HRB claims that Sri Lanka owes them US$ 243 million in principal, which might not give them a blocking stake.

By: Staff Writer

Colombo (LNW): Chairman of the committee of public Finance (COPF), Dr. Harsha de Silva MP has addressed critical issues, starting with the pressing need for tax reform.

He highlighted that tax revenue currently stands at only 8% of GDP, a stark contrast to the 20% it once represented during President Premadasa’s time. Dr Harsha emphasized the importance of revenue rationalization while ensuring fairness in the tax system.

He made these observations at a recent event, titled “Insights with Harsha: Smart Policies & Economic Revival,” which has brought to light key policy discussions essential for Sri Lanka’s economic revitalization.

He also touched upon the topic of demonetization, drawing on India’s experience. He acknowledged both advantages and disadvantages but underscored the potential for transitioning towards a cashless and digital society through the adoption of e-wallets and digital identification systems like Aadhar.

He highlighted that achieving a cashless society should rely on regulation and incentives rather than abrupt demonetization, driving Sri Lanka into a more digitized future.

Another vital issue raised during the event was the adoption of cost-based tariffs or cost-reflective pricing. Harsha noted that this approach reduces government expenditure that would otherwise be used to support loss-making enterprises.

He cited an example of the recent need for Rs 231.5 billion to cover payments to CPC for fuel, illustrating how mispricing can place a burden on taxpayers.

The event also emphasized the need for reforms with a focus on empathy. Harsha’s vision is to instill hope in the youth by demonstrating that meaningful reforms can pave the way for a brighter future. He stressed the importance of committed leaders who understand the challenges faced by the younger generation.

A notable point raised during the event was the need for Sri Lanka to invest in skills development, similar to the successful approach in Tamil Nadu.

Dr. Harsha emphasized that to propel the nation forward, the workforce must be equipped with the right skills.

Tamil Nadu’s 550 engineering schools at various levels produce the talent required by various industries, helping the state aspire to achieve a trillion-dollar GDP by 2030. This underscores the importance of nurturing a skilled labor force.

Audience questions covered various topics, including demonetization, VAT increases, the brain drain, and the development of skilled labor. Harsha’s responses highlighted the need for growth, trade, and investment policy reforms, as well as technology adoption to drive total factor productivity.