Cooperation Afloat Readiness and Training (CARAT) 2023, the annual bilateral exercise hosted by the U.S. Pacific Fleet, got underway in Sri Lanka (19th January 2023). The opening ceremony of CARAT-2023 was held at the Colombo harbour premises and Naval Dockyard in Trincomalee.

The opening ceremony at the pier side of Colombo harbour was held under the patronage of the Deputy Chief of Staff and Director General Operations of the Sri Lanka Navy, Rear Admiral Pradeep Rathnayake and Deputy Commodore Commander, Destroyer Squadron Seven, Captain Sean Lewis. Meanwhile, Commander Eastern Naval Area and Commandant Volunteer Naval Force, Rear Admiral Dammika Kumara and Lieutenant Max Cutchen of the U.S. Navy presided the opening ceremony held in Trincomalee.

CARAT Sri Lanka is a bilateral exercise between Sri Lanka and the United States designed to promote regional security cooperation, maintain and strengthen maritime partnerships, and enhance maritime interoperability and preserve a free and open Indo-Pacific region. The bilateral exercise will feature participants from the Japan Maritime Self-Defense Force and Maldives National Defence Force aside from the Sri Lanka Navy, Sri Lanka Coast Guard and Sri Lanka Air Force.

Meanwhile, training exchanges of CARAT will be held both ashore and at sea in Colombo, Trincomalee and Mullikullam from 21st to 26th January. SLNS Gajabahu and SLNS Samudura of Sri Lanka Navy will take part in the sea phase of CARAT-2023.

CARAT is designed to enhance abilities of the partners to operate together in response to traditional and non-traditional maritime security challenges in the Indo-Pacific region and build relationships through sports, cultural, and information exchanges. Meanwhile, taking part in naval exercises of this nature would open up new avenues for the Sri Lanka Navy to share knowledge, strategies and experience as well as to build trust and strong relationships to step up the readiness and interoperability that allows to overcome common maritime challenges.

In addition, the Band of Sri Lanka Navy is expected to partner with the US 7th Fleet Band to showcase band performances at the Galle Face Green and Colombo Lighthouse (20th January), Dutch Hospital – Colombo (21st January), Viharamahadevi Park (22nd January), Diyatha Uyana, Battaramulla (23rd January), Independence Square (24th January) and One Galle Face premises (25th January) from 6.00 p.m. onwards each day.

Naval personnel who followed the Forensic Diving Course at the Hulhumalé Coast Guard Base of Maldives National Defence Force (MNDF) presented an Olympus TG – 06 underwater camera and peripherals to Commander of the Navy, Vice Admiral Priyantha Perera at the Navy Headquarters (18th January 2023).

As part of the European Union Critical Maritime Routes in Indian Ocean (EU CRIMARIO) Programme, the Gendarmerie Law Enforcement Forces of France has organized this Forensic Diving Course.

The course was conducted by a group of experts in Forensic Diving at the Gendarmerie Law Enforcement Forces of France, from 09th to 13th January 2023 and it was attended by 03 officers and 03 sailors from the Sri Lanka Navy Diving Unit. It covered a range of areas including Underwater Search, Underwater Photography of the Crime Scene and Evidence, Labeling of a Crime Scene, Fingerprint Detection and DNA Collection, Packaging of Evidence Underwater, Corpse Recovery and Inspection and Evidence Collection of Sunken Aircraft.

Upon successful completion of the course, the Gendarmerie Law Enforcement Forces on 13th January gifted a state-of-the-art ‘Olympus TG – 06’ underwater camera and peripherals to the Sri Lanka Navy. Calling on Commander of the Navy at the Navy Headquarters today, the course participants presented those equipment to the Navy.

Sri Lanka Navy regularly provides diving support to government and non-government organizations for underwater inspections. The Navy will be able to use this state-of-the-art camera and equipment efficiently in the future when conducting underwater crime-related investigations.

Treasury Secretary Mahinda Siriwardene says Govt’s cash flow management is extremely challenging at present with foreign and domestic financing channels exhausted: also says difficult to find additional resources for an election: laments even regular payment of public sector salaries on time, is challenging.

President Ranil Wickremasinghe appoints SLPP MP Pavithra Wanniarachchi as Cabinet Minister of Wildlife & Forest Resources Conservation and CWC leader Jeevan Thondaman as Cabinet Minister of Water Supply & Estate Infrastructure Development.

Indian Minister of External Affairs Dr S. Jaishankar says he had a “good meeting with Foreign Minister Ali Sabry and other ministerial colleagues” in Colombo: also says India-Sri Lanka cooperation in infrastructure, connectivity, energy, industry and health was discussed: adds India is committed to the increase of investment flows to Sri Lanka to hasten economic recovery.

Regulation of the Election Expenditure Bill passed in Parliament with a majority of 61 votes: 97 in favour and 36 against.

Chairman, Election Commission says Police protection has been provided to the 2 members of the Election Commission who faced threats.

Veteran film Producer and Director Dr. Sumithra Peries, wife of late Dr. Lester James Peries, passes away at age 88 years.

Minister Manusha Nanayakkara says although the Samurdhi allowance will continue to be paid, measures are underway to remove all other benefits given to low-income families along with the Samurdhi allowance.

Hector Kobbekaduwa Agrarian Research and Training Institute study reveals over 200 mn coconuts have been destroyed by toque macaque, monkeys and giant squirrels in 2022.

SLPP MP Gevindu Cumaratunga says President Ranil Wickremesinghe should seek a fresh mandate if he intends to fully implement the 13th Amendment to the Constitution: asserts the President’s responsibility is to complete the remainder of Gotabaya Rajapaksa’s 5-year term.

‘Paying Wards System’ in state-run hospitals grabs spotlight at a time when the lauded free healthcare system is becoming a burden on the economy: medical practitioners accuse Govt of attempting to privatise the state health service under the guise of finding solutions to the country’s economic crisis.

The Ambassador of Japan to Sri Lanka, H. E. Hideaki MIZUKOSHI met with Commander of the Navy, Vice Admiral Priyantha Perera at the Navy Headquarters (18th January 2023).

The ensuing discussion between them mainly focused on several matters of bilateral importance. The Defence Attaché at the Embassy of Japan in Colombo, Captain Yuki YOKOHARI was also present on this occasion.

The cordial discussion drew to a close with and exchange of mementos, symbolizing the cooperation and goodwill.

The Nelumyaya Foundation Corporate Social Responsibility (CSR) initiated another pilot project distributing school equipment to children of low-income families attending 84 selected schools in Rideemaliyadda Divisional Secretariat, Mahiyanganaya.

Today (19), we distributed shoes, water bottles and etc. for twenty (20) selected students at Bhaddatta Secondary School, Mahiyanganaya National School and Arawatta Junior School in Sorabora state, Mahiyanganaya.

The initiative expects to contribute to the development of quality education in Sri Lanka in an effort to minimise the discrepancies in the education system and is committed to carry the distribution across the island for children with difficulties.

You are most welcome to contribute to this humanitarian operation by joining hands with us.

The Universal Periodic Review – UPR was established when the United Nations Human Rights Council – UN HRC was created on 15 March 2006 by the UN General Assembly. On 18 June 2007, one year after its first meeting, members of the UN HRC agreed on its institution-building process – providing a road map to guide the future work of the Council. The UPR is the newest addition to the long-standing regulatory framework for monitoring or supervising UN member states.

Do the one hundred and ninety-three (193) member states honor and implement agreements and promises made to the United Nations? Some countries are not worried about human rights violations in their countries. The UPR is a tool for investigating or scrutinising such issues and has been implemented for the last fourteen years. It combines different concerns, previously monitored by separate treaty bodies and working groups, into one process.

The UPR takes place three times a year in a series of meetings of the UPR Working Group in Geneva. In this process, the UN questions its member states to see whether those states have honoured their obligations. It also gives an opportunity for other member countries to question or criticize a state that is undergoing the UPR process. At this time, friendly countries of the scrutinised country will exaggerate, portraying it as a country that respects human rights, democracy, and rule of law. It is to be noted that any country can ask a few questions, make statements and propose recommendations.

In this process, a country subject to its UPR cycle will submit a report to the UPR Working Group at a specific time. This is called a National report and may exaggerate the country’s ‘achievements’, misinforming the UN about: what they are implementing; what they are going to implement; what they have not implemented; and their intentions etc. The UPR unit of the Office of the Human Rights Commissioner – OHCHR also submits its report on the country. Members of Civil society organizations including human rights activists who carry out specific country programs submit a report too. This is known as Stakeholders’ reporting. These reports are compiled into a summary.

To oversee this process, representatives of three countries known as the ‘Troika’, selected by the forty-seven member countries of the UN HRC are appointed to discuss all the reports with the country under scrutiny.

Following this, on a specific day, the UPR Working Group meeting is discussed in an open forum in the UN. During this process, member countries express their doubts, fears and apprehensions about the country under scrutiny. Within exactly forty-eight (48) hours of this scrutiny – the ‘Troika’, facilitated by the OHCHR submits an ‘outcome report’ on the country, to the UPR Working Group. The statements, recommendation and queries that have been accepted or rejected by the country under scrutiny can be found in this report.

Fourth Cycle underway

Although the UPR Working Group would have adopted the report, the respective country is allowed to make some changes in their position within two weeks.

Following this, the report is submitted for approval by the UN Human Rights Council in their usual session. At that time, the country under review is allowed to present its views again. In addition, member states and non-governmental organizations may also submit comments.

So far, forty-one UPR Working Groups have been held. Three cycles for Member States have been reviewed, and the fourth Cycle is currently underway.

In December 2008, when Israel faced its first UPR, fifty countries, along with Islamic countries and some other countries, raised very serious questions about Israel.

Because of this, in January 2013, Israel refused to participate in its second UPR Cycle. At the time, this was seen as a revolutionary decision by Israel. Due to UN pressure, eventually Israel re-joined the UPR process and seventy-four countries raised questions to Israel, putting it under severe pressure.

Based on the fourth Cycle of the UPR, Sri Lanka will be discussed at the 42nd session of the UPR Working Group on 1st February 2023 in Geneva.

Sri Lanka’s National Report for this has been published – consisting of thirteen (13) pages and eighty-three (83) paragraphs. Meanwhile, the Stakeholders’ reports covering seventeen (17) pages and (82) paragraphs have also been published. In this report, some important NGOs’ reports were not included due to late submission. Fortunately, their submissions are covered in some other joint statements.

United Kingdom – UK, Algeria and Qatar have been appointed as ‘Troika’ countries for the forty-second session on Sri Lanka.

Countries waiting to question Sri Lanka

In the impending UPR process on Sri Lanka, it is believed that many countries are waiting to question Sri Lanka on accountability, as promised to the UN Secretary General Ban Ki Moon in May 2009, and on the draconian law known as the Prevention of Terrorism Act – PTA. In addition, states are waiting to ask questions about the failure of seventy-four years of promises to create a political solution to the Tamils: especially after thirteen years since the end of the war. Now it’s obvious to the international community that Sri Lanka is buying time and space until they fully achieve their four pillars – Militarisation, Buddhistisation, Sinhalisation and Colonisation of the North and East. It’s believed that once this is fully done, there will be no question of a political solution for the Tamils on the island.

The first Cycle on Sri Lanka was held in May 2008 at the 12th session of the UPR Working Group. At that time, Bangladesh, Cameroon and Ukraine acted as ‘Troika countries’. During this process, fifty-six (56) member countries asked serious questions creating a very embarrassing situation for Sri Lanka.

The second Cycle on Sri Lanka was held in November 2012 at the 18th Session of the UPR Executive Committee. At that time – India, Benin and Spain acted as ‘Troika Countries’. In this Cycle, ninety-eight (98) member countries questioned Sri Lanka. This may be a record-breaking number of countries questioning a country under scrutiny in the UPR Working Group meetings. Over fifty percent of the one hundred and ninety-three (193) member countries raised questions, making Sri Lanka’s atrocious human rights situation known to the world.

The third Cycle took place in November 2017 at the 28th session. In this process eighty-eight (88) countries questioned Sri Lanka.

To be frank, Sri Lanka has never implemented or respected the recommendations they have agreed to, nor kept the voluntary pledges they themselves have given during the UPR process!

Cycle

01

02

03

04

Session

2nd

14th

28th

42nd

Date examined

13/05/2008

1/11/2012

15/11/2017

01/02/2023

Report & date

A/HRC/8/46 05/06/2008

A/HRC/22/16 18/12/2012

A/HRC/37/17 29/12/2017

— —

N°. States intervened

56

98

88

—

Agreed*

45

110

177

—

Rejected**

16

94

—

Noted/delayed***

08

53

—

Troika countries

Ukraine Cameron Bangladesh

Benin India Spain

Burundi Rep. Korea Bol. Rep. Venezuela

UK – United Kingdom Algeria Qatar

* Agreed = no. of statements and recommendations made by other states, enjoying the support of Sri Lanka

** Rejected = no. of statements and recommendation that did not enjoy the support of Sri Lanka

*** Delayed/Noted = Sri Lanka would reply later or noted the point: it’s a diplomatic reply rather than rejection

Sri Lanka has either rejected/delayed answering, or diplomatically said it noted the contents, of many of the recommendations or statements made by other States in the past UPR cycles. Although the number of statements and recommendations agreed to is high – the point is whether they are taken seriously or not, and whether they are implemented or not. Some interesting questions, concerns and recommendations raised by other countries, on Sri Lanka, are given below:

Questions raised in the past

Many countries wanted Sri Lanka to: examine the possibility of ratifying OP-CAT and ratifying the Rome Statute; accede to the Rome Statute of the International Criminal Court (ICC) and draft a law on cooperation between the State and the Court; ratify the Second Optional Protocol to ICCPR; continue its efforts to ratify the International Convention for the Protection of All Persons from Enforced Disappearance; fully incorporate the Convention on the Elimination of Discrimination against Women into its domestic system; adopt a number of laws on freedom of expression and speech, and of the media; and consider the possibility of abolishing the death penalty.

Countries remained concerned about: Sri Lanka’s consolidation of executive power; the militarization of former conflict zones; serious human rights violations, including disappearances, torture, extrajudicial killings, and threats to freedom of expression; reports of human rights violations under the Prevention of Terrorism Act; intimidation and harassment of human rights defenders and journalists; insufficient protection of rights of religious minorities; and prevention of acts of violence.

Sri Lanka was encouraged to continue the reconciliation and peace process, urged to resolve residual resettlement and rehabilitation issues; and develop a strategic plan against human trafficking. Countries were concerned about the slow progress in the constitutional reform and transitional justice process, urging a constructive approach to addressing post conflict reconciliation issues and resolving post-conflict challenges.

Many countries encouraged Sri Lanka to adopt an action plan to implement its Human Rights Council resolution commitments; noting that much work remained on accountability, transitional justice and reconciliation. Concerns remained about recent developments in the fight against impunity; Protection of Victims of Crime and Witnesses Act, and the Peace building Priority Plan…….

So far what we have learned from the UPR mechanism and process of the UN HRC is that, although it looks different to the earlier mechanisms (Treaty bodies and other working groups), eventually the UPR has no teeth. It is just like other mechanisms in its incapacity to punish a country’s failure to implement its agreed commitments.

If one seriously considers the time, energy, finance and other means spent on the UPR process, one comes to the conclusion in UN language, what counts is ‘just’ the potentially powerful act of “naming and shaming”.

It is to be noted that according to the last resolution, Sri Lanka will not be on the agenda during the 52nd session of the UN HRC, which will begin in the last week of February. However, lobbying on Sri Lanka continues as usual.

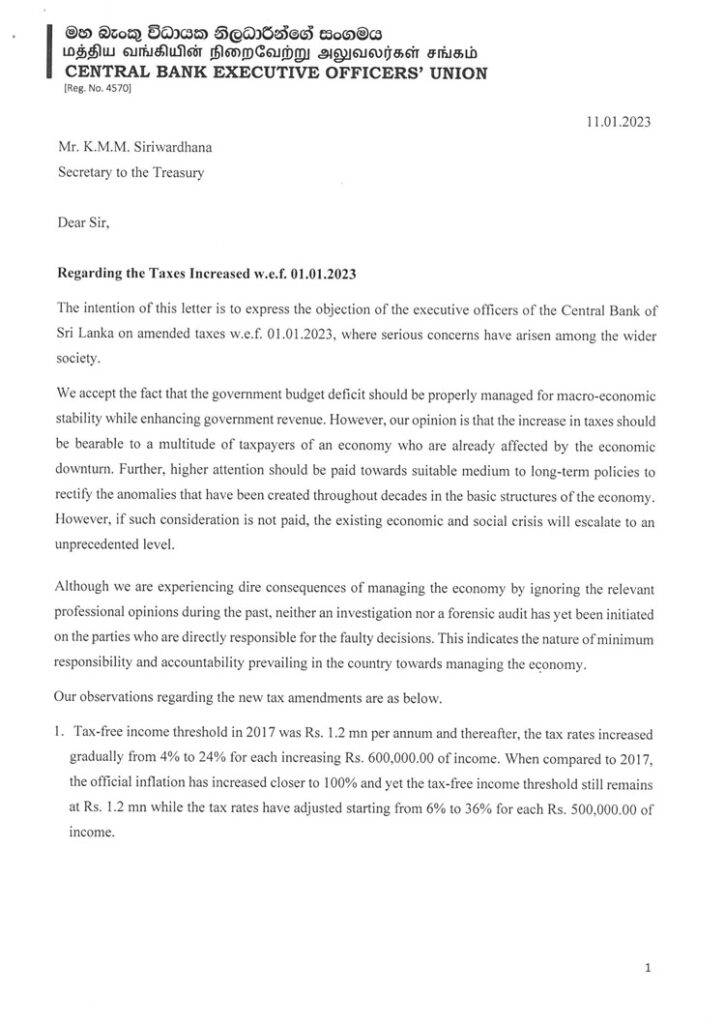

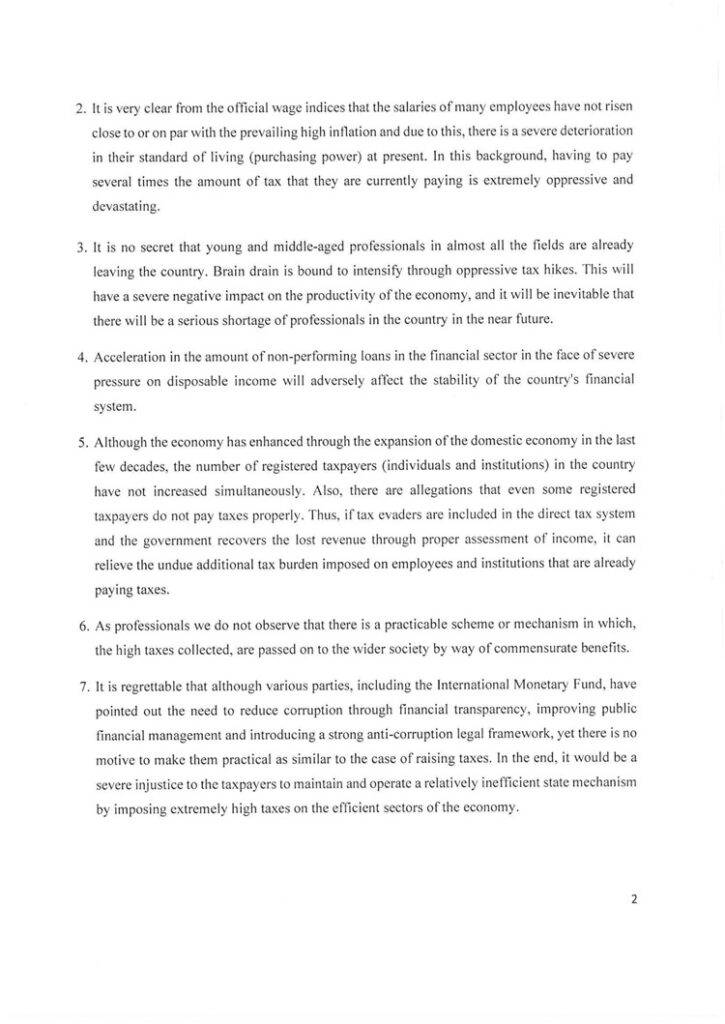

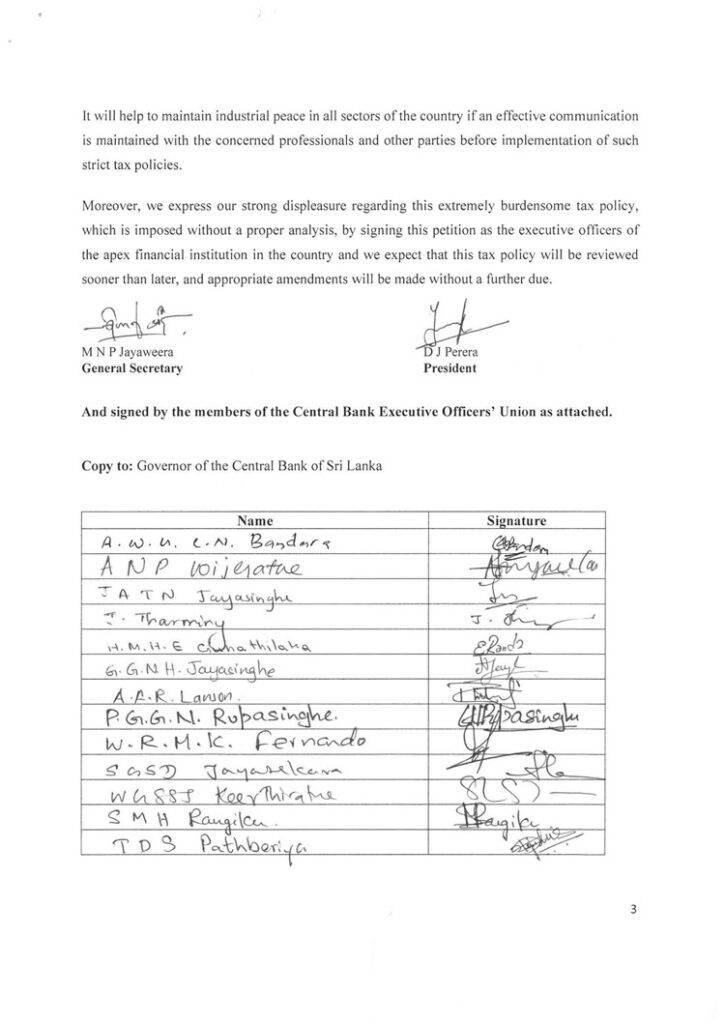

The Executive Officers’ Union of the Central Bank of Sri Lanka (CBSL) has reportedly expressed its strong concerns over the new tax structures introduced with effect from January 01, 2023.

In a letter addressed to Treasury Secretary Mahinda Siriwardena and forwarded to CBSL Chief Nandalal Weerasinghe, the Union warns these tax revisions could seriously have a negative impact on a number of fields.

These concerns come to light following many disputes over the top management of the CBSL fueled by bureaucracy leading to industrial disharmony.

LNW earlier disclosed how the holiday leave enchashment entitled to employees under the Shop and Office Employees (Regulation of Employment and Remuneration) Act, 1954, which was set to be paid on the dawn of February this year, was settled on December 30, 2022 by the CBSL top management in a move to bypass the taxes applicable to 2023. Then it was revealed how the CBSL had established a strict repressive action against its trade unions, further confirming the turmoil within the island nation’s monetary regulator.

India’s heavy commercial vehicle maker Ashok Leyland on Wednesday announced that it has bagged an order from the Sri Lanka Transport Board to supply 500 buses.

The Sri Lanka Transport Board is a state owned single largest bus transport provider with 110 depots throughout the island nation and operates buses in city routes, hilly and rural routes and also in long distance inter-city routes.

As a part of the order secured from SLTB, it delivered 75 buses to the neighbouring country, the Hinduja Group flagship company in a statement said.

The order was part of the Line of Credit extended by the Export Import Bank of India, under the Economic Assistance Scheme of the Indian government.

“More than 5,000 Ashok Leyland buses are currently in operation with Sri Lankan Transport Board and these new 32 seater buses are expected to be put into operation in rural routes throughout the island” PTI quoted Ashok Leyland president — International operations Amandeep Singh as saying.

“Ashok Leyland buses and trucks are also manufactured in Sri Lanka, and the brand ‘Lanka Ashok Leyland’ is well known among Sri Lankans for their daily transportation requirements,” he said.

“Ashok Leyland is proud of its long-standing partnership with the Sri Lankan government. We also thank the Government of India for assistance towards strengthening public transport infrastructure in Sri Lanka.”

Sri Lankan Transport Board operates in diverse routes and conditions and the new Ashok Leyland buses would be best suited for roads in the rural routes.

Indian High Commissioner, Sri Lanka Gopal Baglay handed over the first set of buses to Sri Lanka Minister of Transport and Highways Affairs Bandula Gunawardana at an event in Colombo recently, the company said.